WEEKLY BUSINESS ROUNDUP

Global Business Week: Global debt could go up to 265% of GDP by year-end

The state of Financial markets & Economies, Weekly Charts, Business Trends & Statistics

Although the U.S stock markets couldn’t close in the green for five days in a row, one of the most tumultuous week in the country’s political history has come to end. And while we have a winner from the hotly contested election, the uncertainty might last a little longer. For the markets, though, things might begin to settle down sooner rather than later and the litigation on elections is not expected to hold.

For the week, the S&P 500 and Nasdaq had jumped 7.3% and 9%, respectively, while the Dow rose 6.9%. S&P 500 in fact had the biggest election week gain since 1932 for all you record keepers. Outside the financial markets, the economies are of the world are flashing red signals as a raging pandemic throws a huge challenge for the upcoming U.S administration and the governments around the world.

After an initial whipsaw action on the eve of U.S elections, the dollar index has turned sharply lower, owing to the investors opting for riskier assets. Closing at 92.24 last Friday, it is perilously close to the previous low of 91.80 reached in early September. The expectation of another bumper stimulus package & further monetary easing might extend its weakness to new lows. The medium-term bearish trend has once again reinforced itself.

Bitcoin (BTC) has been ripping higher in the election week too. It has almost touched $16k and is now consolidating above the previous resistance, now turned support of $14k. The strong bullish undertone in the premier digital asset is pointing to further gains ahead. We might see BTC taking a stab at the next resistance level around $17.2k before another correction. Beyond that, it goes for an all-time high of 20k. Below $14k it would aim for $12.4k. For now, though, things looking really good for bitcoin & cryptos in general.

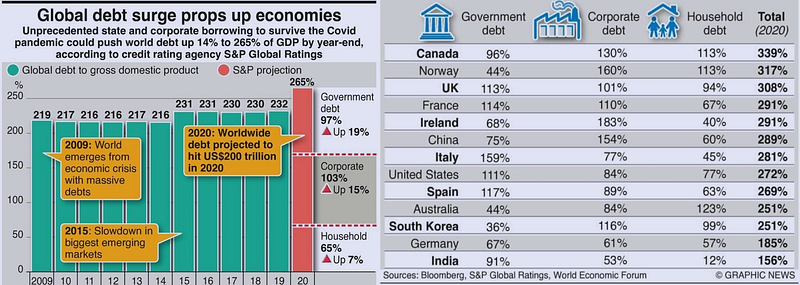

Today’s featured infographic (above) highlights the ballooning debts across the world as financial & monetary authorities opted for easing measures to prop up their economies. The global government debt is expected to jump to 265% of GDP in 2020, from 232% in 2019.

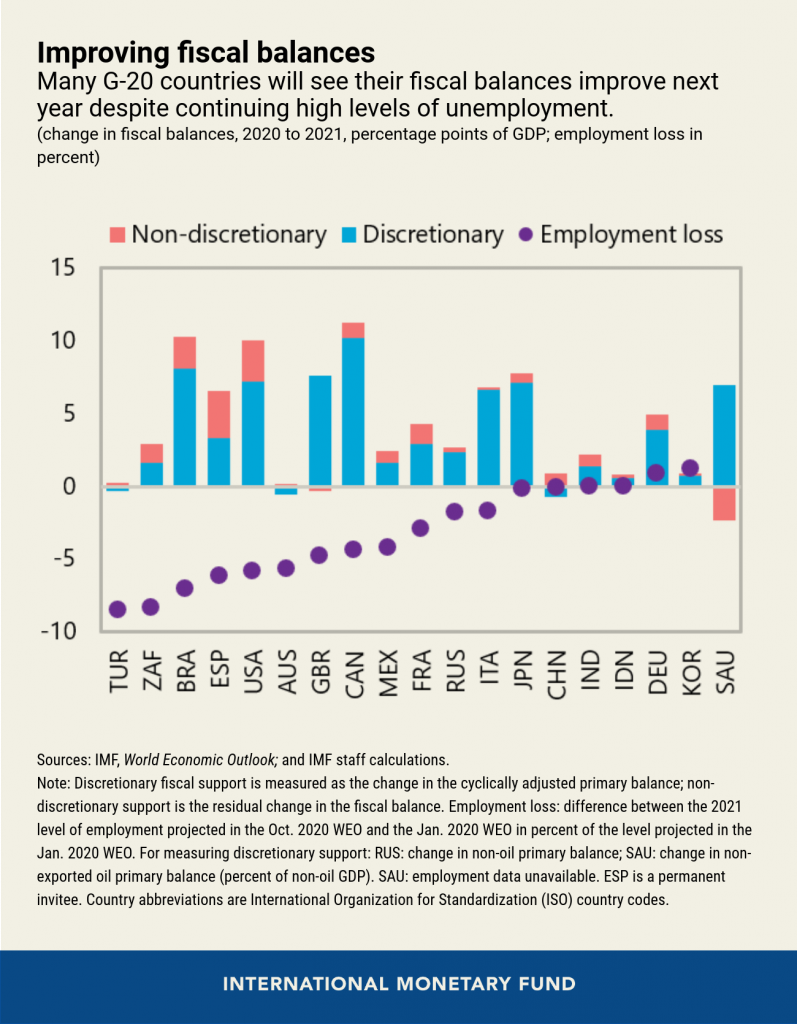

Improving Fiscal balances in 2021

Although big challenges lie ahead, Swift and unprecedented action by policymakers around the world has helped avert a bigger financial crisis. G20 alone has provided around US$11 trillion in necessary support to individuals, businesses, and the healthcare sector since the start of the pandemic. With COVID-19’s second wave in full swing and much of the financial support now gradually winding down, countries may need to prop up cash transfers to households, offer deferred tax payments or temporary loans to businesses that have expired or are set to expire by the end of this year.

The following analysis in IMF’s G20 Report on Strong, Sustainable, Balanced, and Inclusive Growth illustrates how fiscal deficits in almost all G20 economies are projected to shrink next year, based on announced budgets and current policies. In economies where deficits widened sharply this year, fiscal balances are now expected to narrow by more than 5% of GDP in 2021 (Figure 2).

