WEEKLY BUSINESS ROUNDUP

Global Business Week: Visualizing Careers in Corporate Finance

The state of Financial markets & Economies, Weekly Charts, Business Trends & Statistics

A new era of monetary policy is starting to hit investors in the face following previous estimates that any tightening would be limited and gradual. Stocks ended a rough week, U.S. equity markets continued their 2022 slide on worries about rising interest rates — with money flowing out of growth stocks and into value stocks as Treasury yields surged across the board. The Nasdaq 100 Index fell for a fourth straight session Friday, concluding its worst week since February. For the week, the Nasdaq plunged 4.5% and the S&P 500 sank 1.8%, while the Dow Jones was off only 0.3%. But the S&P closed just above its 50-day moving average, a key technical reading that has attracted dip buying in the past.

The yield on the 10-year Treasury note reached 1.77%, the highest level in two years, and was up 26 basis points (BPS) this week. Oil futures fell but remained above $79 a barrel. Continued virus spread and a weakening Jobs report out of the U.S didn’t help the investor sentiment either. However, the first trading day of 2022 resulted in a historic day for the U.S. stock market as Apple became the first company in history to reach a valuation of $3T. Lifting investor confidence was the belief that Apple will keep launching best-selling products as it explores new markets like self-driving electric cars, augmented-reality glasses, and possibly the Metaverse. Earnings season kicks off in the U.S next week.

While the benchmark dollar index (DXY) added +0.07% for the week, most of its gains were given back by the end of the week — following the disappointing NFP print. EUR/USD rates finished lower by -0.20%, while USD/JPY rates added +0.33%. With risk appetite fading, commodity pairs like AUD/USD and NZD/USD fell back by -1.24% and -1.07%, respectively. GBP/USD rates bucked the trend, gaining +0.39%. DXY closed the week @ 95.74 as it continued to trade in a tight range from late November. Several high-ranked data releases are along with Feds’ statements due in the coming days may precipitate the move out of the current range. For now, the bias remains mixed.

The sell-off of major cryptocurrencies continued, as the easy money environment seems to be winding down. The price of Bitcoin dipped below $41k before rebounding to over $42k at the time of writing. Ethereum has followed its peer on the route to weakness, as have the other digital assets. ETH dropped to just below $3,000 before rebounding — currently trading over $3170. Whether crypto enthusiasts like it or not, lately Bitcoin has acted more like a risk-on asset than a store of value, something which is so vehemently propagated by its proponents. Having said that, cryptos have come a long way in a very short time, and this year would see further maturing of this space. The umbrella of regulation might also help them strengthen their position in the mainstream.

