My Cat’s Randomly Picked Stocks Outshine Wall Street with a 226% Return

How Can Randomly Generated Portfolios Outperform Wall Street?

After working in finance for the last 18 years, I finally realized that putting my hard-earned money into actively managed funds isn’t worth it.

I’ve switched from actively managed funds to index ETFs. These are completely passively managed but still outperform most professional funds.

Staggeringly, 88% of professional fund managers in the US underperform the S&P 500, while 92% of European funds underperform the S&P 350 Europe.

I don’t understand how big fund managers justify their fees. It’s baffling why people continue to invest in actively managed funds instead of choosing index ETFs or even randomly picking stocks!

Look, you can hire my cat, Bunbun, to pick your stocks, and she is more likely to perform better than those professional fund managers — even though she doesn’t even have an MBA.

Bunbun is a 2-year-old cat with an extraordinary origin story. We discovered her as a kitten, just a few weeks old, abandoned and dodging cars on one of the busiest streets in Hong Kong, while we were passing by in a taxi.

Now, prepare to be amazed as you see how she has evolved from a vulnerable kitten into a remarkable stock investor — her investing skills will blow your mind.

Here’s How We Pick Random Stocks

To assist my cat Bunbun in picking stocks, I created a spreadsheet simulator that randomly selects 5 out of 3,524 stocks from the New York Stock Exchange.

The simulator then generates a chart showing each stock’s performance and another chart comparing the random portfolio to the S&P 500 over a five-year period.

Later, I will show you how to try it yourself, but first, look at these amazing results. I will also explain the mental biases and the mathematics justifying how totally random portfolios can significantly outperform the benchmark.

Bunbun, press the button!

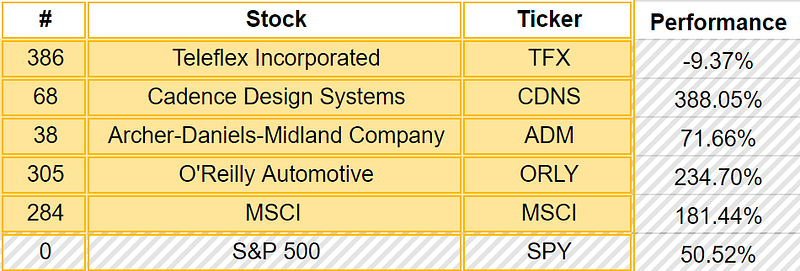

Random Portfolio 1: 173% Return

Incredibly, the first random portfolio generated by Bunbun yielded a 173% return over the tested five-year period, more than tripling our benchmark — the S&P 500, which only returned 50%.

Here are the 5 randomly picked stocks. As you can see, these stocks are not the most popular:

The 5-year portfolio performance of this first simulation is also very impressive. The chart on the left shows the 5 random companies and the S&P 500 (SPY) in navy blue. The chart on the right shows the portfolio performance:

Pretty impressive, huh? Is this just luck? Or can we replicate it?

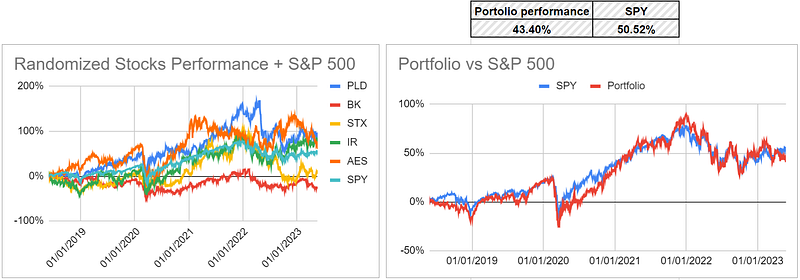

Random Portfolio 2: 43% Return

The second random portfolio generated by the random tool that BunBun used is a bit lower than the first, returning “only” 43% and underperforming the index.

I guess the Bank of New York Mellon screws the returns of the portfolio.

The stocks picked can perform extremely well, around the average, or very poorly. Consequently, the return distribution of our random portfolios is a convex curve.

In this case, as the chart below shows, the portfolio's performance was quite close to the SPY average:

My dear kitten, can you do better picking the next stocks?

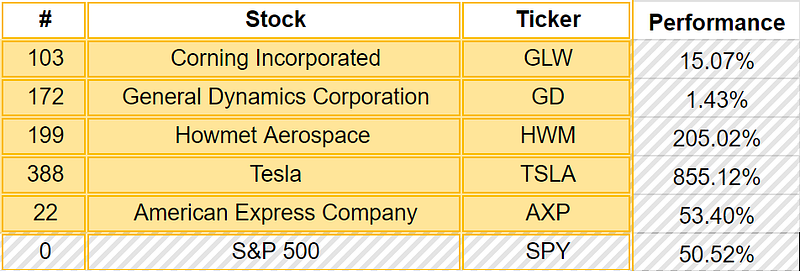

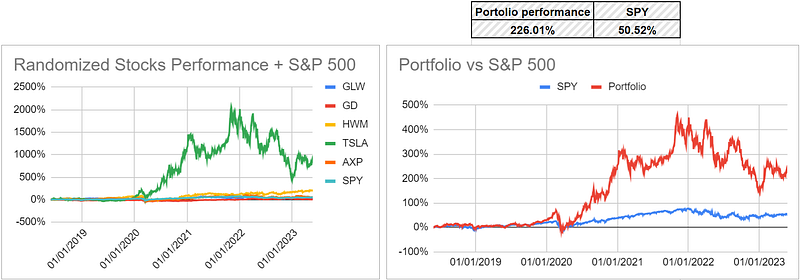

Random Portfolio 3: 226% Return 🤑

Well done, little kitten! 226% return versus 50% on the S&P 500 is a remarkable result.

If my cat were a Wall Street fund manager, she would have a very nice end-of-year compensation, perhaps something close to $1 million. However, because our stock picker is a cat, and the stocks were picked randomly, she will only get a small dried fish snack. 😿

Two of the five randomly picked stocks performed extremely well. Howmet Aerospace increased by 205%, and Tesla increased by 855% during the 5-year period.

This, of course, reflects on the total portfolio return:

I have to promote this kitten to Senior Portfolio Manager of the fund!

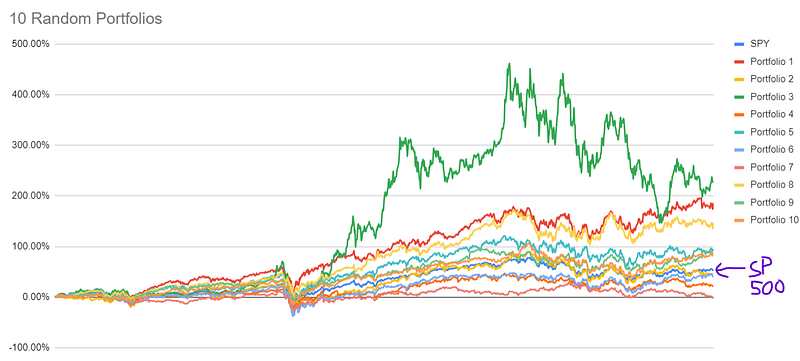

Now, let’s take the random stock simulations a bit further and analyze 10 random portfolios. Let’s see how they perform.

Simulating 10 Randomly Generated Portfolios

We conducted a simulation to generate 10 random portfolios, comparing their returns to the S&P 500 index. Surprisingly, 6 out of the 10 portfolios outperformed the index, with the 10 portfolios giving us an average return of 92%.

Recall that only 20% of professional fund managers outperform the S&P index. However, 60% of our totally random portfolios have outperformed the index:

This raises the question:

Can randomly selected portfolios consistently outperform the market index and Wall Street funds?

How can random portfolios perform so well?

There are 2 main reasons:

- Randomness doesn’t care about mental biases.

- It’s mathematical — the more random something is, the more it divorces from the average.

Someone with a random convex payoff doesn’t need to be right the majority of the time, as the payoffs are convex, and the upside is higher than the average.

I will write another article detailing the mathematical reasons why a random portfolio outperforms the average. It will include interesting concepts like the law of large numbers, convex functions, and Jensen’s Inequality.

For now, let’s look at the psychological aspect of it.

Why Does My Cat’s Random Portfolio Perform Better than Wall Street Funds?

