WEEKLY BUSINESS ROUNDUP

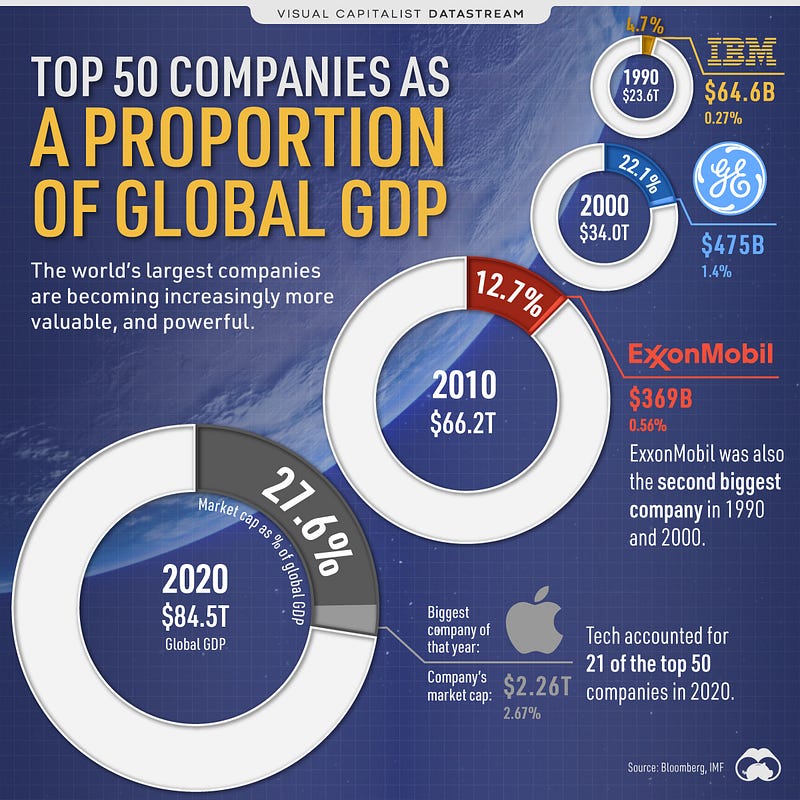

Global Business Week: Top 50 Companies as a Proportion of World GDP

The state of Financial markets & Economies, Weekly Charts, Business Trends & Statistics

After a massive sell-off to begin the week last Monday, the major U.S. averages reached new heights as they posted four straight sessions of gains. The Dow, S&P 500, and Nasdaq all closed at all-time highs, with the Dow finishing above 35,000 for the first time ever — bringing its 2021 gain to 14%, and rising 1% for the week. The S&P 500 rose 2% for the week and the Nasdaq Composite added 2.8%. The 10-year Treasury yield rebounded to 1.29% on Friday, easing concerns about the economy.

The change in sentiment from the beginning of the week, when worries about the spread of the Delta COVID-19 variant sent markets plunging, can be seen in the volatility index (VIX). After soaring Monday, VIX quickly fell from the peak and then declined steadily throughout the week. Next week is jam-packed with earnings as major companies across sectors of the economy report quarterly earnings — including the big techs. The U.S. Federal Open Market Committee (FOMC) also announces interest rate and monetary policy decisions.

Greenback continued to firm on a weekly basis but remained relatively flat on Friday. The benchmark dollar index (DXY) closed @ 92.91 and remains bid ahead of the FOMC rate decision in the coming week. Lingering inflation fears is keeping the USD bulls afloat. With the latest flash PMI data from IHS Markit echoing inflation risk, this could be helping boost the US Dollar, as more evidence of persistent price pressures rekindles speculation around when the Federal Reserve will taper asset purchases.

Elon Musk was at it again — this time talking in favor of cryptos and bringing in a much-needed relief for the digital currencies. Cryptocurrencies regained their footing after Elon Musk, whose statements have helped drive rallies in the market before, said Tesla will accept Bitcoin again for vehicle purchases, and added that he also owns Ethereum. Bitcoin prices climbed 6% on the news, while Ethereum rose 8%. At the time of writing, BTC was trading over $34.3k whole ETH was charging above $2,180 — before previously dropping to below $30k and $1,800 respectively.

Today’s featured infographic (above) highlights how the world’s top 50 companies have become increasingly more valuable, and more powerful, over time. As global GDP has grown over the last four decades, from $23.6 trillion in 1990 to $84.5 trillion in 2020, the proportional share of the world’s top companies by market capitalization has grown over 5x. You might also be interested in reading about the 50 Most Innovative Companies in the World.

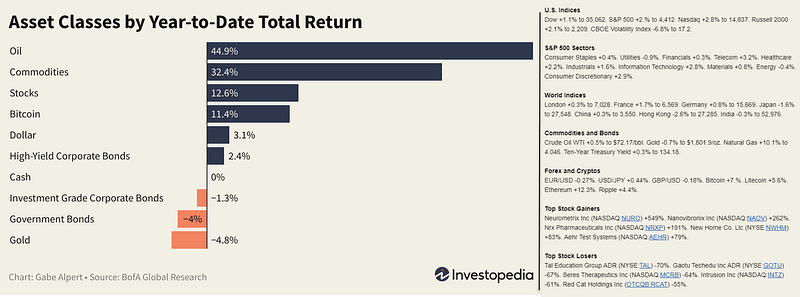

And finally, before moving on to some other statistics, here are the weekly & YTD numbers from various markets and different assets (Figure 1).

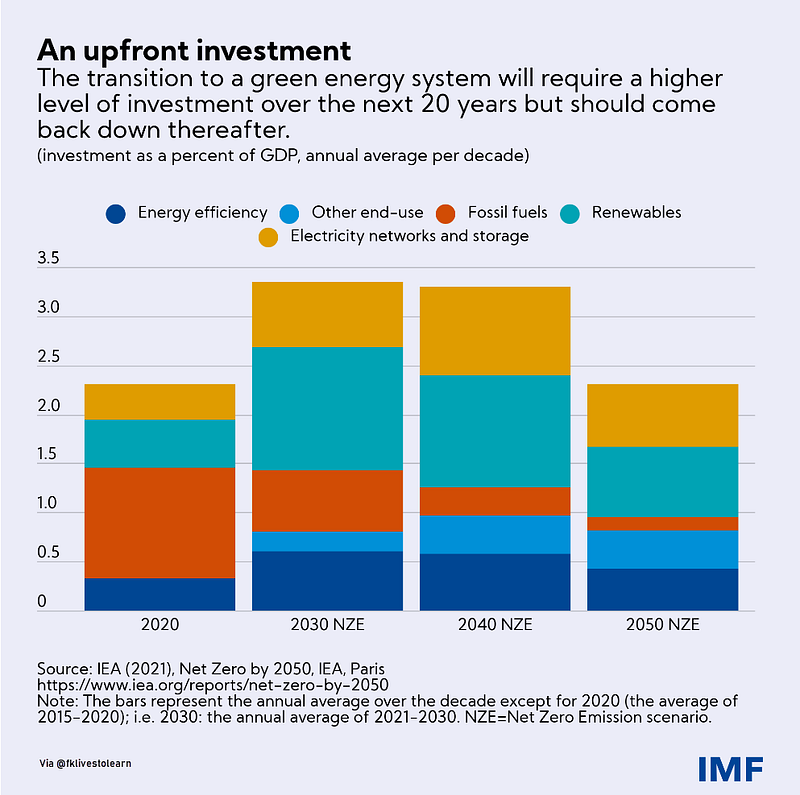

Investment for a Green Energy System

An estimated additional $6 to 10 trillion in global investments, both public and private, are needed in the next decade to mitigate climate change. This amounts to a cumulative 6–10% of annual global GDP. According to International Energy Agency data, about 30% of additional investment, on average globally, is expected to come from public sources — that is a cumulative 2–3% of annual GDP for the decade 2021 to 2030. The remaining 70% would be private (Figure 2). On the public side, fiscal packages from governments to support recovery from the COVID-19 pandemic are a unique opportunity to invest in a transition to a low-carbon economy.

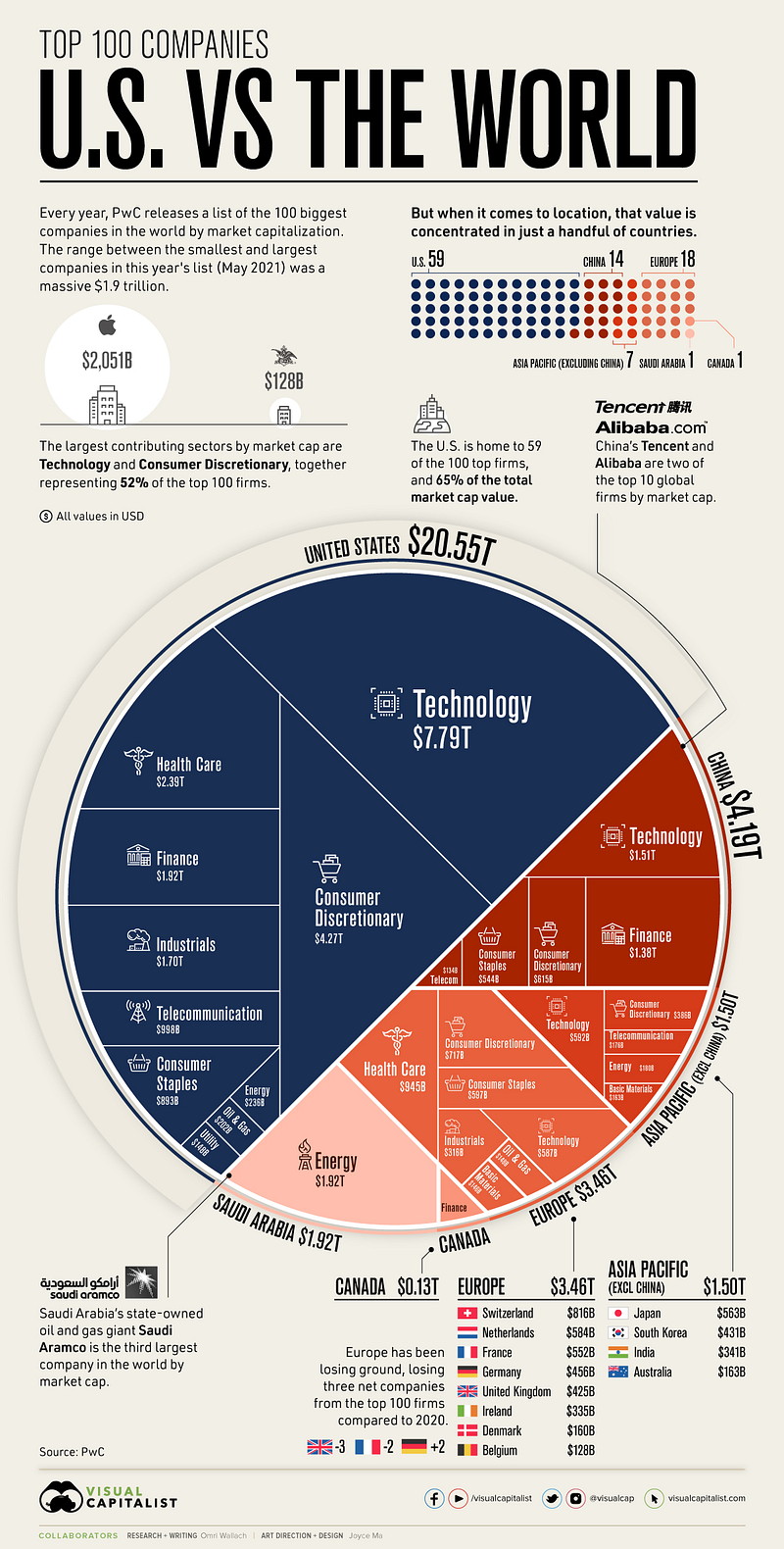

Top 100 Global Companies by Country

How do the top 100 companies of the world stack up? This infographic below (Figure 3) pulls data from PwC’s annual ranking of the world’s largest companies, using market capitalization data from May 2021. Throughout the 20th century and before globalization reached its current peaks, American companies made the country an economic powerhouse and the source of a majority of global market value. But even as countries like China have made headway with multi-billion dollar companies of their own, and the market’s most important sectors have shifted, the U.S. has managed to stay on top.

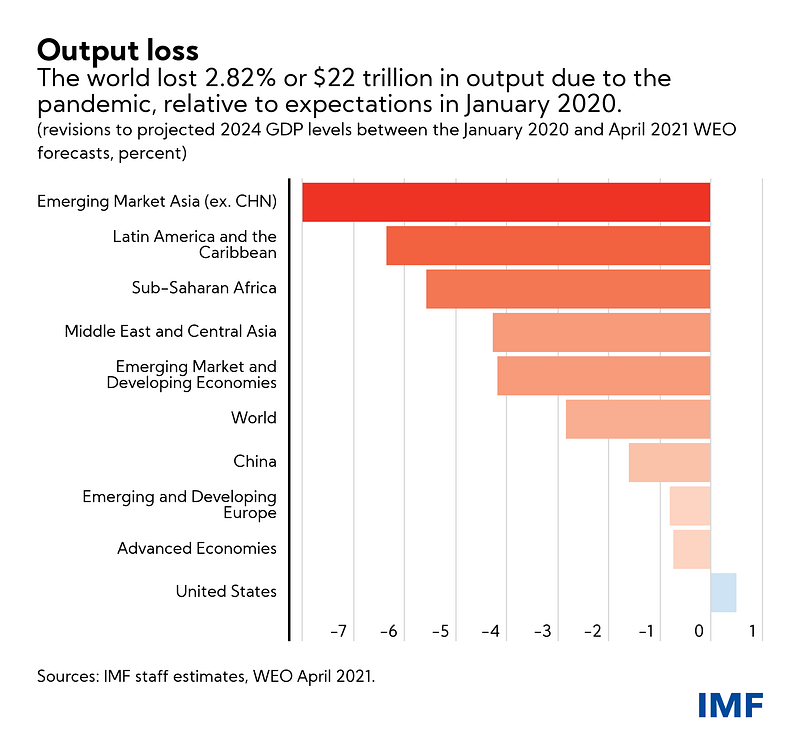

Global Output Loss due to Pandemic

Since March 2020, governments have spent $16 trillion providing fiscal support amid the pandemic, and global central banks have increased their balance sheets by a combined $7.5 trillion. Deficits are the highest they have been since World War II and central banks have provided more liquidity in the past year than in the past 10 years combined. This was absolutely necessary — IMF research indicates that if policymakers had not acted, last year’s recession, which was the worst peacetime recession since the Great Depression, would have been three times worse. Nevertheless, the world lost $22 trillion in output as a result of COVID-19 (Figure 4), relative to what the IMF expected in January 2020. The same energy that is being put into vaccination and plans for recovery spending also needs to be put into growth measures to make up for this lost output.

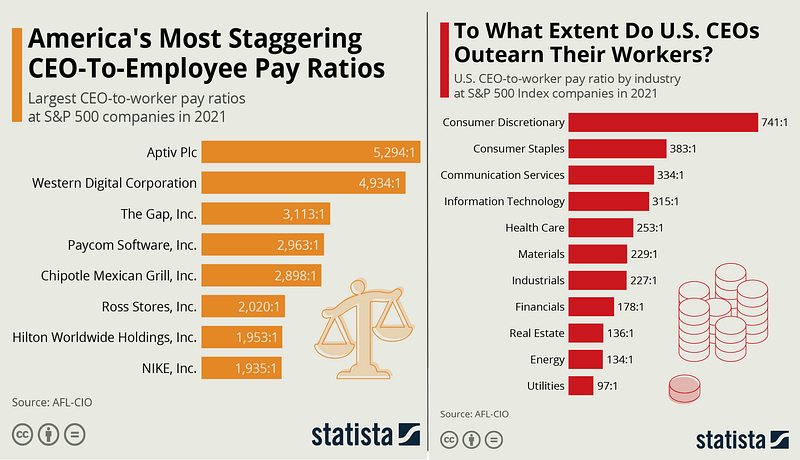

American Salary Discrepancies

The average S&P 500 CEO made $15.5 million last year, 299 times the pay of the median worker. That’s according to an annual report from America’s largest labor union, AFL-CIO, which is widely cited as a measure of workforce equality (Figure 5). This year’s figure represents an increase on the 264-to-1 ratio from 2019 and it came amid devastating job losses due to the Covid-19 pandemic. On average, S&P 500 bosses saw their pay packets grow by $700,000 last year and $2.6 million over the past decade. According to AFL-CIO, the ratio of CEO-to-worker pay is important because “a higher pay ratio could be a sign that companies suffer from a winner-take-all philosophy where executives reap the lion’s share of compensation”. It adds that “a lower pay ratio could indicate the companies that are dedicated to creating high-wage jobs and investing in their employees for the company’s long-term health”.

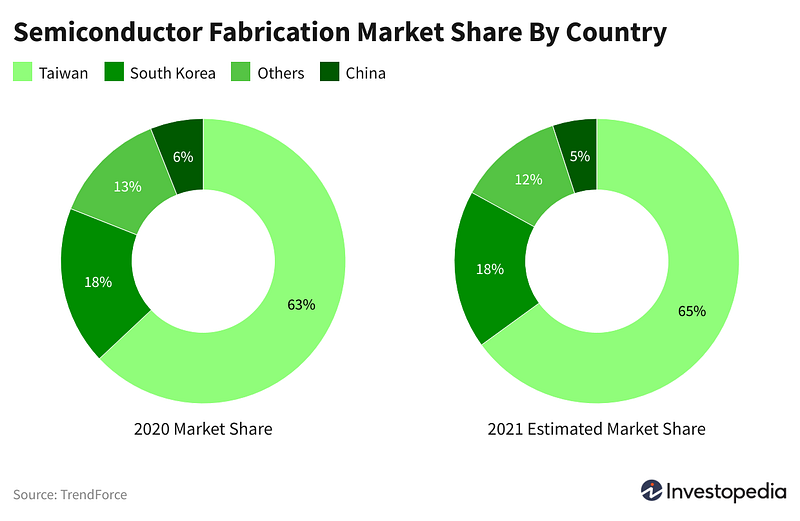

Global Semiconductor Market Share

Taiwan controls nearly two-thirds of the global semiconductor fabrication market, and has only increased its market share in the last year (Figure 6), but has struggled to meet demand amid a difficult COVID-19 vaccine rollout and a jump in cases, leading to a global shortage of chips. U.S administration is developing plans to quickly spend $52 billion to deal with semiconductor chip shortages if Congress passes a bill funding such efforts. Mainland Chinese companies currently control between 5% and 6% of the global semiconductor fabrication market, and they’re trying to increase that share by buying foreign fabricators.

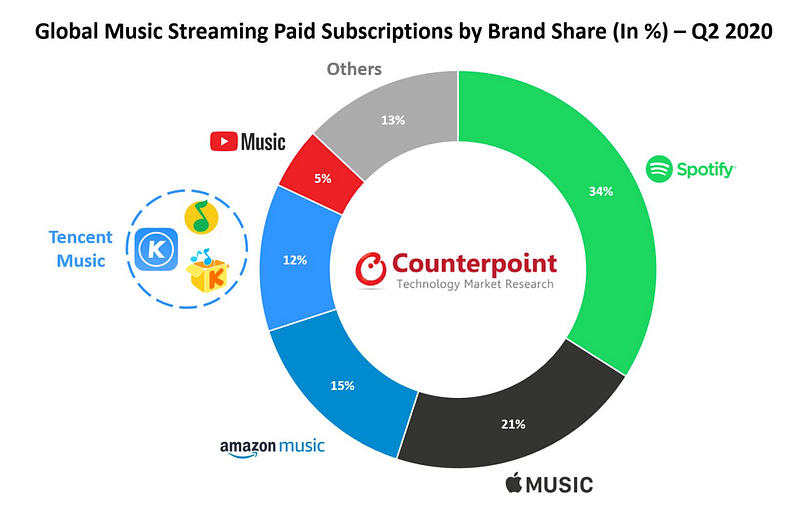

Global Music Streaming Giants

Streaming is now, by far, the most prevalent medium of consuming music. A concoction of increased smartphone usage, greater availability of streaming services, and the reducing cost of data have all helped drive this migration to digital distribution and consumption. This is reflected in the growing revenues of music streaming and is projected to increase in the future (Figure 7).

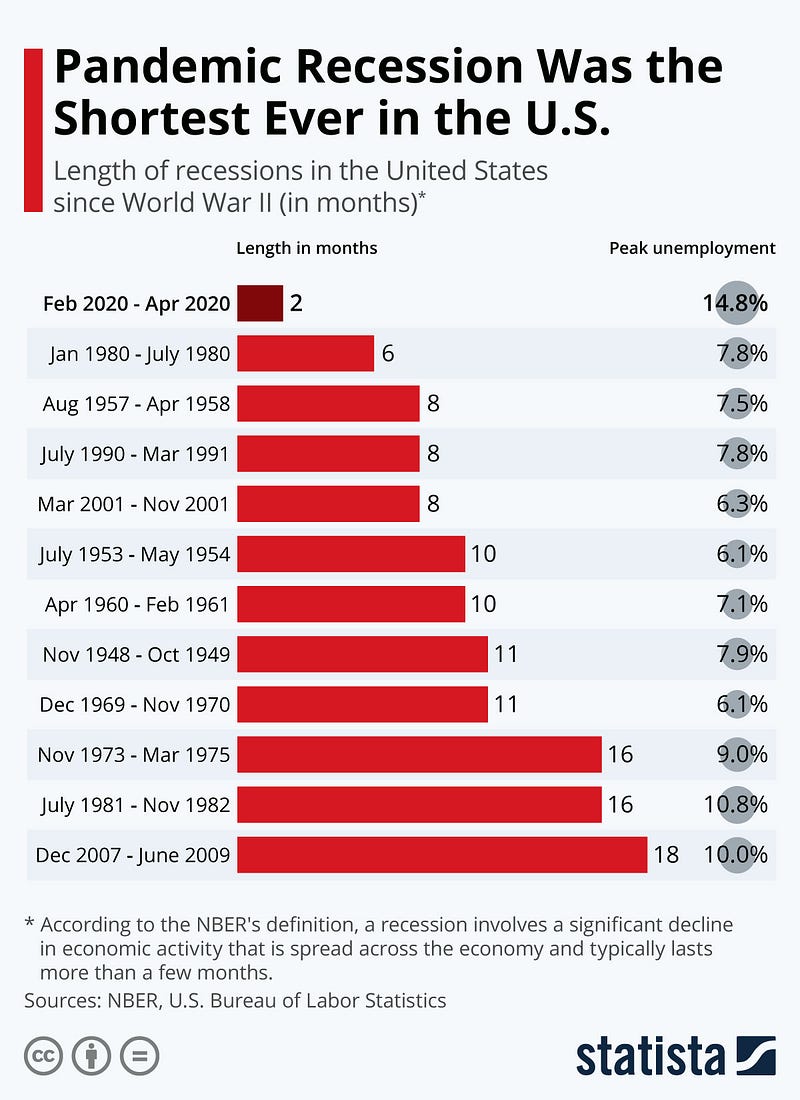

Shortest Recession Ever for the U.S

While the COVID-19 pandemic is far from over, as rising case numbers in various countries sadly illustrate, the recession it brought on to the U.S. economy officially is. And for quite some time, as the official chronicler of U.S. business cycles announced recently. According to an official statement from the Business Cycle Dating Committee of the National Bureau of Economic Research (NBER), the U.S. economy bottomed out in April 2020, just two months from its previous peak in February 2020. According to the NBER’s conventions for chronicling economic cycles, a recession begins in the first month following a peak in economic activity and ends in the month of the subsequent trough. In this case, that means the COVID-19 recession only lasted for two months, making it the shortest on record (Figure 8).

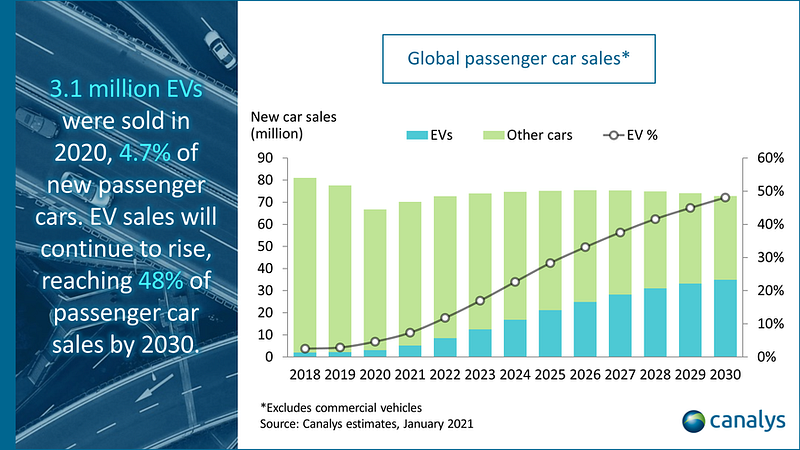

EVs Sales Continue to Rise Globally

Add Mercedes-Benz to the list of carmakers who are making a complete switch to electric vehicles (EVs). The luxury brand owned by Daimler announced it will be all-electric by the end of the decade, where market conditions allow. The company said by 2025 all of its new vehicle platforms will be electric-only, and customers will be able to choose an electric version of every vehicle it makes. Mercedes-Benz plans to spend some $47 billion from 2022 to 2030 to produce battery-driven vehicles. Daimler and Mercedes-Benz CEO Ola Källenius said the shift to EVs is picking up speed (Figure 9), especially in the luxury segment, and the “tipping point” is near.

Market Humor: Stocks’ Roller Coaster Ride

Previous Edition of GBW