Good News About Healthcare Costs for People on Medicare

One very big expense to stop worrying about

Everyone is likely aware of the Fidelity report stating that a 65-year-old person in 2023 will need to save $157,000 for medical costs, while a married couple will need $315,000.

We know that 69% of people ages 65 to 69 have less than $100,000 saved, and 71.2% of people ages 65 and older have less than $250,000 saved and that makes the Fidelity numbers really scary.

I debunked that number in my May 2023 article titled “How to Plan for Medical Expenses After Age 65.”

But because of the Inflation Reduction Act of 2022, there is some really good news to share. That news will also result in significantly lower costs. Prescription drug costs are less of a worry today, and they will be even less of a worry in 2025.

Even with the Part D prescription drug benefit, the cost of drugs has been an ongoing problem. The fact is that nine out of ten people aged 65 and older report taking at least one medication. However, 54% of adults aged 65 and older report taking at least four medications.

According to the National Library of Medicine, 20% of older adults reported financial hardship due to prescription drug costs. The hardship is a direct result of high out-of-pocket costs and the structure of the Medicare Part D program.

The History of the Part D Prescription Drug Benefit

Before December 8, 2003, seniors did not have comprehensive prescription drug coverage. There were three Medicare Supplements (Medigap) that included some prescription drug coverage. Those plans were H, I, and J. But they were expensive, resulting in few seniors buying them.

According to a July 2001 report from the GAO, the average premium for a Medigap Plan J was $1672. That was almost $450 more than the other Medigap plans without prescription drug coverage.

Plan J paid 50% of prescription drug costs up to a maximum of $3000 per year. But that was only after a $250 deductible. That is why only 4% of Medicare beneficiaries enrolled in it.

As prescription costs became a burden, President George W. Bush signed the Medicare Prescription Drug, Improvement, and Modernization Act, which created Part D of Medicare.

While Part D helped many seniors, it still left people with high prescription costs with a big problem. To meet budget requirements, the coverage included a gap, also known as the donut hole. Once in the donut hole, the member had to pay a percentage of drug costs.

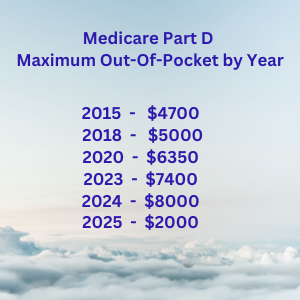

In addition to the donut hole, there was an annual out-of-pocket maximum. That annual maximum out-of-pocket grew between 2003 and today, as can be seen below.

To help you understand just how big a deal this is, I will tell you about two of my clients. One of my clients is on several really expensive medications that were covered pretty well before he turned age 65. However, Medicare Part D doesn’t do as good a job covering prescriptions as health insurance does for people under age 65. In 2023, before he entered the donut hole, his costs were manageable. During his first month on the plan, he had to pay $608, which was the cost of his first drug plus a copay after the deductible.

In each subsequent month his cost was $172 for this specialty drug, But, in the seventh month, his costs jumped because he was in the donut hole. As a result, he started skipping some refills.

Another client incurred a cost of more than $300 monthly once in the donut hole.

The elimination of the donut hole and the lowered maximum out-of-pocket will be a huge relief for both clients. Anyone with multiple non-generic prescriptions will also see relief in 2025.

Lower Healthcare Costs for People on a Budget

I strongly encourage people on a fixed, limited budget to consider enrolling in a Medicare Advantage Plan PPO offered by one of the national insurance companies. As an insurance agent specializing in Medicare, my wife and I have been enrolled in one since 2019.

In most areas of the country, these plans are offered with no premiums. And they include the Part D prescription benefit. I know that there are many naysayers when it comes to Advantage Plans. However, these plans have actually become better over the last few years and the maximum out-of-pocket has slowly been lowered. In my plan, I have seen my maximum out-of-pocket lowered from $6500 to $3850 for 2024. Even my out-of-network has been reduced to $5750.

Last year, my maximum out-of-pocket was $5500. But with two hospitalizations, two surgeries, and six weeks of home healthcare IV antibiotics, my total cost was less than $2200.

If you take the time to understand how your coverage works, a good Advantage Plan can save you thousands of dollars over a Medicare Supplement combined with a Part Prescription Drug Plan.

If you are wondering, I have many clients enrolled in a Medicare Supplement. For those who can easily afford the monthly premiums, a supplement is a great choice. By choosing an Advantage Plan, my wife and I save a combined $350 monthly that would have gone to pay premiums.

Conclusion

If you are not on multiple medications, especially the tier 3 through tier 5 drugs, none of this will matter in 2025. And I hope that you can go through your retirement without needing expensive medications.

The Inflation Reduction Act of 2022 will bring much-needed relief to people who are on expensive medications or who find themselves on those medications later.

Contrary to Fidelity’s claim that you will need $157,000 ($315,000 for a couple) to pay for medical expenses, your retirement healthcare costs will likely be far less. Even for those with health problems, it is possible that your costs will be far lower than is thought.

None of this is to say that you will not incur higher costs. There are a lot of ways that medical costs can be higher than I am discussing.

For those on Advantage plans, it is possible that you will use providers that are not on your network. For example, a prescription drug may not be covered on your Part D formulary.

Finally, none of this considers nursing home costs, which Medicare does not cover.

But for most of us, our out-of-pocket costs are capped at manageable levels. With the right planning, you can enjoy life without worrying that you are one medical event away from bankruptcy.