How to Plan for Medical Expenses After Age 65

Putting current studies into perspective.

Everyone has read the articles that quote the Fidelity Retiree Health Cost Study that stated that an individual age 65 would need $157,000 and a couple aged 65 would need $315,000 in retirement for health care costs. According to a Fidelity article, How to Plan for Rising Health Care Costs, retiree health care money pays for Medicare Part D and B premiums, prescription drug costs, copayments, coinsurance, and doctor and hospital visits.

On July 19, 2023, the Kaiser Family Foundation released an article titled: Medicare Households Spend More on Health Care Than Other Households.

According to this article, Medicare households will spend $6,557 per year on health care. This includes the cost of their health care coverage through monthly premium payments, deductibles, and other cost-sharing requirements. In addition, some Medicare beneficiaries will pay for a Part D Prescription drug plan, dental care, vision, and hearing care.

Understanding the Gap

There appears to be a huge gap between spending $157,000 for health care after age 65 and a Medicare household spending $6,557 on health care. An even bigger gap exists between $315,000 for a couple in the Fidelity study and the annual expenditure of $6,557 for a Medicare household.

So how do we reconcile these numbers?

If you divide the Fidelity estimate of $157,000 in lifetime healthcare expenses by the $6,557 in annual average expenses for a Medicare Household, you arrive at 23.94 years. That means a 65-year-old would have to live until age 88.94 and spend the full $6,557 annually.

If you do the same math for a couple (since the Kaiser Family Foundation uses Medicare household), a couple age 65 would have to live an additional 48 years to spend $315,000 at $6,557 annually.

But the real question is whether these numbers matter.

In my opinion, neither number matters. And none of the numbers are accurate for planning purposes.

How to Plan for Health Care Expenses After Age 65

In my opinion, the first mistake both studies make is including Part B premiums in the calculation of health care costs.

Part B premiums should not be included for two reasons. First, it is deducted before you receive your Social Security Retirement check. Your retirement income for budgeting is based on the money that you have available to spend. And the Part B premium never comes out of your spendable income. To better understand this statement, let’s assume your monthly Social Security benefit is $1664.90.

What you see every month is $1500 deposited into your checking account. For planning and budgeting, $1500 is the only number that matters.

Second, and even more importantly, regardless of the Part B premium increase, your Social Security check can never be lower than the previous year. That is due to the Social Security Hold Harmless provision. In addition, in most years, the Social Security cost of living increase has been higher than the Medicare Part B premium increase.

That means that looking at the Kaiser Family Foundation number of $6,557, we can subtract $1,978.80 (the Part B premium of $164.90 X 12). That leaves you with an average annual expenditure of $4579.

Should you use $4,579 as the basis for your healthcare cost planning? That would require you to put aside $382 a month, which for many people would be impossible. Still, is that a reasonable number to work with in planning for your future healthcare costs?

I think there is a better way and it depends on whether you are in Original Medicare with a Medicare supplement or in an Advantage Plan.

Planning If You Have a Medicare Supplement

If you purchased a Medicare supplement G plan, your monthly premium is approximately $130 if you are aged 65 through 70 and live in a lower-cost state. With a plan G, your maximum out-of-pocket for Medicare-approved medical costs is the Part B deductible of $226. In addition, you will have the Part D premium, which averages $31.50 nationally. I know many people pay significantly less, but we must go with the average.

So, for premiums, you have $161.50 monthly or $1,938 annually.

Planning Point #1: You should plan for increasing premiums in your Medicare Supplement and Part D prescription drug plans.

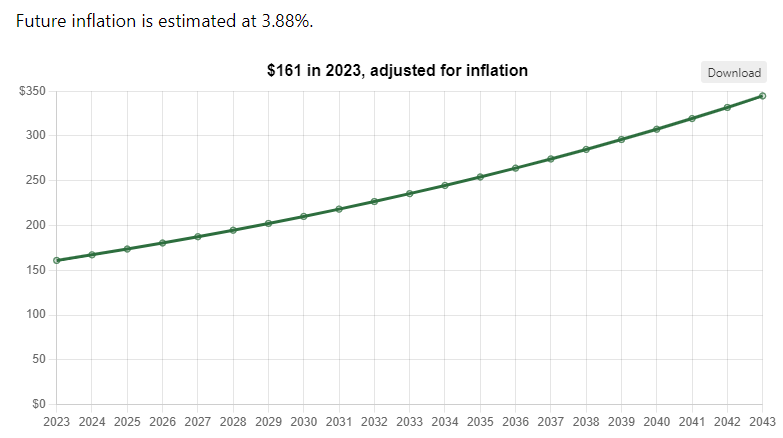

First, you should plan for inflation. Over the last fifty years (1973–2023), inflation averaged 3.88%. The chart below illustrates the impact of 3.88% annually on that $161.00 premium.