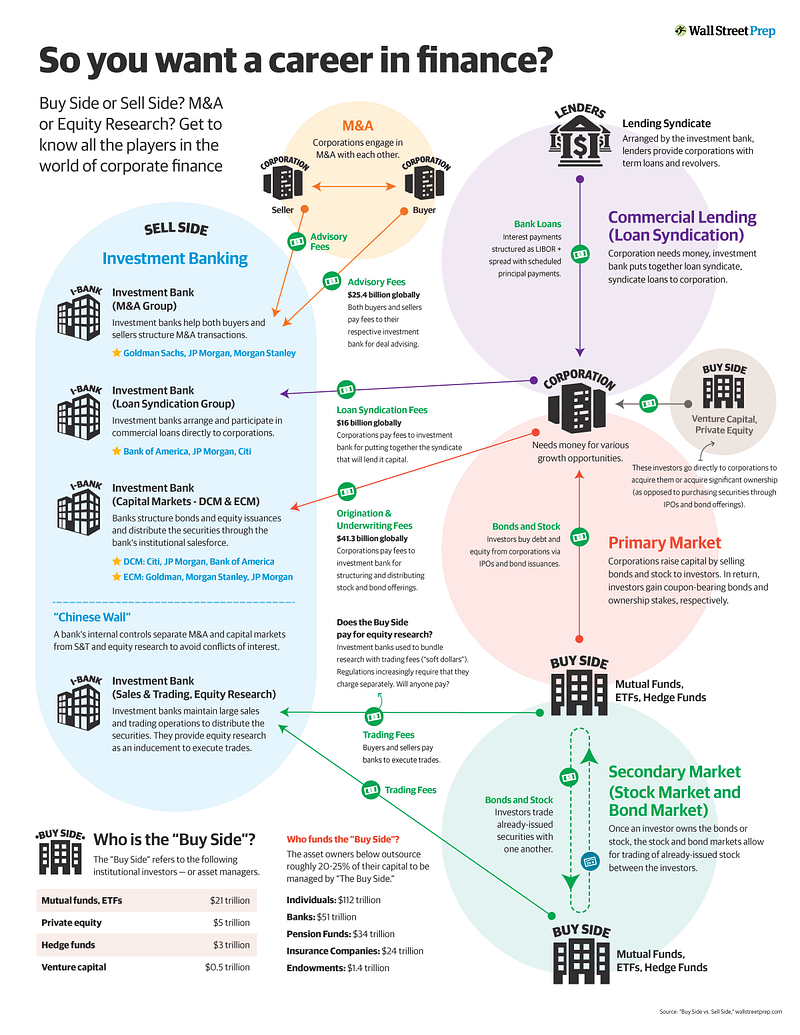

Corporate finance is a key pillar on which modern markets and economies have been built. And this complex ecosystem consists of a number of important sectors, which can lead to lucrative career avenues. Today’s featured infographic (above) by Wall Street Prep — from lending to investment banking, and private equity to hedge funds, breaks down the key finance careers and paths that people can take.

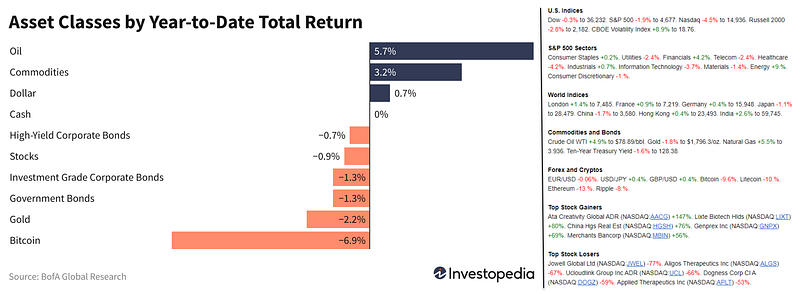

And finally, before moving on to some other statistics, here are the weekly & YTD numbers from various markets and different assets (Figure 1).

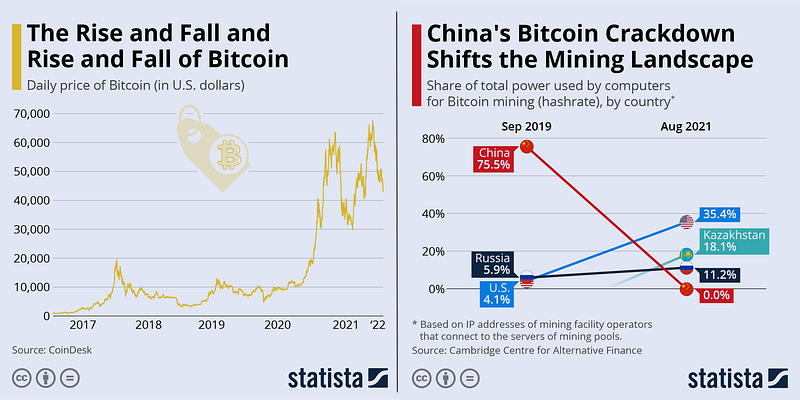

Rise & Fall of Bitcoin

Despite being the biggest and most significant cryptocurrency, Bitcoin is still famously susceptible to dramatic rises proceeded by equally rapid falls. Having surged to an all-time high of over $60 thousand in April 2021, Bitcoin plunged to around the $30 thousand mark at the end of July. Instability and crypto go hand in hand though, and the Bitcoin roller coaster raced skyward again soon after, with the record-breaking price of over $67k hitting in early November. The yo-yo gave in to gravity again at the beginning of 2022, fueled largely by the political unrest and protests in Kazakhstan and the subsequent internet shutdown. What does the situation in Kazakhstan have to do with Bitcoin? Since China’s crackdown on the currency, its neighbor has risen to become the second biggest player in the Bitcoin mining landscape, accounting for 18.1% (Figure 2) of all global computing power used for the activity.

