Do Randomly Picked Portfolios Consistently Outperform the Market?

Understanding Why Randomly Generated Stock Portfolios Often Perform Well

In this article, I will cover the effects of variability and randomness on your investments and how you can benefit from them.

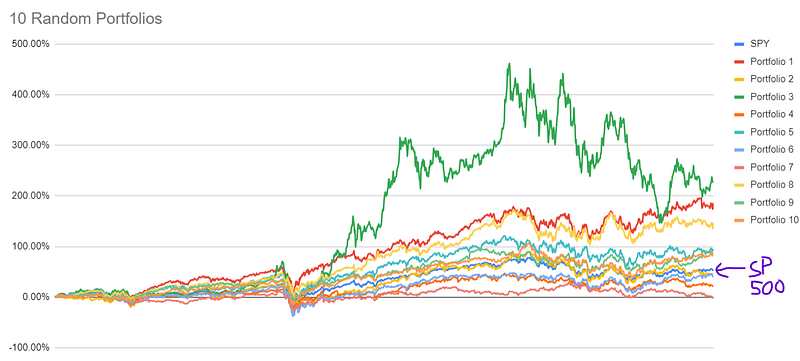

In my previous experiments, I’ve shown that my cat Bunbun created 10 random portfolios — 6 performed better than the index, and the top random portfolios returned 229%, 187%, and 147% in a 5-year period tested.

But that’s odd, isn’t it?

Why do random stock portfolios often outperform both Wall Street fund managers and the S&P 500 index?

How can random portfolios generate such impressive profits? Should we all start making random investments?

And is the popular quote from Burton Malkiel true?

“A blindfolded monkey throwing darts at a newspaper’s financial pages could select a portfolio that would do just as well as one carefully selected by experts.”

— Burton Malkiel in the book A Random Walk Down Wall Street

I wanted to test that, but instead of using blindfolded monkeys, I have used my cat.

I've created a spreadsheet for you to use if you want to test the random stock portfolios yourself.

But how is it possible that random portfolios often perform so well? Should we all add randomness to our investments?

Why Did Our Random Portfolios Perform So Well?

There are 2 reasons why our randomly picked portfolio performed well:

- Randomness doesn’t care about mental biases. I covered these biases in the previous article.

- The second reason is mathematics, which I will cover in this article.

The Mathematics of Exponential Returns Versus Linear Risk

The more random something is, the more it divorces from the average. In this case, randomness in stock picking drives us away from the average returns of the stock market.

Nassim Taleb extensively explored this idea in his book Antifragile—Things that Gain from Disorder. You can also check his article Understanding is a Poor Substitute for Convexity.

Someone with a random convex payoff doesn’t need to be right the majority of the time, as the payoffs are convex, and the upside is higher than the average.

What do I mean by payoffs/returns being convex?

Let me explain with charts.

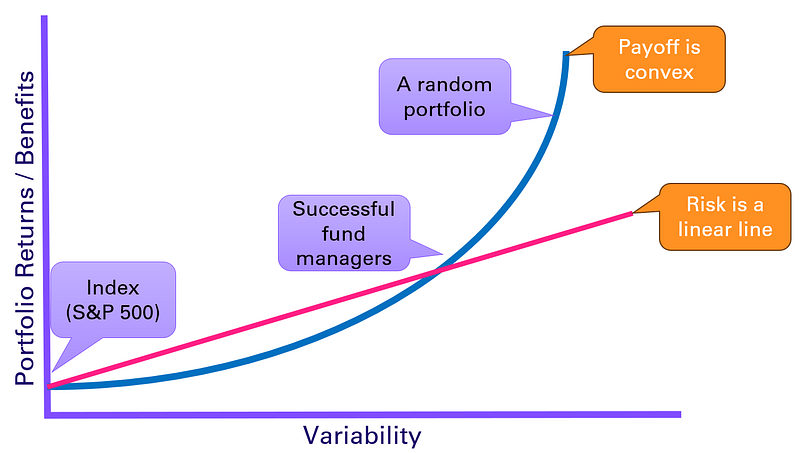

The chart above illustrates that portfolio returns will increase with variability—by adding randomness, such as picking random stocks.

Risk increases linearly as a function of variability; that is, greater variability corresponds to higher risk.

R = aV + b

Where:

R: risk

V: variability

a: slope of the linear function

b: y-intercept of the linear functionHowever, the payoff follows a convex function of variability, meaning that as variability increases, the payoff accelerates at a higher rate.

P = x^(yV)

Where:

P: payoff

V: variability

x: base value

y: exponentIn other words, as variability grows, the payoff grows faster than the risk, leading to potentially higher returns for the same level of increased risk.

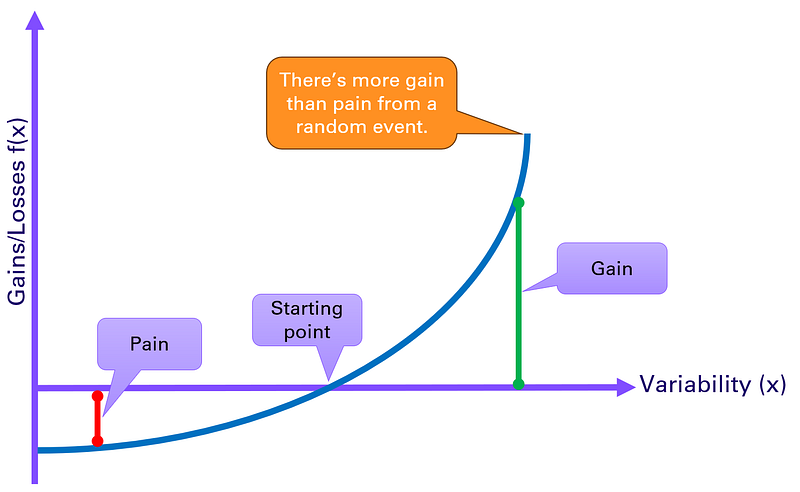

For each new unit of risk added to the portfolio, the payoff can increase in a more exponential manner. This is because of the way convex functions work. For each unit of risk, the payout increases by x^yV.

Uncertainty increases the upside more than it increases the downside.

As you can see in the chart above, the least uncertain portfolio would be investing in the S&P 500. Successful fund managers who outperform the index add more upside than risk. However, a random portfolio can often have asymmetric payoffs.

This is what I mean by “The more random something is, the more it divorces from the average.”

Embracing Variability: The Mathematical Advantage of Random Portfolios

If you add some randomness to a portfolio, you might have a higher upside, as this variability gets you away from the average — in this case, the S&P 500.

Convex Payoffs Benefit from Uncertainty and Disorder

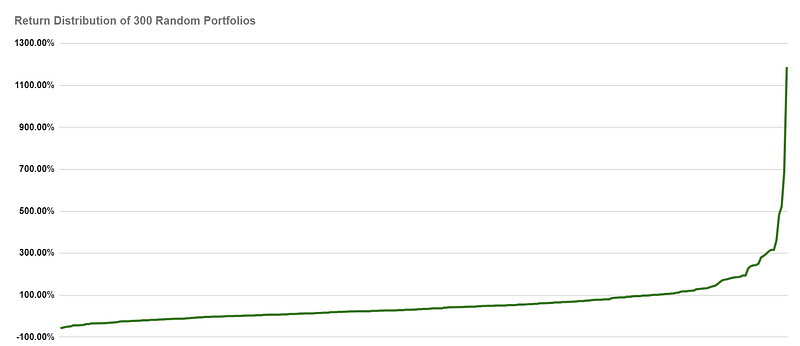

As we saw above, payoffs can accelerate with variability. I’ve simulated 300 random portfolios to show that these asymmetric gains can be very high while the “pain” is always limited.

In my simulations, the worst portfolio returned was -67%, but the best portfolio returned 1,188%. This is what I mean by “pain is limited” while the gains can eventually be high.

This further proves that “the more random something is, the more it divorces from the average,” as a 1,188% return is far from the S&P 500 average.

The convex payoffs also prove that the downside brought by variability is limited while the upside is uncapped.

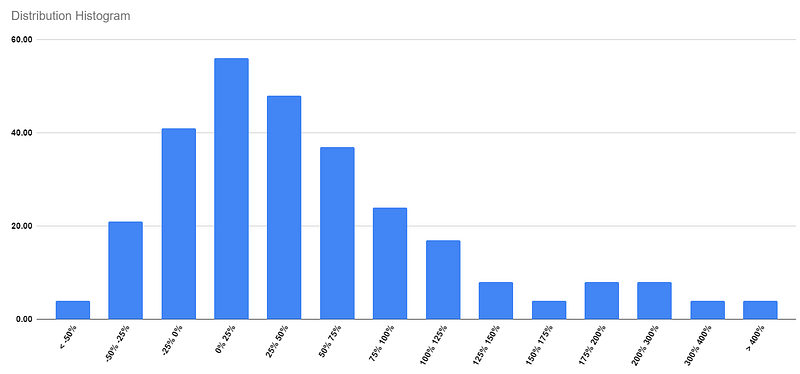

We can also look at the distribution histogram below to see how the convex distribution plays. While it seems that there’s a large concentration of random portfolios in the 0% to 25% range and the 25% to 50% range, the reality is that the long distribution across all the other ranges show that 60% of all the 300 portfolios outperformed the S&P 500 index.

This convex upside can also be explained by Jensen’s Inequality, which suggests that if the portfolio return is a convex function of the individual asset returns, the expected return of the portfolio will be greater than or equal to the weighted average of the expected returns of the individual assets.

Note that I’m not saying that a random portfolio will always outperform the index. Please don’t go all in investing in random portfolios. What I’m saying is that adding variability to a portfolio has certain mathematical advantages.

Can the Law of Large Numbers Counteract Convex Payoffs?

Individual random portfolios can outperform, but… there’s a but.

As we increase the number of random portfolios, their average return will converge towards the index's return.

For example, if we generate 200 random portfolios, their average return would be closer to the index’s return of 50%. If we further increase the number to 400 random portfolios, the average return would be even closer to the index.

This phenomenon can be explained by the Law of Large Numbers, which states that as the number of observations increases, the average of the results will converge towards the true average. In the context of investing, too many stocks will “kill randomness” by being too diversified, causing the average return to converge to the market average.

The key takeaway is that introducing randomness in stock selection can mitigate the biases often present in traditional stock-picking methods. It is possible to outperform the index by doing so, but the Law of Large Numbers limits this.

In this case, chance stops being chance when you try it hundreds of times.

Conclusion

The analysis of randomly picked portfolios reveals interesting data regarding the role of variability and randomness in investing. Individual random portfolios can outperform the market index, but we need to understand the mathematical principles behind them.

The convex payoff structure of random portfolios allows for potentially higher returns compared to the linear risk increase. This means that as variability grows, the payoff can grow faster than the risk, leading to asymmetric gains.

If you want to play around with random stock portfolio generation, use my Random Stock Portfolio Simulator Google spreadsheet. You might need to request permission, but I will approve it ASAP.

— Henrique Centieiro 🕺🏻

If you found any value in this article, throw me some love!

🥰 What you can do to support my work: Clap up to 50, leave a message to share your thoughts & be sure to follow. 💌

🚀 Follow my Limitless Investor publication for more valuable content in the future:

🌞 Stay in touch: