A Boring Way to Make Money is Back

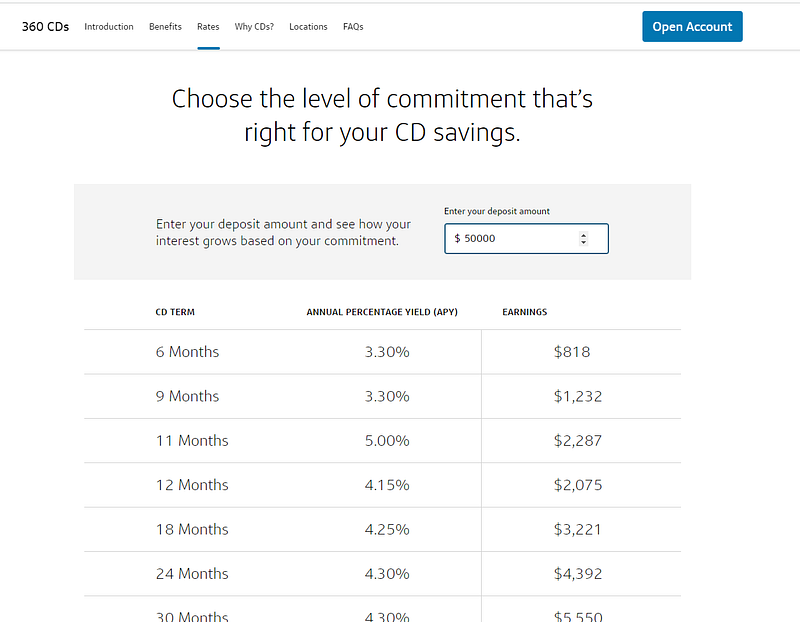

I’ll be collecting $2,287 from it

I’ve been investing for a while. As each year passes and more and more newbies enter the investing, or in the case of crypto, gambling world, it makes those of us who first parted with our hard-earned funds into something that we hoped would provide a return back in the day that much older and wiser.

I have stories galore when it comes to personal finance including raising my suburban middle-class family on my government worker-bee income alone while managing to save six figures for each of our children’s college accounts and then finally taking the advice to Pay Ourselves First to heart ❤️ and investing around $20,000 per year for each of the past seven or eight years.

I remain on track to semi-retire in my mid to late-fifties and tend to favor the Boglehead investing philosophy. I even bought a boring old savings bond last year.

All that is a preface to say that I am not really chasing some newly invented cryptocurrency or investing scheme that has the potential to make you rich quickly, but with even greater potential to lose it all. I’m a get-rich-slow kinda guy.

Part of our middle-classiness if you will is that my wife and I took our family to Walt Disney World six friggin’ times.

TBH, each of the times it lost its luster a little bit, but my wife loves the place so much that it became our go-to spot for spring break six out of eight years beginning in 2008. Incidentally, my wife and daughter are heading there together next month just for kicks and to get the hell out of Dodge.

Although I write that my wife and I took our family, in reality, she was the one who scoured the Internet for deals for weeks on end when it came to airfare and “special offers” from Disney and made all the dining and fast-pass arrangements.

I was the one who paid for it.

Any way you slice it, the trip always ran somewhere in the neighborhood of $5,000. These days, that does not even seem so high considering that we always lodged on Disney grounds at Port Orleans French Quarter and we always purchased five-day park hopper passes for the four of us. We always flew direct flights except for once, and we always dined at signature restaurants once or twice per trip and at mid-tier places the other times.

My wife’s and daughter’s trip next month is set to cost about the same for just the two of them, and they will be staying at Pop Century, a lower-cost “value” resort than where we used to lodge ($2,900 for six days, with five-day park passes not park-hopper).

I could go on, but suffice it to say that these were not cheap vacations. But most of it was paid for before we went, so I tried hard not to stress out about the cost while we were there. I would typically bring $800 to $1,000 in cash with me and would always give each kid $100 or more for spending money. They would also save up their allowances for the trip.

With my wife being a stay-at-home mom at the time, trying to pay ourselves first while I was also automatically investing $1,000 per month into our kids’ college accounts, and paying for all of their lessons (tennis, music, fencing, dancing, horse riding to name a few), we were right there on the brink of always spending more than what I brought in.

But I did not want to wind up an elderly guy sitting in a rocking chair by myself with millions in the bank while never taking our family on vacation.

So now I share the old-school way that I used to pay for about half the costs for those trips and what I just invested in today.

If you have been around for a while like I have, you may recall when you could buy a CD, not the kind that plays music, but the kind that is a certificate of deposit in a bank, that would pay out over five percent.

I cannot recall exactly because it was back around 2008 or 2009, but I once purchased a CD from a local bank that paid out around six percent.

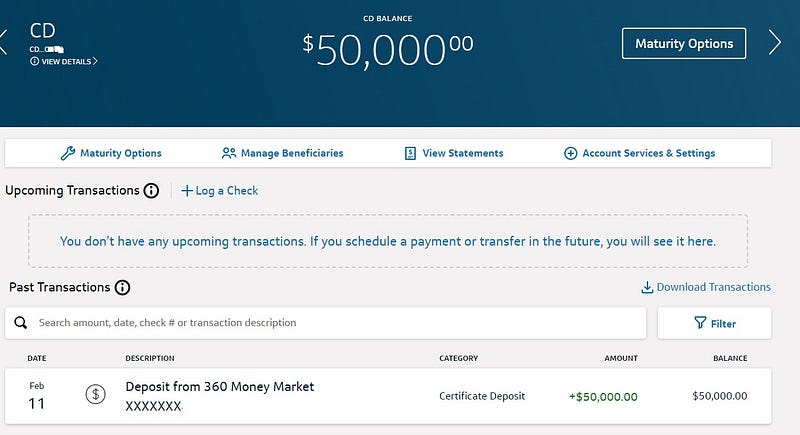

So the joke, if you will, is that you should start out with around $50,000.

I do not mean that to be snarky either. I fully realize that we all have our various shades of green and that many people can never come within miles of saving up that kind of dough.

But there are also millionaires in the making reading this, many of whom have far more than that at their disposal. You can obtain the same rate of return for investing whatever the minimum deposit is, but it helps if you can invest around $10,000 or more to open one.

While doing all of the financial stuff referenced above such as paying our mortgage, car payments, utilities, school items, super high property taxes, lots of food, saving for college, and beginning to pay ourselves first, I also scrimped and saved during those years to the point where I amassed a rainy day fund in the $60,000 range.

Again, this is not a sexy story. I saved it through sheer determination while my wife clipped coupons, we watched our old tube TVs, bought everyone’s clothes with thirty percent off coupons from Kohl’s, and used the same pay-as-you-go phones that we use today. I even drive the same car now that I was paying for back then.

Although I acted nonchalant as I purchased CDs in amounts between $50,000 and $60,000 for about four years, as if it was a mere pittance within a vast fortune, what it was, in reality, was over ninety percent of our liquid funds. I figured that in case of a major emergency, I would cash it out, suffering the consequences in terms of fees and whatnot.

One time, I drove out to a small, privately-held bank — St. Charles Bank and Trust — because it was the one with a one-year CD in the six percent range. After receiving my wife’s credit card bill with the $2,700 or so charges from Disney that spring, boy was I glad to collect roughly the same amount from the CD!

If there was any downside to the 128-month period of massive economic expansion from June 2009 to February 2020, it was that the ultra-low interest rates applied not only to borrowers but to fixed-income investors as well. Certificates of deposits were such jokes that most savvy investors would not even consider them.

Along with the massive inflation that we are all living through and the Fed raising interest rates eight times since early last year, someone who keeps their eyes and ears open for investment opportunities cannot help but notice that the banks are finally offering better rates to investors.

For quite a while, it seemed as if all banks were enjoying collecting more interest from borrowers, while the rates that they offered in fixed-income opportunities lagged behind.

What would you expect? Their entire profit margin is based upon the interest rate spread between funds loaned out and that they pay.

So as the interest rates have been rising over the past year, so have the myriad ads appearing before me and being mailed to my home by the banks that I have relationships with.

Most likely because I searched out high-interest CDs a few times, ads for them began to appear all over my various feeds.

The topic for another story, I now have something along the line of seven or eight banking relationships. I am not claiming to be wealthy, mind you, I am simply sharing that through a number of things that have transpired over the years, I might be what one would consider “overbanked.”

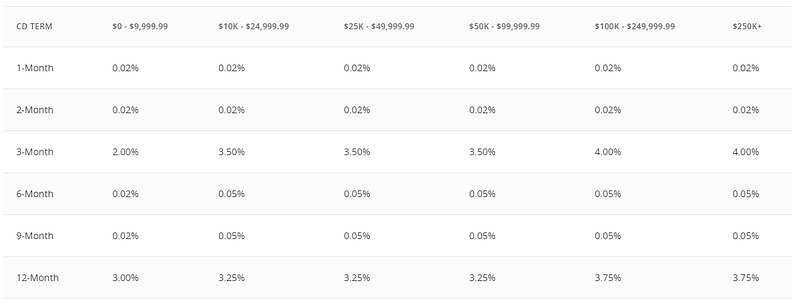

One of my banks is Capital One, where I have held an online savings account for quite some time. TBH again, Capital One acquired a bank that I once had both CDs and our mortgage with called ING Direct in 2012 and I just never closed it.

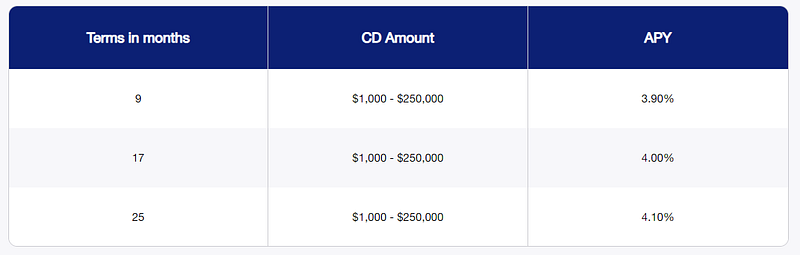

I do not particularly favor Capital One, but seeing that you could get a higher rate from an eleven-month CD than a one-year or even a 30-month definitely piqued my interest.

Waiting only an extra two months, eleven instead of nine, could get you a cool grand (plus $55) if you are willing to park $50k until early next year.

I fully realize that it is neither an exciting investment opportunity nor a way to make the big bucks. Even with a guaranteed five percent return, this is decidedly not a way to save your way toward massive wealth.

What it is is a pretty decent return on your family’s emergency fund if you have one. You know, those funds that you have or will save up for those inevitable hard times that hit when you least expect it.

You don’t want to spend those funds, but you would sleep better knowing they are there.

Yet another story for another day is how much of a cushion you should have. While I do not always agree with one of the gurus, Suze Orman, I do tend to agree with her advice on how much you need in an emergency fund to cover between 8 and 12 months, to 12 months worth of expenses.

She recently reminded us once again that there’s a potential recession looming on the horizon and said “You know that my hope is that you work your way toward having enough set aside to cover 12 months of essential living costs. And you also know that I realize that can take time. Every month you move closer to your (new) goal is a month to celebrate your progress.”

In my own family’s case, that means having give-or-take around six figures liquid, which is something that I do currently have but, once again, do not assume that it came easily. I am a true grinder and have worked like a good worker bee for going on thirty years now.

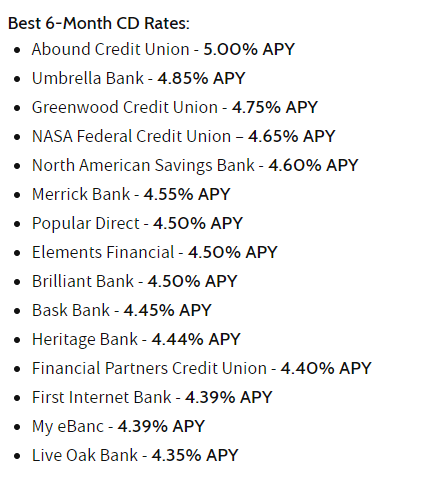

The moral of this story is that there is, once again, an investment option in terms of a decent, if not impressive, return on deposits if you are willing to park some funds for at least six months.

The six-month CDs in my area are in the four percent range, although I have found higher ones online if you are willing to share every bit of information about yourself with some random bank that you’ve never heard of.

I chose the highest rate under one year that I could locate with one of the banks that I already have an account with.

You may not have too many banks as I do, but if you have a few bucks set aside for that inevitable rainy day and can hopefully get by the next six months without needing them, why not look around like I did and let those dollars grow by four or five percent?

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.