Behavioral biases explain well why a randomly picked stock portfolio selected by my cat performs better. A random portfolio is the least biased portfolio anyone can achieve.

Awareness of these 5 biases can make you a better investor:

1. Herd Mentality

- Fund managers are pressured to invest in popular stocks with lower growth potential. “Nobody Gets Fired For Buying IBM” is a Wall Street phrase that illustrates this. They should rephrase it to “Nobody Gets Fired For Buying IBM, but they should.”

- Conversely, lesser-known stocks can perform better as they are overlooked by stock analysts. This is called the Neglected Firm Effect. Our randomly selected portfolio includes lesser-known stocks that have performed exceptionally well.

2. Loss Aversion

- Loss aversion can hurt because investors miss out on potential opportunities by being too risk-averse. As Omar Aguilar, CEO of Charles Schwab Asset Management, mentioned, Investors end up prioritizing losses over earning gains.

- A randomly picked portfolio is not subject to this bias, as it does not involve active decision-making.

3. Anchoring

- Professional fund managers tend to “anchor” to certain information or a sector or stock analysis. This is what Charlie Munger called the liking/loving tendency: people are likely to invest in companies or industries that they personally like.

- The solution to this bias is to be aware that anchoring to certain information or liking something or someone might distort your logic.

4. Doubt-Avoidance Tendency

- Fund managers will stick with conventional wisdom and consensus opinions — for example, Modern Portfolio Theory and the 60/40 portfolio — which leads to a lack of contrarian thinking and failure to identify opportunities that a random portfolio might capture.

- Often, to be at the top, you need to be a contrarian.

5. Overconfidence Tendency

- Overconfidence is a cognitive bias that can lead fund managers to excessive trading or buying/selling stocks too often. This leads to investors' illusion of control and sub-optimal decision-making.

- On the other hand, our randomly chosen portfolio was simply held for 5 years, just like Sleeping Beauty would do.

In simple terms, by removing human emotions from the equation and increasing randomness, we increased the profitability of our investments and the upside of the portfolio.

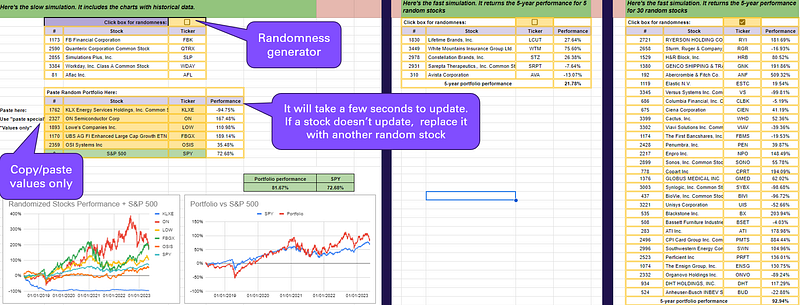

You Can Also Try My Random Stock Portfolio Simulator!

If you feel like playing around with my random portfolio tool, here’s how you can do it:

- Open my Random Stock Portfolio Simulator Google spreadsheet. You might need to request permission, but I will approve it ASAP.

- The first box with stocks generates the random stocks.

- You need to copy/paste these stocks to the yellow box. Make sure you use “paste special” and “values only.” See the screenshot below.

- After pasting, it takes up to 20 seconds to collect the data and update the charts.

- The 2 random stock pickers on the right side don’t generate any charts but provide you with the random portfolio performance immediately.

Conclusion

Even if it is not consistently right, a random portfolio can outperform the average, thanks to convex payoffs that move away from averages and mental biases. I will definitely detail this in the next article.

Note that I don’t advocate for a purely random approach to investing — the goal here is to highlight the importance of being aware of behavioral biases and the potential benefits of incorporating elements of randomness in investment strategies.

By understanding these concepts and playing with my Random Stock Portfolio Simulator, you can gain some insights into why randomness improves a portfolio and become a better investor. 🏆

— Henrique Centieiro 🕺🏻

If you found any value in this article, throw me some Medium love!

🥰 What you can do to support my work: Clap up to 50, leave a message to share your thoughts & be sure to follow. 💌

🚀 Follow my Limitless Investor publication for more valuable content in the future:

🌞 Stay in touch: