Data Science, Optimization, Programming

Genetic Algorithm for Trading Strategy Optimization in Python

How can GA help cut down problem space and converge towards a better solution?

If you have heard of systematic trading or algorithmic trading, then you must know that optimization of strategy is among one of the most important factors that dictate whether the strategy would even break even. And the worst part is: optimization is very computationally heavy. Imagine a simple MACD crossover strategy, there will be at least 3 parameters: fast, slow and signal moving average period, and hundreds of possible values for each, making it more than a million possible combinations.

Incomes genetic algorithm (GA): a probabilistic & heuristic searching algorithm inspired by Darwin’s theory on natural selection that the fittest survive through generations. In this blog, we are going to use GA as an optimization algorithm for identifying the best set of parameters. We will be illustrating it with a simple MACD crossover on Nvidia. Remember, this is only a demonstration of the application of GA for optimizing trading strategy and should not be copied nor followed blindly.

Note: We will be covering the code section by section. If you find it hard to follow or glue them together, no worries, the full script will be available at the end of the blog.

If you would like to learn more about how to avoid overfitting Genetic Algorithm, here is a sequel to this blog that focuses on some techniques to a more robust Genetic Algorithm:

What is a Genetic Algorithm?

Inspired by Darwin’s Theory of Evolution, the Genetic Algorithm is an iterative process for search the global optimal solution to a problem statement, from getting the best gene to survive in the harsh world to identify the best parameters to a trading strategy in this blog’s context. To better understand how a genetic algorithm works, here is a short crash course of the key concepts:

- Gene: This refers to a parameter/variable of the solution. It is quite usual for a gene to be represented as a bit (i.e. 0 or 1), but that can be changed based on the underlying problem statement.

- Individual / Chromosome: A string of genes that represents a solution.

- Population: One generation of individuals.

- Fitness Function: A function for calculating how successful (fitness score) an individual is. Depending on the underlying problem statement, we can search for individuals with the highest fitness score or the lowest. To embrace the concept of survival of the fittest, the better the fitness score, the higher the chance that an individual can survive and reproduce to form the next generation.

- Selection Strategy: This defines how we compare individuals against each other for selection the seeds for the next generation. Some common examples are tournaments (a random sample of individuals face each other 1 v 1, and the winner wins a place in the next generation), roulette (probability be chosen is proportional to the fitness score), or double tournaments for more complex scenarios