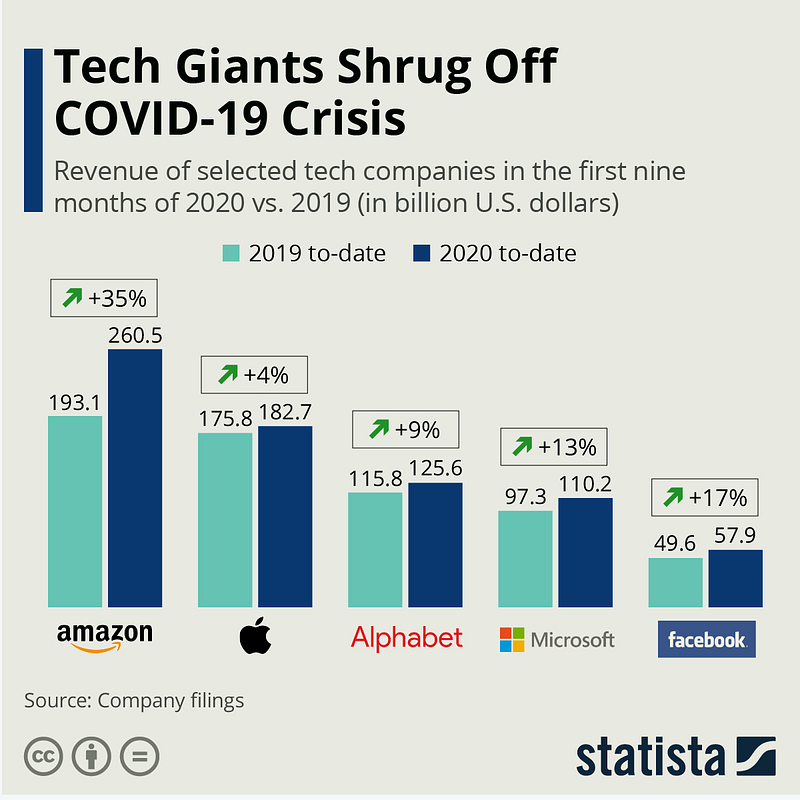

Tech Giants Shrug Off COVID-19 Crisis

While many industries like airlines, hotel chains, restaurants and millions of small businesses that are fighting for survival amid the COVID-19 pandemic, the world’s most prominent tech companies have remarkable resilience as they post staggering gains this year. Defying all odds, three out of five of the GAFAM group of companies (Google, Apple, Facebook, Amazon and Microsoft) posted double-digit revenue growth for the nine months of the current year (Figure 3). Amazon is the leader of the pack with 35% Y-o-Y gains, followed by Facebook, Microsoft, Google & Apple — posting 17%, 13%, 9%, and 4% respectively.

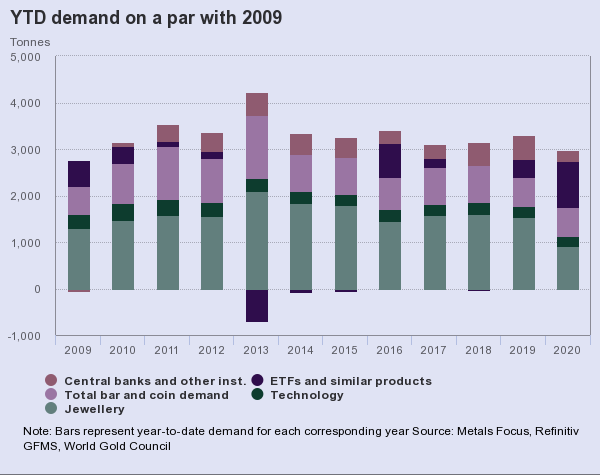

Global Gold demand drops

Global demand for gold dropped to 892.3 tonnes in Q3 — the lowest quarterly total since Q3 2009 and down 19% year over year, according to the World Gold Council. Year-to-date demand is 10% below 2019. As jewelry demand remained weak last quarter (-29% YoY), bar and coin demand strengthened (+49% YoY) and inflows of 272.5 tonnes took global holdings of gold ETFs to a new record of 3,880 tonnes. Asian-listed gold ETFs saw their highest ever reported quarterly inflows of 20.7 tonnes. Central banks were net sellers for the first time since 2010 (Figure 4).

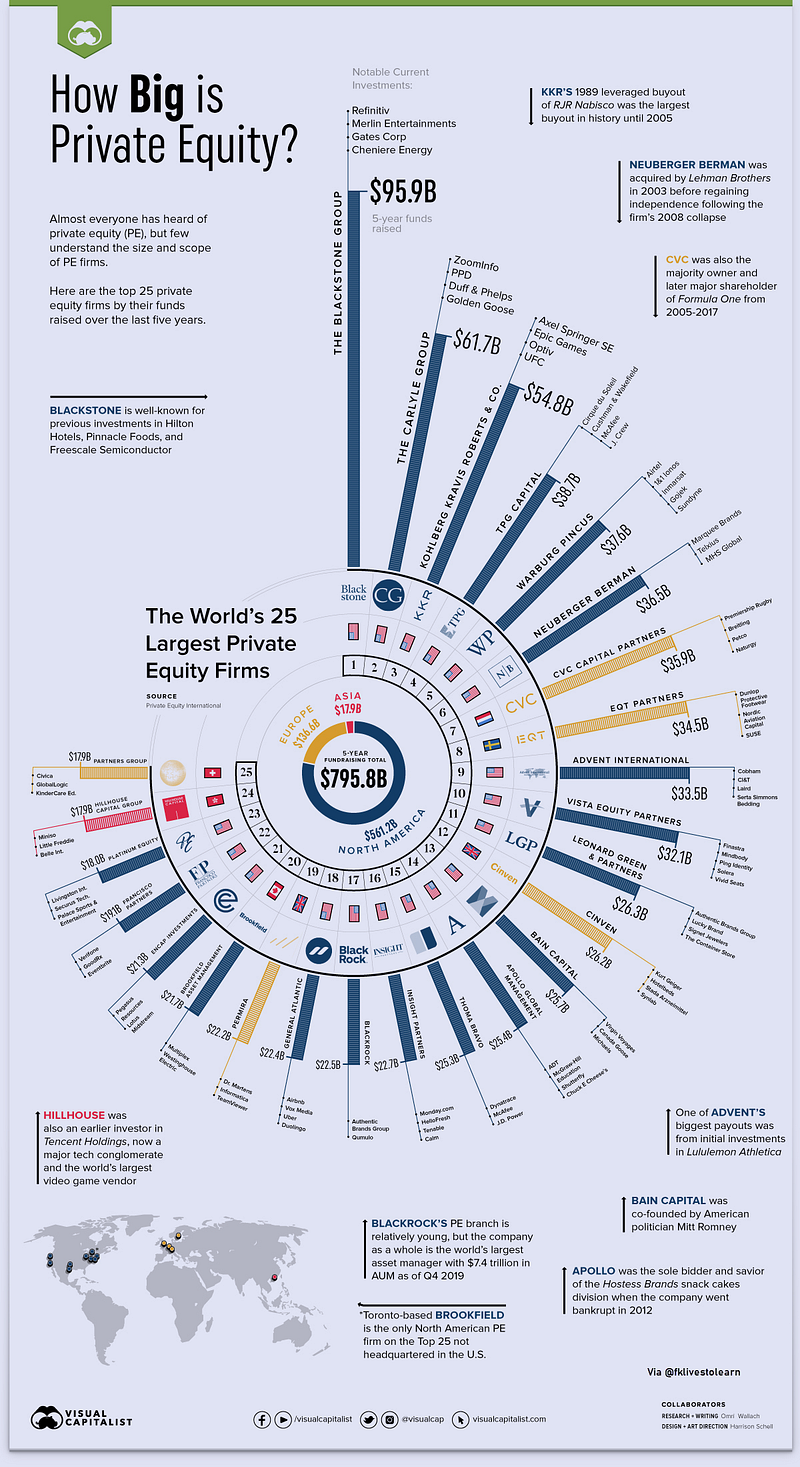

The 25 Largest Private Equity Firms

The following infographic provides the list of the 2 5largest private equity firms by their five-year PE fundraising total over the last five years. The data for the funds and investments from the listed firms was provided by Private Equity International. It includes the well-known private equity houses like The Blackstone Group and KKR (Kohlberg Kravis Roberts), as well as investment managers with private equity divisions like BlackRock.

Most of the world’s top PE firms, including TPG Capital (which invested in Ducati Motorcycles, J. Crew, and Del Monte Foods) and Advent International (an early investor in Lululemon Athletica) are headquartered in the U.S. In fact, of the largest 25 private equity firms in the last five years (Figure 5), just four are headquartered in Europe (CVC, EQT, Cinven, and Permira) and one in Asia (Hillhouse).

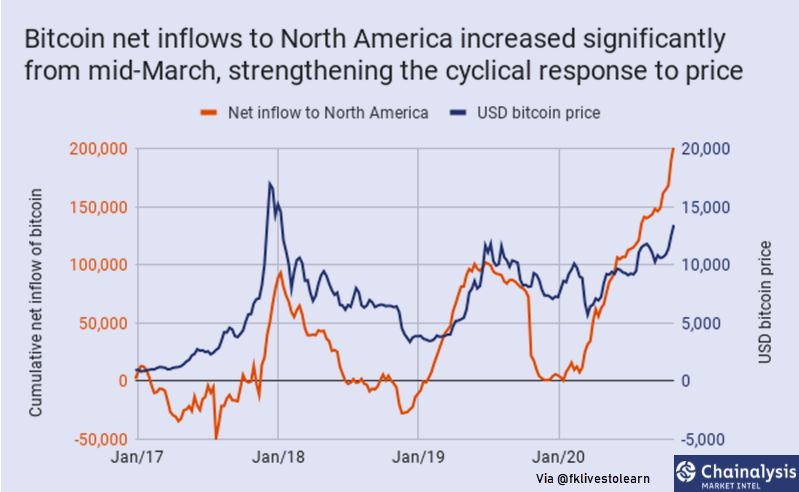

Bitcoin Net Inflows to North America jump higher

Bitcoin net inflows to North America have increased significantly from mid-March, with at least 200k bitcoin moving net from other regions to North America since then. This is shown in orange in the chart below (Figure 6), which presents the cumulative net inflow of bitcoin to North America relative to other regions since the start of 2017. Bitcoin tends to flow into North America as the price increases, then flows out when the price decreases.

Since mid-March, flows into North America have been high, and increasing faster than in past periods of price appreciation. This highlights the growing demand in North America in the current market than it has been in past markets. Western Europe saw a similar effect, although net inflows to Western Europe have tended to only increase since 2017, rather than fluctuating with the price.

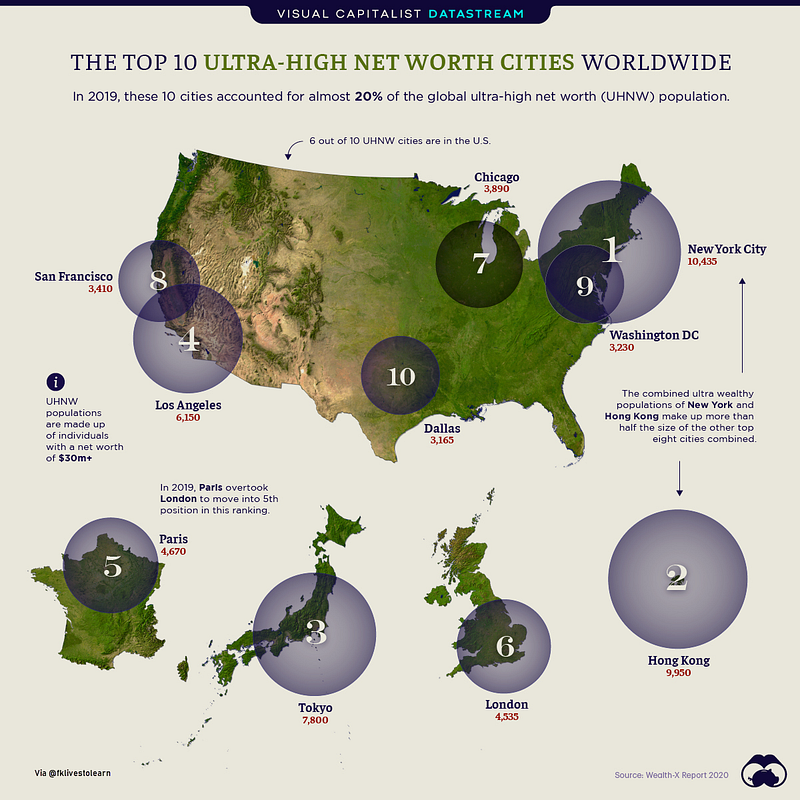

Top 10 Cities where the Ultra-Wealthy Live?

A very small group of ultra-wealthy individuals holds a significant portion of the world’s wealth is in their hands (or bank accounts). And just like their wealth, these UHNW people are concentrated in a small, select number of cities across the globe. But where, exactly, can you find these ultra-wealthy people? Using data from Wealth-X, here’s a look at the top 10 cities with the highest UHNW populations (Figure 7).

Market Humor — Market’s Choice

Previous Edition of GBW: