WEEKLY BUSINESS ROUNDUP

Global Business Week: Investing in the future of Agriculture & Food

The state of Financial markets & Economies, Weekly Charts, Business Trends & Statistics

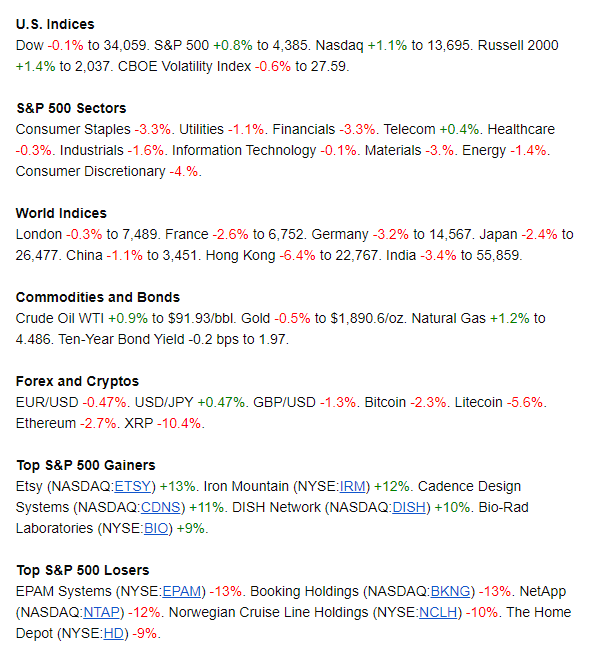

Financial markets went on a roller-coaster ride on Thursday as traders monitored the latest happenings in Ukraine. Buy the dip market maxim has been in play since the COVID pandemic started when a steep selloff was followed by an unprecedented amount of buying that sent indices to continuous record highs. Since then, investors have been on the hunt for bargains, or so-called oversold conditions, while algo trading has magnified the sentiment and contributed to big reversals. WTI crude oil surged to more than $100 a barrel for the first time since 2014, before dropping back to trade near the $90 level.

U.S. equity markets surged, rising for a second straight day Friday, after this week’s sell-off following Russia’s invasion of Ukraine. For the Dow, it was the biggest single-day advance since November 2020. The S&P 500 closed the week with a 0.8% gain after falling as much as 5.5%, the Nasdaq Composite increased 1.1% after plunging as much as 7%, the Dow Jones nearly broke even after losing 5.3% midweek. The shock and uncertainty of war in Europe could discourage the Federal Reserve from being aggressive about hiking interest rates, which had been weighing on stocks before Russia’s invasion.

It was a chaotic week across global markets. This week’s geopolitical items have brought that into question, to some degree, as hiking aggressively into a potential global conflict could be a recipe for disaster. Just last week, it seemed like a 50 basis point rate hike in March was probabilistic. This week, it looks downright unlikely, helped along by some dovish Fed-speak along the way. This has also carried an impact on the Dollar Index with a massive move that was partially reversed to end the day on Friday — closing DXY @ 96.54, before touching a high of 97.74 earlier.

Bearish consolidation has ensued in cryptocurrencies ever since the recent highs reached in digital assets. Recent geopolitical tensions have rocked the financial markets and cryptos’ price action has replicated the risk moves in Equities. Bitcoin is back below $40k, now trading just above $38k — while Ethereum has slid close to $2600 at the time of publishing. Key central bank decisions in the coming days and weeks would define how the markets behave going forward and a slightly less hawkish approach might benefit the cryptocurrencies going forward.

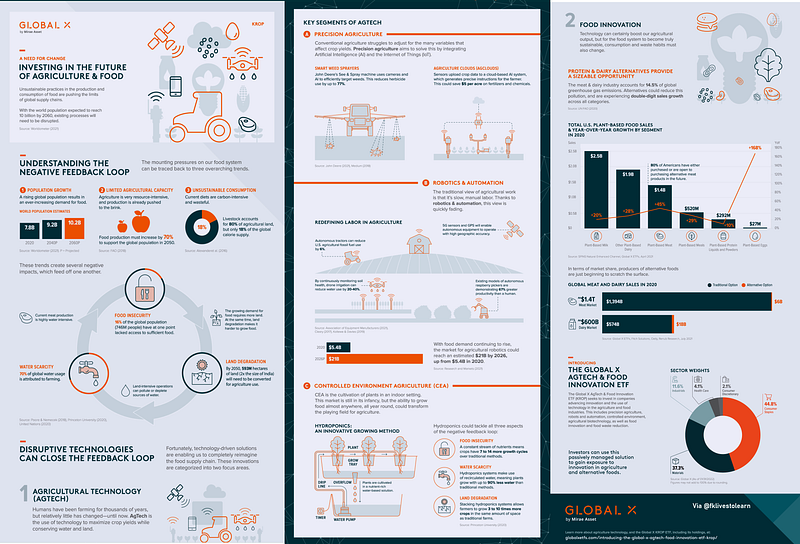

The global food system is under immense pressure due to three overarching trends — population growth, limited capacity & unsustainability. Agriculture technology (AgTech) and food innovation are emerging as two possible solutions. This infographic from Global X ETFs (above) explains both.

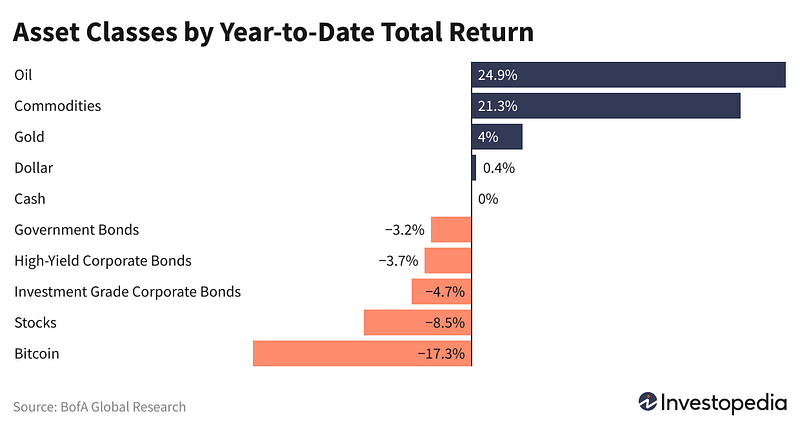

And finally, before moving on to some other statistics, here are the weekly & YTD numbers from various markets and different assets (Figure 1).