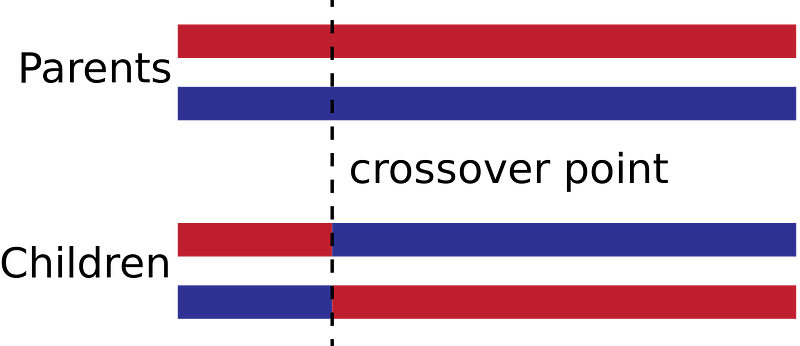

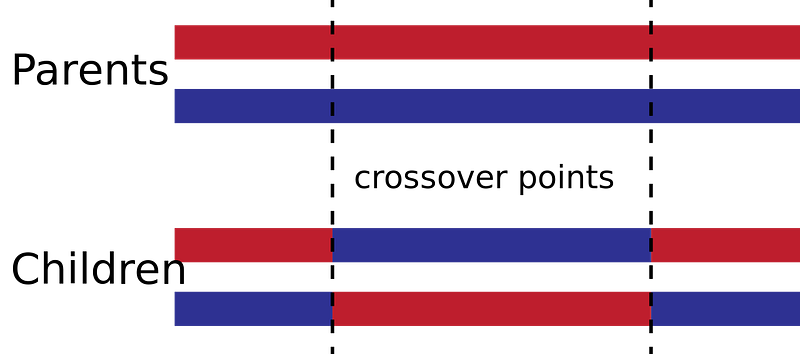

- Crossover Strategy: This is essentially how parent genes are passed to offspring when reproducing. Crossover is supposed to mimic sexual reproduction, where two parents are needed for reproducing. Genes of the parents will then be recombined to form offspring. Although different strategies are depending on scenario and data types, the most common two are k-point crossover and uniform crossover. In the k-point crossover, k crossover point(s) will be selected randomly, where the genes to the right of a point are swapped. Uniform crossover is relatively more straightforward: instead of having sections of genes swapped, every gene will have the same chance to be swapped.

- Mutation Strategy: As a way to maintain gene diversity and prevent premature convergence, genes of the children will have a random chance of mutating, meaning that the actual value will deviate from that of the parents. Mutation usually comes in the form of bit-flipping, index-shuffling, or bounded and unbounded statistical distributions.

These key concepts will then be combined to form an iterative algorithm:

- Parameterise the problem statement

- Define a fitness function

- Define a crossover, mutation, and a selection strategy

- Generate initial population

- Evaluate the fitness of the individuals of the population

- Select the individuals, crossover and mutate to form the next generation of population

- Repeat step 5, and 6 until convergence or until end conditions are met

Now that we have the crash course done, let’s see how this can be applied to trading strategy optimization.

Preparation

Before we start, let’s make sure that we have all our libraries installed and ready. Apart from the usual Pandas, Numpy, etc, we will also be using the following:

- Alpha Vantage: A Free-mium data provider. Rest-assured. A free license is good enough.

- Backtrader: An awesome open-source python framework that allows you to focus on writing reusable trading strategies, indicators, and analyzers instead of having to spend time building infrastructure. It supports backtesting for you to evaluate the strategy you come up with too!

- DEAP: Distributed Evolutionary Algorithms in Python, a novel evolutionary computation framework for rapid prototyping and testing of ideas.

To install them all, simply run the following line:

conda create -n myenvconda activate myenv && conda install -y python=3.8.5pip install alpha_vantage backtrader[plotting] deapNote: It is always a good idea to start a new project in an isolated environment, be it virtual environment, conda environment, or a docker container. It helps keep code and environment clean, reproducible, and portable.

Data Acquisition

With a key from Alpha Vantage, we can then use the snippet below for getting the historical stock price of Nvidia under the ticker ‘NVDA’. One thing to keep in mind when working with financial stock data is price adjustments. For example, Tesla went through a five-for-one split on 31st August. So one share before the split should be about five times that after the split. That’s why we will need to adjust prices according to splits and dividend events.

Fortunately, Alpha Vantage’s Daily Adjusted endpoint, we will have a close price adjusted according to the Center for Research in Security Prices’ formulae. We can then estimate the adjusted Open, High, and Low using the percentage change from unadjusted Open to unadjusted Close: if the percentage change in price for the day is +10%, then Close should be 110% that of Open, whether adjusted or not.

Once you have run through the script, read_alpha_vantage should return you a data frame with the first and last 5 rows similar to the followings depending on when you queried Alpha Vantage:

Backtrader Framework

In Backtrader, a strategy needs to follow the interface of backtrader.strategy. The most important components in the interface are:

params: parameters used by the strategy__init__: where we do data prep and define indicatorsnext(): which decides what should the strategy do in the next step

import backtrader as btclass CrossoverStrategy(bt.Strategy):

params = dict()

def __init__(self):

# initialise strategy

# do data prep

# define indicators

pass def next(self):

# trading logic

passA simple MACD crossover strategy consists of four lines:

- Fast (12-day) Exponential Moving Average of Close

- Slow (26-day) Exponential Moving Average of Close

- MACD line, the difference between the fast moving average and the slow-moving average

- Signal line, a 9-day moving average of the MACD line

We will also need to put in the trading logic under next(). To keep it simple, this strategy will be long-only:

- Long entry: When the MACD line crosses above the Signal line

- Long exit: When the MACD line crosses below the Signal line

The strategy would now need to be fed to the main engine of Backtrader — backtrader.cerebro, alongside our data, trackers (bt.observers) and analyzers (bt.analyzers) of the strategy, and other brokerage level settings like commissions and account balance.

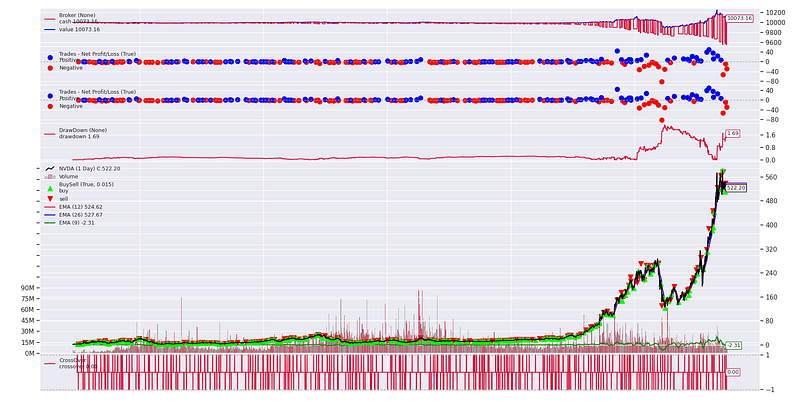

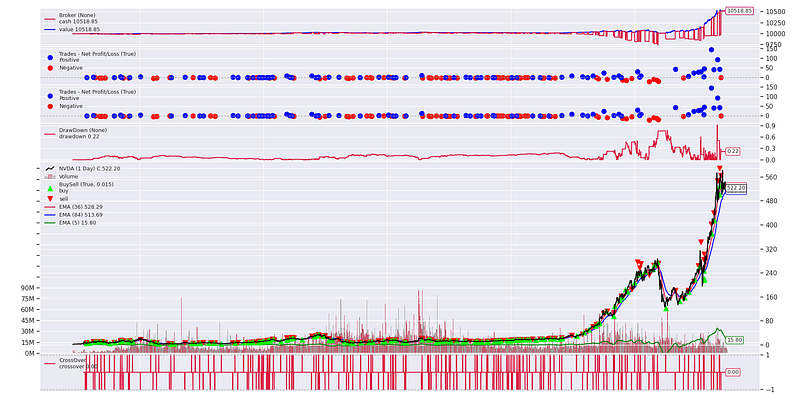

When you execute run_backtest(plot=True, **STRATEGY_PARAMS), you should get something like this:

Genetic Algorithm Parameter Optimisation

Making only 73.16 dollars out of the rocket of Nvidia with default parameters, that does not look promising at all. Let’s try to optimize the parameter to see if we can make it more viable.

Based on the crash course earlier, let’s define our algorithm as follows:

- Gene: This should be the

paramsfor our MACD strategy. Unfortunately, DEAP does not work well with keyword arguments as crossing over would require index slicing. Instead, we will be using alistfor storing the parameters. - Initial Population: Our initial population will have 100 individuals, each with random integers

fast_periodin the range of[1, 151),slow_periodin the range of[10, 251), andsignal_periodin the range of[1, 301). This means there are a total of 150 x 240 x 300 = 10.8 million possible combinations. - Fitness function: To balance rewards and risks, we will be using

Total Profit / Maximum Draw Downas the only objective of our fitness function. As DEAP is a generalized framework, it supports fitness functions with multiple objectives. As a result, the function needs to return a list of fitness score(s). - Selection Strategy: We will be using the classic tournament method where the winner of each round of the tournament will be selected as the seeds for the next generation.

- Crossover Strategy: We will be using uniform crossover with a 50% chance for each gene to crossover.

- Mutation Strategy: We will be using a uniform distribution of integers in the range of

[1, 101)with a mutation probability of 30% for each gene. - End Conditions: The algorithm will stop once it has finished 20 iterations.

The snippet below is the implementation of our genetic algorithm with the above settings. We have also added in a Hall of Fame which will keep track of the best individuals across the iterations of the algorithm.

