Five Steps to Become a Millionaire

Follow These Steps and Make Your Dreams Become a Reality

S o you want to be a millionaire. That’s a goal many want to achieve but few get there.

It is hard to reach this goal but with the right planning and following these steps, you can get there too.

On Dave Ramsey’s blog, he wrote there were 11 million people who were millionaires as of 2017. This is equivalent to 3% of the population. It was also estimated the number of millionaires continues to grow. This information is gathered from data before the corona virus of 2020 so the numbers could be different as of this article.

The NY Post stated 250,000 people became millionaires in 2018.

For the past 10 years, the number of millionaires continues to grow.

The number of millionaires in the high net worth category was 1.3 million people and they had assets between $5 million and $25 million not including their primary residence.

Over 173,000 people had a net worth over $25 million dollars.

To avoid any confusion and make sure we are on the same sheet of music, let’s define how to consider someone a millionaire.

A millionaire is someone who has a net worth of 1 million dollars. Net worth is your assets minus your expenses.

Assets can be your investments, savings, jewelry, and rental properties. Then you subtract any expenses such as mortgage debt, loans, and any bills. Once you subtract the assets from expenses, you have your net worth.

Investments — Expenses = Networth

If you want to be a millionaire, you need to do a few things to get there. I’ll lay out five basic guidelines but it’s really up to you to figure out how you’ll reach a million dollars. You’ll have to do the hard work to get there.

I’m going to assume you work at a job and you will archive a million dollars by investing. So winning the lottery or receiving a big million dollar contract are not included. You can achieve millionaire status that way but I will not focus on those paths.

Step One — Figure out how you plan to get there

Most likely you have finished school, high school, college, or have a GED.

If you don’t have a diploma or degree, it doesn’t matter. Anyone can follow this plan to achieve a million dollars.

It’s not that hard and having a high school diploma or a doctoral degree isn’t required.

The real education is your financial education and not your book smarts. These two educations are very different.

Some obvious answers to achieve a million dollars are investing in the stock market, real estate, selling a product or products, or creating a business. There are other ways but these are the easiest ways to build your wealth.

Step Two — Stick to your plan

Once you have figured out your path to achieve a million. The key is to stick to your plan.

It is too easy to lose focus or get distracted.

These days distractions are your worst enemy.

There are too many bright ideas that can cause you to lose focus and delay your path to seven figures.

For instance, advertisements about making money are out there.

Many internet ads will mention how to flip homes to make millions.

Another ad can mention buying a course to succeed in Amazon FBA, Fulfillment By Amazon, selling on Shopify or Etsy, or many others. There are too many to name.

I am not saying you can’t earn millions through one of these courses but the chances of success are much harder than taking the slower path to millions.

An easy way is to write down your goal and look at your goal daily.

Also, you could write down your goal once in the morning and again in the evening before you go to sleep.

The process of repetition and seeing your goal has a powerful effect.

Continue this process until you have achieved your goal.

You need to stay focused and believe that you can achieve your goal.

Step Three — Avoid bad debt like the plague

Debt is possibly the biggest way to prevent someone from having a seven-figure account.

Money you could use for investing won’t be available since debt will keep you from increasing your net worth.

Let me go a step further since not all debt is bad.

Yes, if you love Dave Ramsey, you won’t like what I’ll say.

It is true debt isn’t good for anyone. There is good debt as well as bad debt. If you didn’t know, there is a difference between the two debts.

I’ll start with bad debt which is what we all know and don’t like.

Bad debt is owing money to a credit card company, bills you have to pay, literally any debt that doesn’t show you a return on your money.

Robert Kiyosaki, the author or Rich Dad Poor Dad, made the term good debt very popular for many to understand this basic concept.

Good debt is debt that has a return on your investment. I bet you didn’t think about this but good debt can work in your favor.

For instance, if you have debt for a rental property and your tenant pays the mortgage, insurance, and property taxes. Then this is good debt.

This is not hard for people to do yet they are scared by horror stories they hear about tenants trashing rentals which does happen. I won’t lie. But this does not happen for every single investment rental.

I have invested in real estate since 2004.

Yes, I have had some dead beat tenants who like to lie and get out of paying their rent for a month or two.

Then there was the one tenant who was taken to court and lied about her dog since the lease said no dogs allowed without prior approval.

The number of times incidents like this happens versus the tenants who have paid on time are very small in comparison.

So you will have some bad apples every once in a while. But for the most part, people pay their rent and do the best to keep your rental clean so they can get their full deposit back.

So having real estate that you rent out is good debt since the tenant is paying your mortgage, and increasing your network on your way to a million dollars.

Good debt has a return on your investment where bad debt doesn’t and only helps to fatten someone else’s’ bank account.

Step Four — Pay yourself first

You probably get a paycheck or two every month from your job.

What do you do with your money?

Most likely you pay your bills such as your rent/mortgage, basic utilities, cell phone bill, put money aside for food, and so on.

One idea you should do is pay yourself first.

By this I mean take a portion of your pay and invest in yourself.

Yes, we all have bills and owe someone for this bad debt. But you should allocate part of your money on you.

You will need this money in a few months or years later so you need to retrain your mind to invest in you.

This money can be used to invest in your retirement account, your investments or money for your business.

Setting up this plan will help you get to your million dollar goal a lot faster if you don’t already have this money in your monthly routine.

For investments, a lot of companies and tools allow you to set up the automatic investment plan which only takes a few minutes to set up.

Once you set this up, you never have to worry about it.

Your money is making you money.

Plus with many investments, this money will grow at a higher rate of return than money sitting in your bank account which earns less than 1%.

Most investments will also earn more than the high yield savings accounts but even these are not as paying as much as they were earlier in the year before the coronavirus.

So if you haven’t already, set up your automatic investment plan and make this a normal part of your monthly budget.

Step Five — Invest early and often

This last step relates very closely to the previous step to invest in yourself.

In this step, you need to invest early and often.

For this step, it applies primarily to someone who wants to invest.

When you invest, the money invested compounds over time.

So the earlier you invest in life, the more money you’ll have invested that grows and compounds.

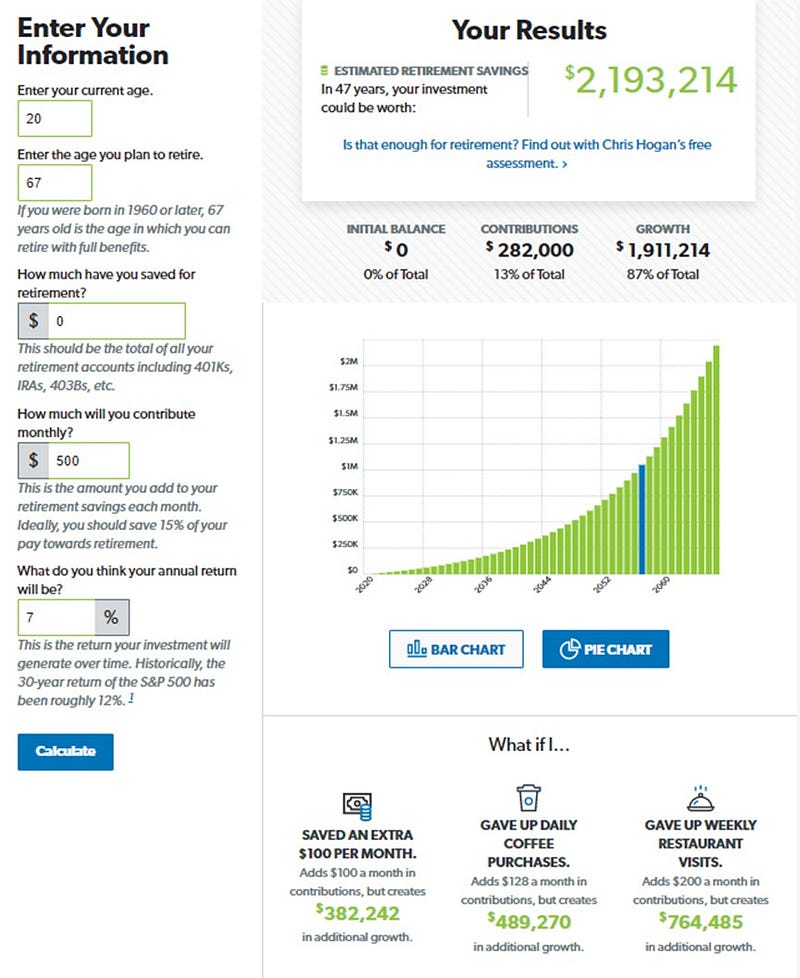

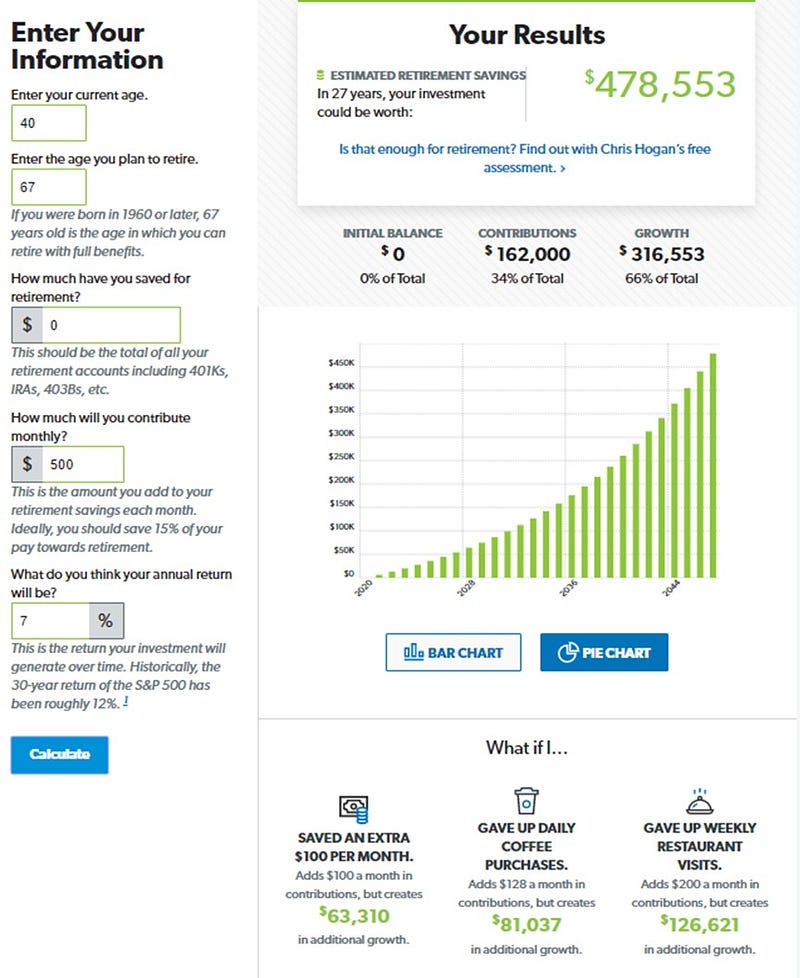

I ran some examples on Dave Ramsey’s website on the retirement calculator. Using two examples for a 20 and 40-year old, I used $500 a month which is the maximum someone could invest in their IRA, Individual Retirement Account. This doesn’t include the catch-up addition for people who are 50 years and older who can invest an additional $1000 a year for a total of $7000 a year.

The results for both by the age of 67 is very shocking and will open your eyes.

This is the example for a 20-year-old who starts to invest $500 a month in their IRA.

This is the example for a 40-year-old who begins their IRA contributions using the same amount invested as the 20-year-old.

Notice both individuals invest the same amount of money each month but one has more money at the age of 67.

Between the two, a little over a $2 million dollar investment compared to $470,000 is a big difference in how much these individuals have by 67 years old.

The earlier someone invests, the more they will have from the money invested and compounded over the years.

Some years the investment return will fluctuate but I used a conservative 7% return for the investment.

Investing early and often pays off in the long run.

The sooner you start, the more money you’ll have later on.

I recommend that you should read this article I wrote on how to invest with the Webull app if you want to get started with your IRA. You can read the article here.

Tom Handy is a top investment writer on Medium, and father of two kids. He retired from the Army and sits on several non-profit boards. Tom is the top Yelper in his community and a top Google Guide. He’s on several social media channels and you can find him on Twitter @tomhandy1 and Instagram @tomhandy1.