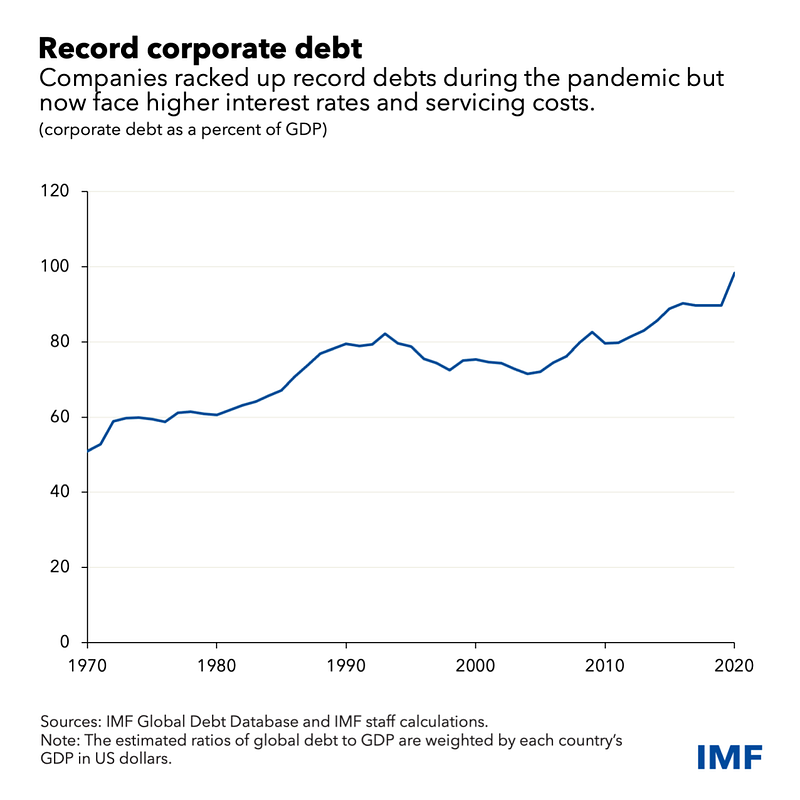

Record Corporate Debt

Companies entered the COVID-19 crisis with record debts they racked up after the global financial crisis when interest rates were low. Corporate debt stood at $83 trillion, or 98% of the world’s gross domestic product, at the end of 2020. Advanced economies and China accounted for 90% of the $8.9 trillion increase in 2020 (Figure 2). Now that central banks are raising rates to check inflation, firms’ debt servicing costs will increase. Corporate vulnerabilities will be exposed as governments scale back the fiscal support that they extended to stricken firms at the height of the crisis.

Governments face difficult decisions as they manage these risks to economic recovery. They may need to continue providing financial support to firms that can recover (but cannot raise the private financing to do so) while withdrawing support from firms that are so badly scarred that they should be restructured or liquidated. Financial support should become more focused amid shrinking fiscal space. Effective insolvency systems make economies more resilient, productive, and competitive. Shoring up these systems is critical as there are shortcomings in many important areas at present and countries may need to tackle many cases at once. There is not much time to prepare.

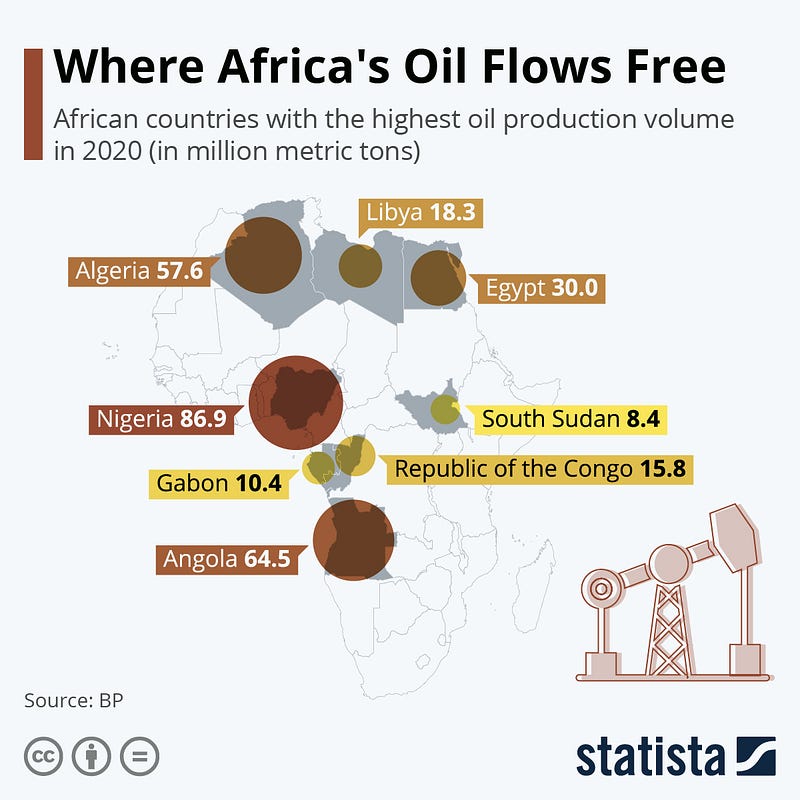

Africa's Oil Flows

While the move away from fossil fuels towards more sustainable alternatives is well on the way in many industry sectors, the world as of now still relies heavily on crude oil for the production of different fuel types, plastics & wax. In 2020 alone, countries around the world produced 4,165 million metric tons of oil. The continent of Africa was responsible for 327.3 million metric tons, netting it fifth place worldwide after the Middle East, North America, CIS & the Asia Pacific region including China. As our chart shows (Figure 3), its oil production hotspots are mainly situated in countries with coastlines, with Nigeria taking the top spot. According to data from BP’s yearly report, the Western African nation produced more than a quarter of the whole continent’s oil production, which translates to 86.9 million metric tons.

