Fundrise Is Not Making Funds Rise

My hot take after three years

In the quest for financial prosperity, one often faces the conundrum of where to park their hard-earned money or funds, if you will.

Personally, I have spent decades reading about and researching personal finance mechanisms to increase my family’s wealth on my lone middle-class salary.

After reading about Fundrise by two of the personal finance bloggers whom I respect, I felt that it ticked several boxes for me so I dove in.

I always lacked the cajones to become a real landlord, so I figured this was a way to dip my little toe into the water of being one along with thousands of other investors on this platform.

I don’t want to beat it to death or do a long, painful analysis, but Fundrise has not performed up to my expectations.

Not even close!

It did when I started, and I suspect that it will once again, but their real estate investing model obviously hinges largely upon interest rate spreads, so as the interest rate has been raised over and over again over the past several years, the profit margin for the rentals that Fundrise has purchased versus the financing costs have been squeezed to razor-thin margins.

Before I share some of what those who run Fundrise write, I wish to share a comment that I frequently think of that my boss told me.

I am a long-time economic development professional, having served the same Chicago area city for the past eighteen years.

Thus, I have been through multiple boom-and-bust cycles including the boom times leading up to the Great Recession, the two very painful years of said Recession, the boom times following it, the massive crushing pandemic year of 2020, and now three more years following that.

In other words, multiple economic cycles including times when businesses were opening and expanding non-stop, years when everything seemingly went out of business and foreclosures were rampant, the massive run-up and opportunities of the longest bull market, which started in March 2009, near the end of the Great Recession, and roamed Wall Street for almost 11 years, and whatever the current cycle is whether you think it is teetering on the brink of Recession once again or the best economic time ever or somewhere in between.

What does this have to do with Fundrise?

Glad you asked.

When I had a great performance appraisal earlier this year based on the massive amount of economic development now occurring in our city and the numerous projects that are coming to fruition, I shrugged my shoulder and told my boss the truth — that I was working the same way, just as hard as I was when everything was closing and going under during the Recession.

“You got it all wrong,” he said.

“How so?”

“When things are going well like they are now, you should take full credit. But when they inevitably go to shit again, that’s when you blame the overall economy or Recession.”

Just like the guys at Fundrise.

When things are going up, they are effing genius investors, capitalizing on the fact that so many people young and old can no longer afford to purchase a home. Many do not even want to.

Pool together a few hundred million or billions from people like me and you and you have some major purchasing power. Institutional money.

So, after my first year with Fundrise, with my investment having increased by over ten percent, I felt pretty good about myself. Just like the Fundrise guys.

Now that things are down, is it their fault?

Truthfully it isn’t. But instead of admitting to overleveraging or not accounting for potential increases in the interest rate, they blame external factors:

When bad is good

On top of this inherent lag, interest rates have continued to defy earlier expectations, staying higher for longer than almost everyone predicted. And, of course, higher interest rates act as a headwind for real estate values.

While this is partially due to the fact that higher interest rates mean higher interest expenses which reduce a property’s cash flow, the bigger impact comes from the relative price at which someone is then willing to value the property.

In the simplest terms, while a 5% return on a real estate property might sound attractive when your savings account is generating 0%, in a world where your savings account is earning a 5% return, the return generated by the real estate property must inherently be much higher.

And, of course, the easiest way to improve a property’s return is simply to lower the purchase price you pay for it (i.e., its “value”). In other words, in a world where savings rates go from 0% to 5%, real estate prices must come down enough to generate a level of return sufficient to offset the implied higher risk of owning said real estate property vs. merely leaving that money in a savings account.

Of course while this means lower valuations for existing property owners, it also means that new investors (or even just new dollars) are getting in at a better price with the potential for higher future returns.

They are right that had I known about this, I would have simply held onto these funds and parked them in a high-yield savings account.

But as they say, hindsight is 20/20.

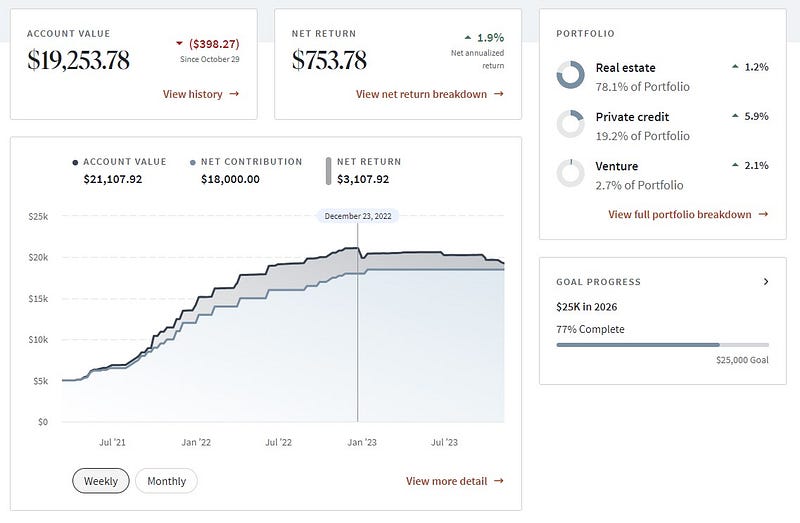

The team behind Fundrise may have expectations and I am quite certain that they follow the real estate market and overall market closer than I do. That’s why I entrusted them with around $20,000 of my hard-earned funds.

I will stick with it for a while, about six more years should I remain. Fundrise has some type of penalty if you cash out funds within five years and rather than deal with those intricacies, I shall simply wait. Those funds are earmarked in my mind as travel funds for 2026 through 2029. They will not cover all or even most expenses, but $5,000 to $6,000 per year to help cover travel would definitely help!

For now, I shall report my personal investment returns since I began investing in early 2021 as a meager 1.9 percent.

It’s better than zero.

But not by much.

One point nine percent to be exact, or more than three percentage points less than I currently collect on both a boring way to make money that is about to mature and a money market account.

I will stick with it for the time being, both hoping and kind of expecting the performance to improve in the coming years.

If it does, I will write another update around a year from now talking about what a great job the managers have done and how they are at least coming close to matching the return that anyone in the world could get by opening a simple savings account.

But it probably won’t.