As you can see, in twenty years $161 can become $350 monthly.

In addition to inflation, many supplements increase premiums annually based on your age.

This is a dollar amount that you are almost guaranteed to spend.

Planning Point #2: If you currently pay prescription copays and coinsurance, you should include those numbers and use the inflation tool referenced above to understand your future costs.

If you incur annual dental, vision, and hearing costs, apply the same reasoning.

Even if you do not currently incur medical costs, creating a savings plan that will make you feel secure makes sense. Recognize that any number is just a guess, even those from Fidelity and the Kaiser Family Foundation.

Planning If You Are in an Advantage Plan

Planning for future healthcare costs is a little more complicated for those on a Medicare Advantage Plan. That is because, unlike Medicare supplements, your costs can vary widely.

While most Advantage Plans have very low or no premiums, they have an annual maximum out-of-pocket that you may or may not reach. And the maximum out-of-pocket limits vary from plan to plan.

In addition, many Advantage Plans include dental, vision, hearing, and Part D prescription drug benefits. My wife and I see our dentist twice annually for routine cleaning, exams, and x-rays, and we each save close to $500 annually because of our Advantage Plan.

At the very least, I suggest saving at least two times your annual maximum out-of-pocket. For example, my plan has an annual out-of-pocket maximum of $5,250, which has remained the same for the last two years.

I also know that for the first two years, I did not incur any expenses beyond a few copays and $300 for my cataract surgery.

I suggest looking at the costs for a Plan G in your area and subtracting any premium you pay for your Advantage Plan. Then, place that into a savings account for healthcare costs.

That number is $165 (at age 70) monthly or $1980 annually. And since I am on low-cost prescriptions, I would have enrolled in the cheapest Part D plan at $4.80 monthly or another $57.60 annually. That brings the total cost for traditional Medicare to $2,037.60.

I have been on a zero premium Advantage plan for three years. I will use today’s rates for a Plan G in my zip code for simplicity. At age 68, it is $150 a month ($1800); at age 69, it is $160.49 ($1926); and at 70, it is $165 ($1980). I will also assume the lowest premium Part D plan for all three years of $57.60 annually or $172.80 over the three years.

Had I placed that money in a savings account, I would have $5878.80, which is $600 more than my maximum out-of-pocket cost. In addition, the $500 annually for routine dental care would have added another $1500 over three years. That brings my savings to $7,378.80.

Planning Point #3: If you are on an Advantage Plan, you need to begin saving for potential future medical costs. You have copays, coinsurance, and a maximum out-of-pocket.

Planning Point #4: Understand that while reaching the annual maximum out-of-pocket is difficult, it is not impossible. A cancer diagnosis or a major heart or stroke diagnosis can easily result in meeting that out-of-pocket. And depending on the timing of the onset, it can result in hitting the out-of-pocket in multiple years.

Prescription Drug Costs

Regardless of your current health, it is important to plan for the possibility of a future that includes monthly maintenance drugs.

Five years ago, at age 65, I was only on a single maintenance drug. Today I am on two. As an insurance agent working with people ages sixty-five and older, I have talked with people on five, six, or more prescriptions. Some of these people are paying three and four hundred dollars a month in prescription costs.

It is striking that many of these were healthy until, one day, they weren’t. And while the Part D program has improved by gradually eliminating the “donut hole,” it is still possible to have large prescription expenses.

Should you plan for long-term care?

This is a separate issue from potential healthcare expenses as defined by Fidelity and the Kaiser Family Foundation. I have attempted to address these costs in an earlier article titled Six Ways to Plan for Long-Term Care.

Conclusion

In planning for health care costs after age 65, several costs are easy to plan for. But many others are less obvious.

The likelihood of needing health care increases as we age, but that is not a guarantee that we will incur them. Some of us will utilize more healthcare than others. And some of us may not incur any costs beyond the routine annual maintenance.

Nonetheless, without significant financial assets, we should plan how to pay for those costs we may incur.

As a wise man or woman once said, “Expect the best but plan for the worst.”

Get Each New Article Right in Your Inbox

If you want to get notified whenever I post a new article about creating a great retirement, consider signing up for email updates here: https://melschlesinger.medium.com/subscribe

If you are not currently a member of Medium, consider joining. It is the best $5 a month that you can spend. And if you use my affiliate link, it doesn’t cost you anymore, but you will be helping me out. https://melschlesinger.medium.com/membership