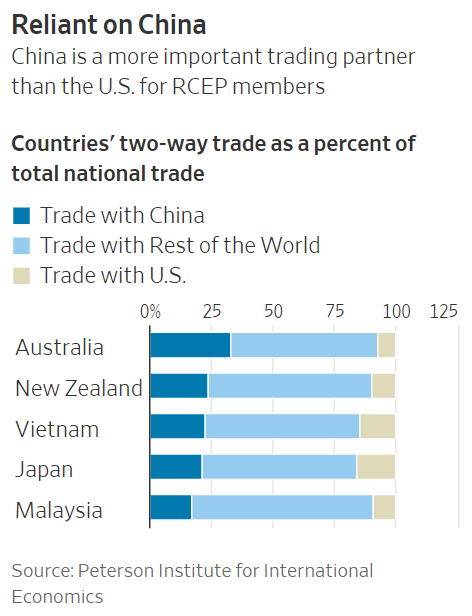

China’s Trading Partners

US allies in the Asia-Pacific region like Australia and Japan trade more with China than with the US (Figure 3). Their ties with China will likely strengthen now that the new Regional Comprehensive Economic Partnership (RCEP), which will “eventually eliminate 90% of tariffs on commerce among its 15 member countries” (not including the US), has gone into effect. The agreement could have important implications not only for boosting trade but also for strengthening supply chains in the region.

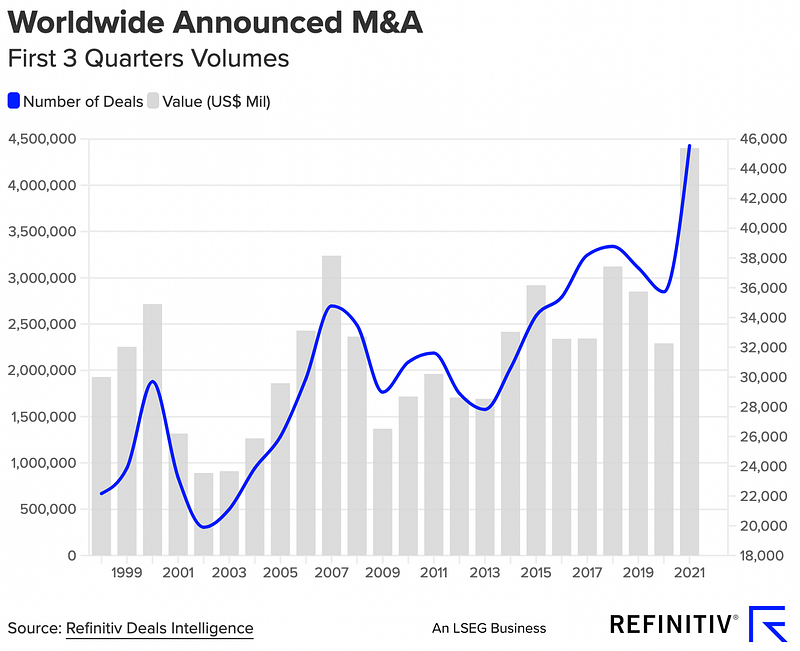

Record Year for M&A

2021 turned out to be a record year for global mergers and acquisitions (M&A), with a record 1,047 deals valued at over $100 million, according to a report by Willis Towers Watson (Figure 4). And researchers say they don’t expect the activity to slow down anytime soon. Last year’s M&A boom was the largest on record since Willis Towers Watson started keeping records in 2008, just before the financial crisis. By comparison, there were only 674 M&A deals in 2020 worth $100 million or more.

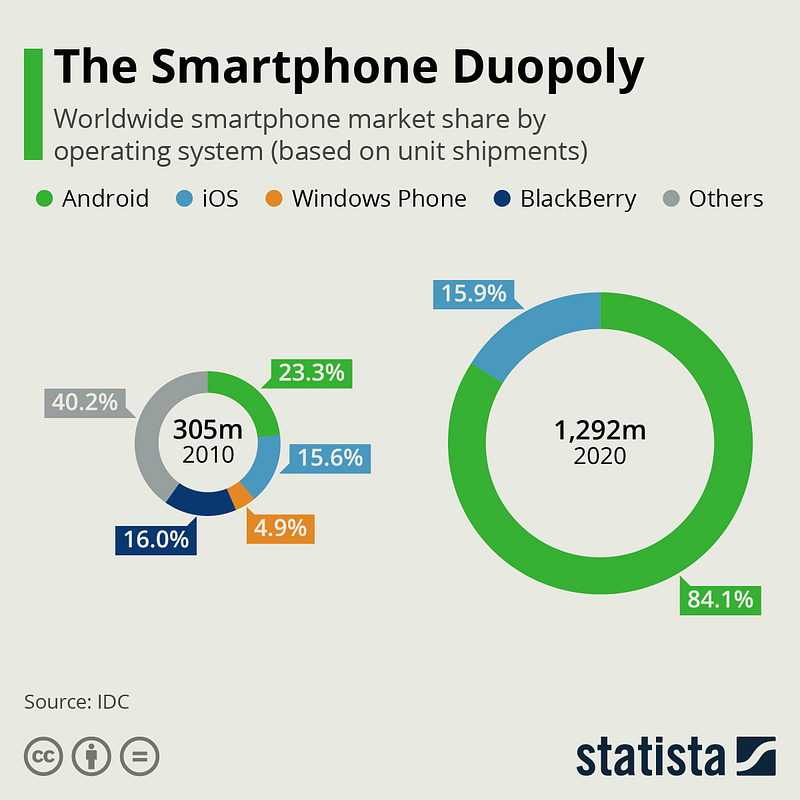

Smartphone Duopoly

Having started out as a multi-platform market, the smartphone landscape has effectively turned into a duopoly in recent years, after Apple’s iOS and Google’s Android crowded out any other platform including Microsoft’s Windows Phone, BlackBerry OS and Samsung’s mobile operating system called Bada. According to IDC (Figure 5), Android devices accounted for 84.1% of global smartphone shipments in 2020, with Apple’s iOS accounting for the remaining 15.9%. In 2010, the combined market share of Android and iOS was below 40%, with Nokia, Microsoft, BlackBerry and others sharing the rest of the market.