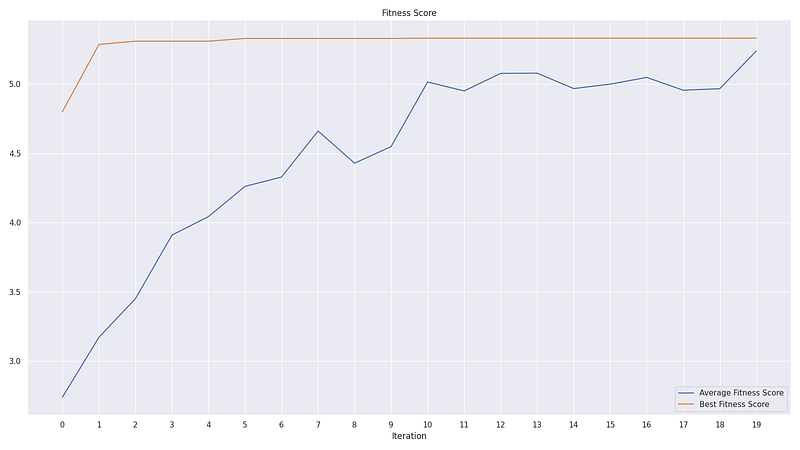

After running the snippet, we have the following results

HALL OF FAME:

0: [36, 84, 5], Fitness: 5.331913978803928

1: [36, 87, 5], Fitness: 5.329609884401389

2: [5, 143, 44], Fitness: 5.309777394151804

From the graph above, we can see how performance converges towards the solution very quickly in about 10 iterations. This means that instead of trying out the entirety of 10.8 million combinations, the algorithm has yielded us a candidate of the optimal solution with just a thousand of backtest runs, which is less than 0.1% of the problem space. And this is already a worst-case estimate for our case assuming that all the individuals are different in every generation of the population.

If we plug the optimal solution of dict(fast_period=5, slow_period=82, signal_period=38) back to the backtest function covered earlier with the following lines, we can see that the profit is now just over 7 times that of the default MACD crossover strategy:

OPTIMISED_STRATEGY_PARAMS = {

k: v for k, v in zip(PARAM_NAMES, hall_of_fame[0])}

run_backtest(**OPTIMISED_STRATEGY_PARAMS)

Conclusion

In this blog, we have covered the key concepts of genetic algorithms and demonstrated how we can use them to optimize a trading strategy.

Historically, parameter optimization is very demanding on computational power. In our example, the simple MACD crossover strategy with just three parameters was already generating millions of possible combinations. Even if each backtest can finish in 0.01 second, that would already be 30 hours of computational time in total. This will only get grow exponentially as the number of parameters increases.

With a genetic algorithm, we can converge to a candidate of global optima after about 10 iterations, which is less than 0.1% of the problem space. The optimized MACD strategy is also performing a lot better than that with default parameters, with over 7 times the original profit.

That being said, please remember that this blog is merely showcasing how we can leverage genetic algorithm as an optimization tool, and hence has been focusing on the underlying concepts and the simple code structure (available here) for us all to give it a try.

If you would like to learn about how to avoid overfitting genetic algorithms, here a sequel to this blog post focusing on how we can leverage random subset selection and Coefficient of Variation to train a more robust Genetic Algorithm.

This is about it for this blog. Hope you find the blog or the code useful! Feel free to reply or pm if I have missed anything, or if you have any questions. If you are interested in tricks to become a better Python programmer, I have put together a list of these short blogs for you:

- Python Tricks: Flattening Lists

- Python Tricks: How to Check Table Merging with Pandas

- Python Tricks: Simplifying If Statements & Boolean Evaluation

- Python Tricks: Check Multiple Variables against Single Value

If you want to read more about Python, Data Science, or Machine Learning, you may want to check out these posts:

- 7 Easy Ways for Improving Your Data Science Workflow

- Efficient Conditional Logic on Pandas DataFrames

- Memory Efficiency of Common Python Data Structures

- Parallelism with Python

- Essential Jupyter Extension for Data Science Set Up

- Efficient Root Searching Algorithms in Python

If you would like to read more about how to apply machine learning to trading & investing, here are some other posts that may be of interest:

- Genetic Algorithm for Trading Strategy Optimization in Python

- Genetic Algorithm — Stop Overfitting Trading Strategies

- ANN Recommendation System for Stock Selection

{kind=link}

#/media/File:TwoPointCrossover.svg){kind=link}