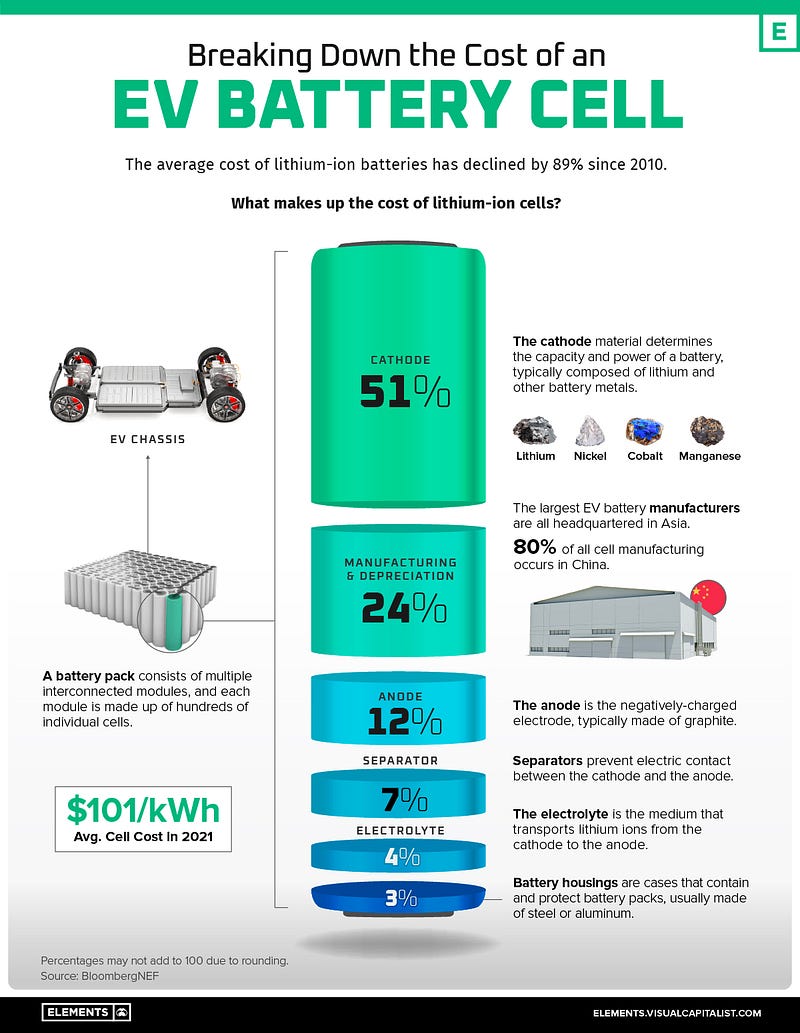

Cost of an EV Battery Cell

As electric vehicle (EV) battery prices keep dropping, the global supply of EVs and demand for their batteries are ramping up. Since 2010, the average price of a lithium-ion (Li-ion) EV battery pack has fallen from $1,200 per kilowatt-hour (kWh) to just $132/kWh in 2021 (Figure 4). Inside each EV battery pack are multiple interconnected modules made up of tens to hundreds of rechargeable Li-ion cells. Collectively, these cells make up roughly 77% of the total cost of an average battery pack or about $101/kWh.

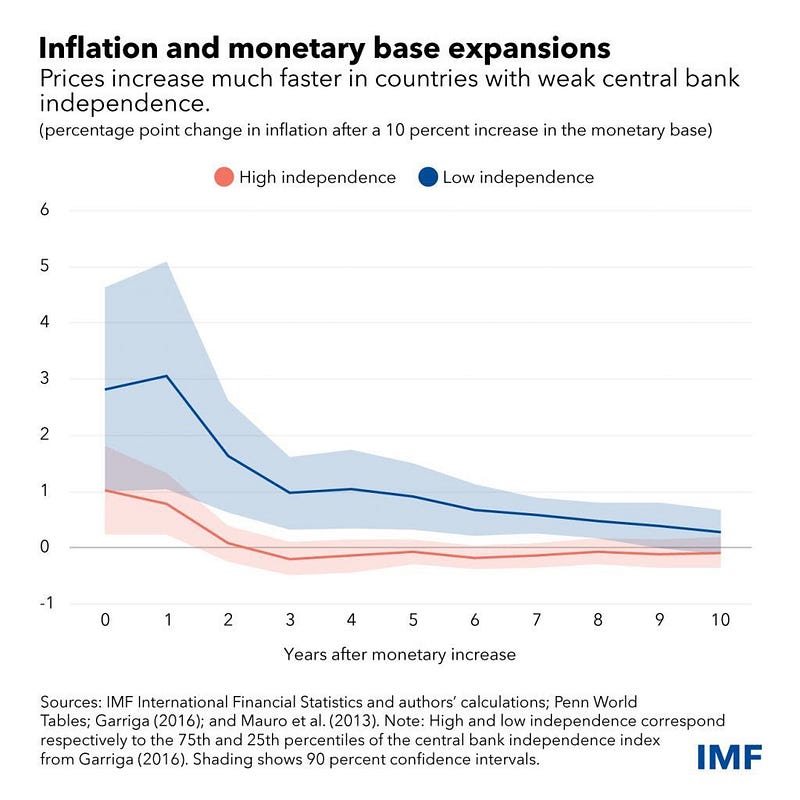

Inflation & Monetary Base Expansions

Most importantly, possible monetary finance operations should be decided exclusively and independently by central banks with the sole goal of ensuring economic stability. This is admittedly a difficult standard to achieve. A difficulty is seen by some as sufficient reason to ban monetary finance altogether. Indeed, in this context, departures from central bank independence can be very dangerous (Figure 5). History abounds with examples where the use of monetary finance under inappropriate circumstances had devastating effects on economies and livelihoods.

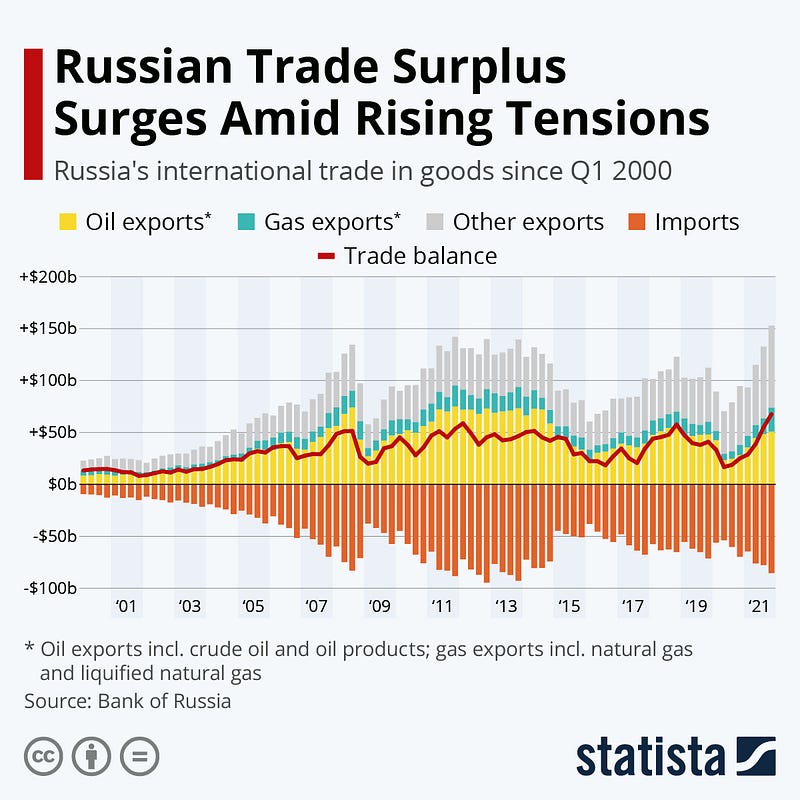

Russian Trade Surplus Surges

Amid rising tensions between Russia, Ukraine & the West, Russia’s oil and gas exports rebounded sharply in 2021. According to the Bank of Russia, crude oil exports climbed to $32 billion in the fourth quarter of 2021, the highest level since 2014. As a result of surging energy prices, the country’s total oil and gas exports, including oil products and liquified natural gas, exceeded $240 billion last year, up 60% from $150 billion in 2020, when energy prices had slumped at the onset of the Covid-19 pandemic. According to figures from the Russian Finance Ministry cited by Reuters, the oil price averaged $69 per barrel in 2021, up from around $40 in 2020. The average price of natural gas exported by Russia reached $277 per 1,000 cubic meters in Q3 2021, up from less than $100 in Q2 2020, amid the Covid crash. As the following chart shows (Figure 6), Russia’s merchandise trade surplus climbed to a record high of $67.6 billion in Q4 2021, despite the fact that the country’s imports also reached the highest level since 2013.

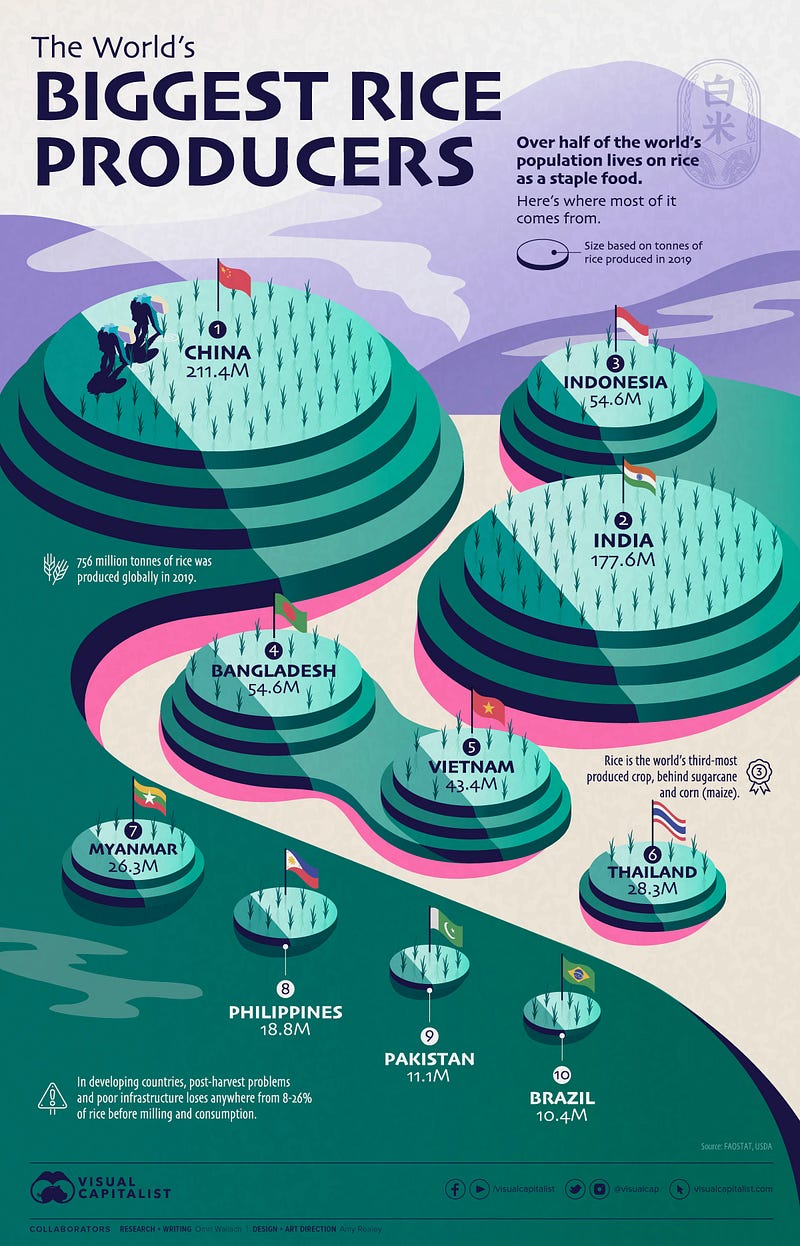

World’s Biggest Rice Producers

It’s hard to overstate the importance of rice to the world. As a staple food, over half of the global population depends on the crop as a major part of their diet. In fact, rice is considered a vital part of nutrition in much of Asia, Latin America, Africa, and the Caribbean, and is estimated to provide more than one-fifth of the calories consumed worldwide by humans. This infographic (Figure 7) highlights the world’s 10 biggest rice-producing countries, using 2019 production data from the UN’s FAOSTAT and the USDA.

Market Humor: Russia-Ukraine Headlines Trigger Market Volatility As Biden, Putin Plot Their Next Move!

Previous Edition of GBW

Read more stories like this and others by Faisal Khan on Medium.

Stay informed with the content that matters — Join my weekly Newsletter