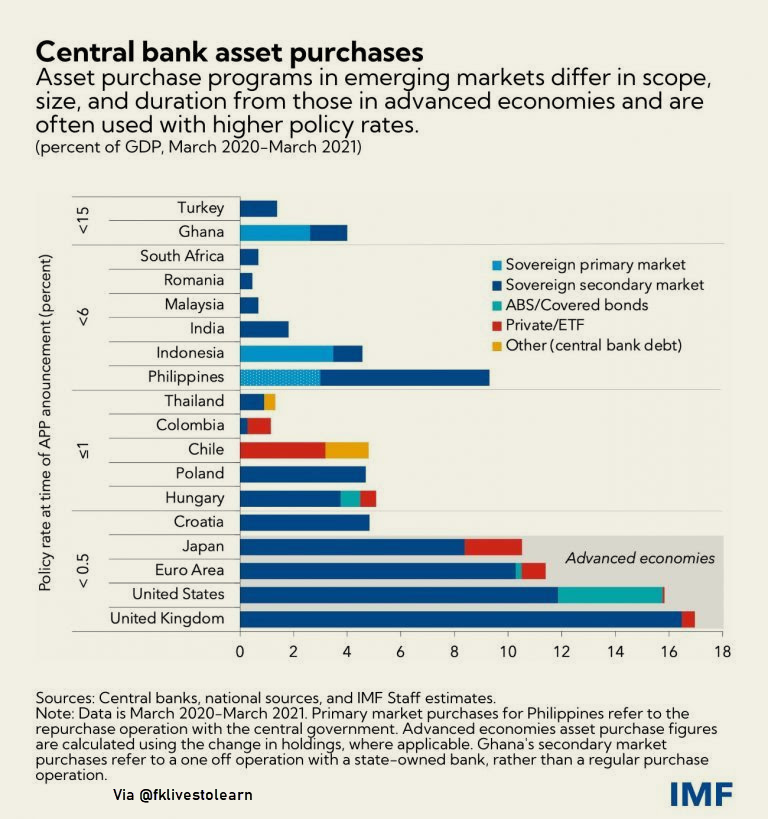

Central Bank Asset Purchases

Central banks in many emerging markets and developing economies have been reluctant to use asset purchases in past crises for fear of engendering a market backlash. As it turned out, targeted asset purchases in these countries during the COVID crisis helped reduce financial market (Figure 6) stresses without precipitating noticeable capital outflow or exchange rate pressures. This overall positive experience suggests that these central banks will also consider asset purchases in future episodes of market turbulence, as discussed in a recent Global Financial Stability Report.

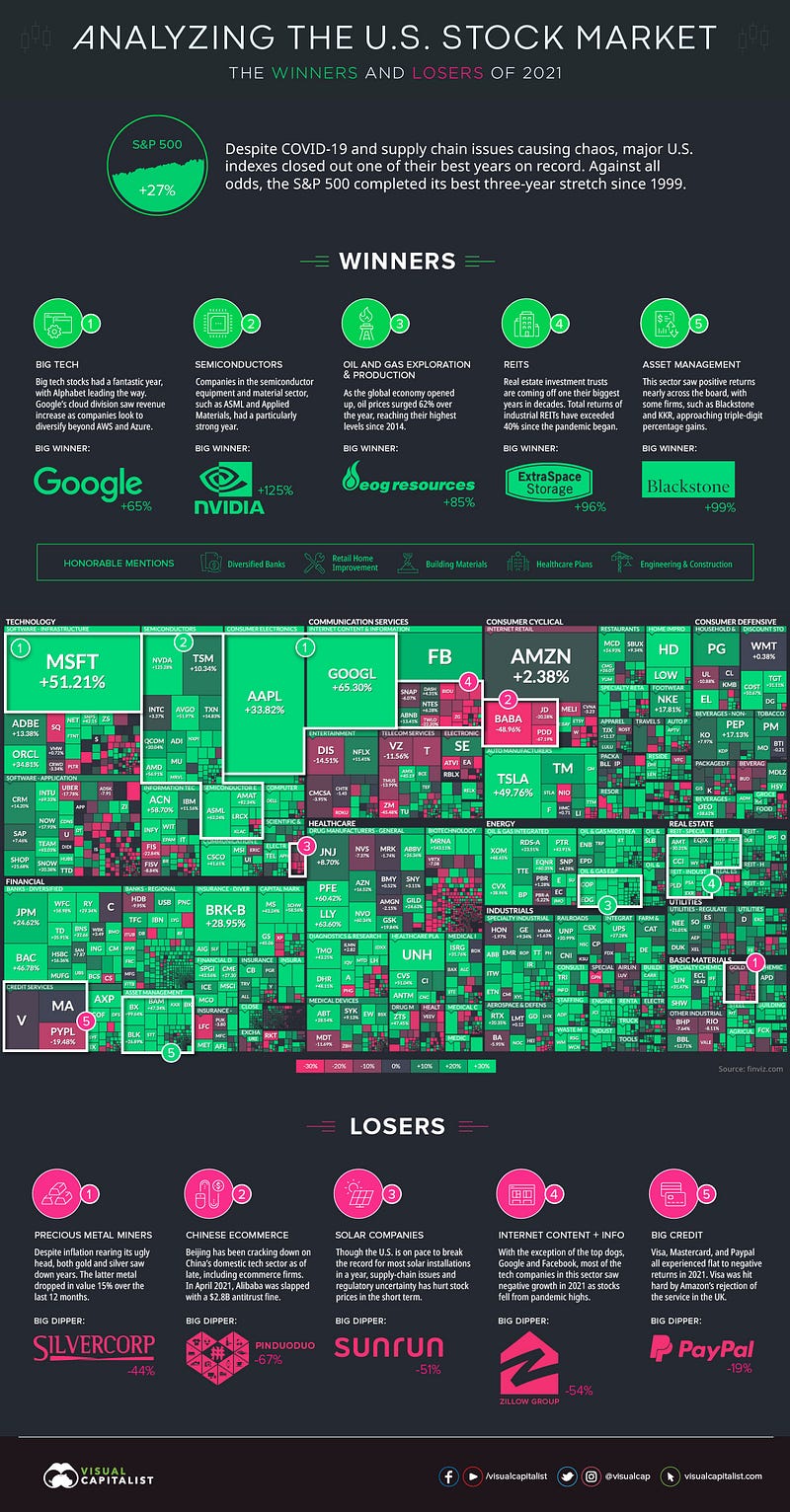

Winners & Losers of U.S Stocks in 2021

It was another eventful year — and while it may not quite compare to the pandemonium experienced in 2020, it was still jam-packed with market-moving events. This visualization (Figure 7) uses an augmented screenshot of the FinViz treemap, showing the final numbers posted for major U.S.-listed companies, sorted by sector and industry. Here are the big beneficiaries of last year, along with those that got left behind.

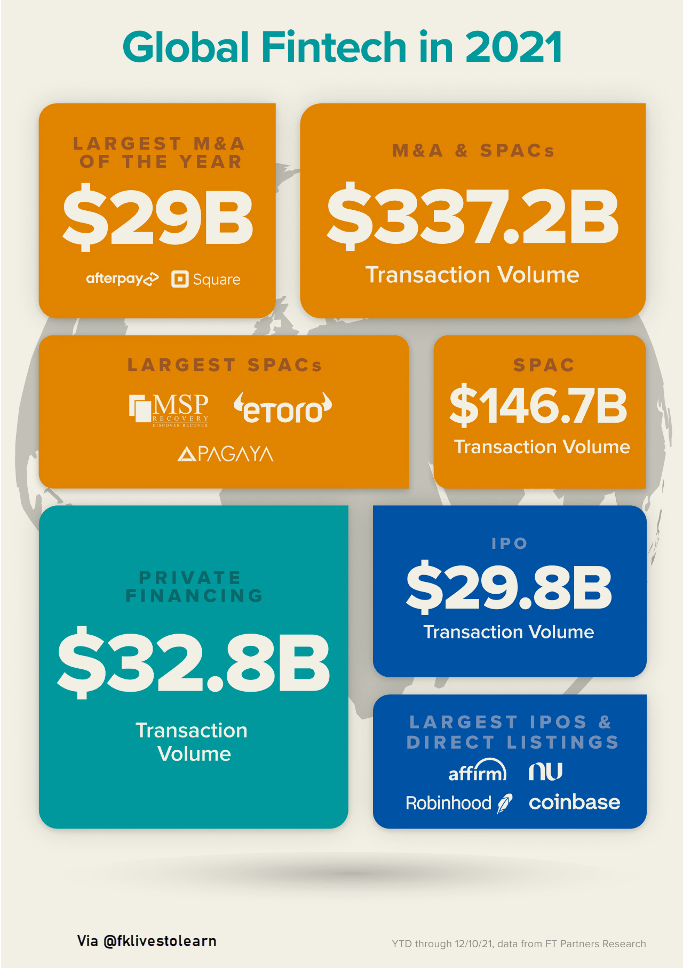

Fintech Distribution

It has been a titanic year for “traditional” fintech. The last decade of storytelling, hustle, venture investment, and anxiety had finally burst through into billions and billions of enterprise value in the public markets (Figure 8). We saw, for the first time, into essentially every single “democratizing finance” business model imagined by entrepreneurs in a standardized, SEC filing format. We saw the headline Coinbase, Robinhood, and Transferwise IPOs bring to market financial companies that don’t dance like banks, minting fintech billionaires in the process. The PayPal mafia is joined by dozens, if not hundreds, of new fintech super angels, who will fund the next pass at assailing orthodox market structures. Capital will only become more available for the space, despite a mind-boggling $30+ billion of venture investment in 2021.

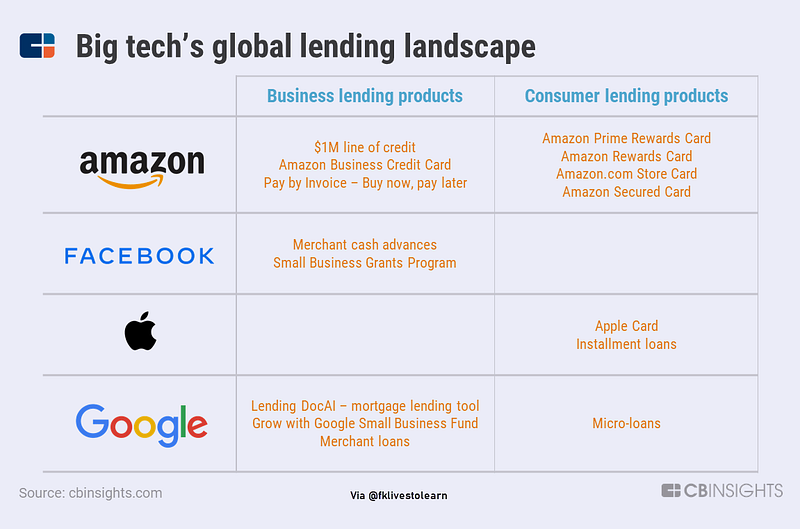

Big Tech’s Global Lending Landscape

Big tech companies are moving more and more into financial services. After last year’s payments push, big tech companies are now turning their attention to lending (Figure 9). Amazon, Facebook, and Google’s strategies focus on business lending — offering capital to the merchants, small businesses, or enterprises that they often already provide other services to. Meanwhile, Apple is leaning on its sticky products and loyal customer base to offer consumer lending products like “buy now, pay later” (BNPL) options and credit cards. Lending could be a lucrative opportunity for big tech, with the global SMB lending market alone estimated to be worth $3.4T by 2022. With extensive amounts of data on merchant business operations and consumer spending, tech giants are well-placed to make inroads with lending products and train algorithms to predict creditworthiness.

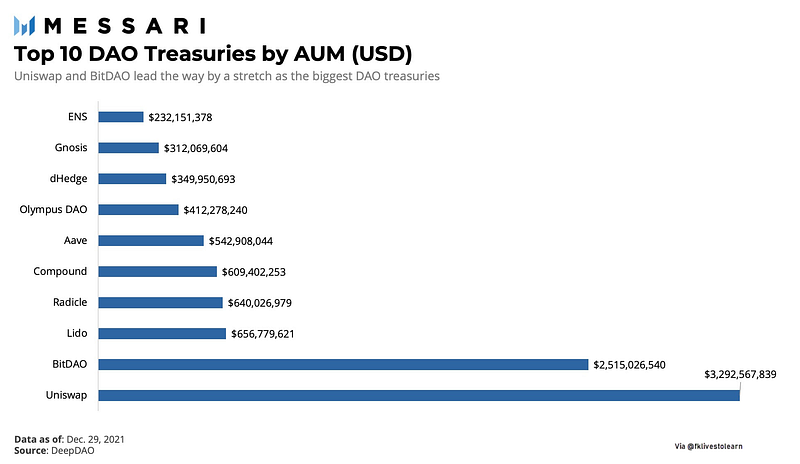

Top 10 DAO Treasuries

BitDAO launched August 3, 2021, and although it is quite new, it is one of the largest DAOs by treasury size with about $2.5B in assets under management (AUM, Figure 10). The grand vision for BitDAO is to support the growth of open finance and help develop decentralized, tokenized economies. The DAO was started by Bybit, which is a top derivatives exchange based out of Singapore. It launched in 2018 in order to compete against BitMEX in areas where it lacked. Bybit is currently not available for usage in the U.S. or Canada as with other perpetual and future exchange protocols. Uniswap remains the leader of the pack.

Market Humor: Investors Rotate Out Of High-Growth Tech Stocks To Start Off 2022!

Previous Edition of GBW

Read more stories like this and others by Faisal Khan on Medium.

Stay informed with the content that matters — Join my weekly Newsletter