Best Stock Market in 20 Years + Worst Economy in 100 Years = Asteroid Ahead!

What investors need to know about the greatest stock market economy dislocation of our generation

The world is simultaneously experiencing the greatest stock market comeback in 20 years while in the depths of the worst economy since the Great Depression.

According to the New York Post, the S&P 500 officially rallied more than 19% — its biggest gain since 1998, at the height of the tech boom. According to the New York Times, in an update to its World Economic Outlook, the I.M.F. said it expected the global economy to shrink 4.9 percent this year — a sharper contraction than the 3 percent it predicted in April.

“Financial market dislocations are circumstances in which financial markets, operating under stressful conditions, cease to price assets correctly in an absolute and relative basis.” — (Pasquariello (2014): Financial Market Dislocations)

The current stock market economy dislocation situation is startling but what I find more troubling are the efforts stock market pundits put into explaining why a financial market dislocation is completely normal.

Stock market economy dislocations may not be uncommon – but they are definitely not normal — and they rarely end well for investors. Without significant improvements to the worldwide economy in the very near future, the current financial market dislocation will have to correct itself, sooner or later.

For the economy to validate the V-shaped stock market recovery we are experiencing, a number of serious economic and political hurdles will have to be overcome in short order. In this article, I will share 4 sobering reasons investors should be paying much closer attention to underlying economic fundamentals and political realities causing one of the worst stock market economy dislocations in history.

In this article;

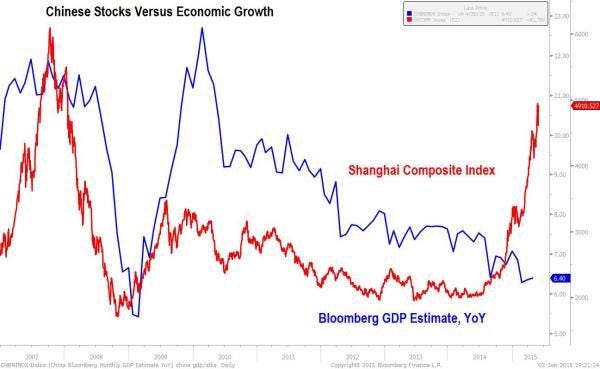

- Financial dislocation — Shanghai, 2015

- 4 reasons investors should be paying closer attention to one of the biggest financial market dislocations in history

- Final thoughts

Financial dislocation — Shanghai, 2015

Only five years ago, China experienced its own stock market dislocation from the underlying economy. Starting in mid-2014, investors with easy access to margin, poured money into the Shanghai stock market. By the spring of 2015, investors had chased stock valuations up to fantastic prices.

Investors ignored the wild PE ratios and underlying economic fundamentals as stock prices relentlessly marched higher. By the fall of 2015, it was all over, ending in disaster for millions of investors around the world. Investors who bought near the top of the dislocation are still out of the money – 5 years after the crash.

“Under such circumstances, stock investors’ mind-sets are not that rational. They don’t look at PEs, the earnings are meaningless.” — James Yip, a fund manager at Shenwan Hongyuan Asset Management — June, 2015

4 reasons investors should be paying closer attention to the current dislocation

1. Credible economists still think things are worsening

The truth is, we are in a worldwide recession. Recessions simply don’t ‘go away’ after a few months. Recessions usually take a couple of years to work through. Contrary to recent comments made by some members of the mainstream media concerning stock prices, the stock market is 3–6 months forward-looking, not 2 years forward-looking. If the recession drags on, stock prices will have to correct.

You can always find someone in the media claiming we are through the worst of the current economic downturn, but credible economists tell us we are still in the very early days of the worst recession since the Great Depression.

Nouriel Roubini

As far back as February 26th, Nouriel Roubini, (affectionally known as ‘Dr. Doom’) claimed a V-shaped economic recovery was ‘delusional’.

Roubini expects a recovery in the 3rd quarter but only because we are recovering from something so terrible. Roubini still thinks we will experience a U or W or even an L recovery, depending on how bad the pandemic resurges this winter.

Roubini thinks the re-hiring of labor will increase the ratio of contract workers. The economy will be facing;

- Negative supply shocks,

- less technological innovation,

- more fiscal deficits,

- and possibly a renewal of stagflation in time.

Mohamed A. El-Erian

Mohamed A. El-Erian expects that more stimulus from the Fed will get harder and harder. Momentum in Congress has slowed considerably.

The Republicans and Mitch McConnell are insisting on liability protections for corporations, so no one can be sued for illness or death caused by catching the virus at work. Democrats want the HEROES act passed, an act that would include more stimulus checks for households and hazard pay for health care workers – something Republicans have said will never see the light of day because it ‘rewards people who don’t want to work’ (Republican Sen. Jim Inhofe).

Mohammed’s investment bets are currently focussing on moral hazard – in this case meaning, investing in companies the Federal Reserve has already guaranteed to bail out. However, Mohammed also still has a lot of money on the side and is not putting new money to work — he suggests if investors are putting money to work, they should be ‘looking for a very strong balance sheet and positive cash flow’.

Ultimately, Mohammed is concerned by the disconnect between the economy and the markets. Last month he penned an article — Bad things happen when finance front-runs the economy. Without significant economic improvement, Mohammed thinks validation of the markets will fail, leading either to more Fed intervention and financial market distortion or markets will have to correct lower.

2. Politics is making future rolling economic shutdowns likely

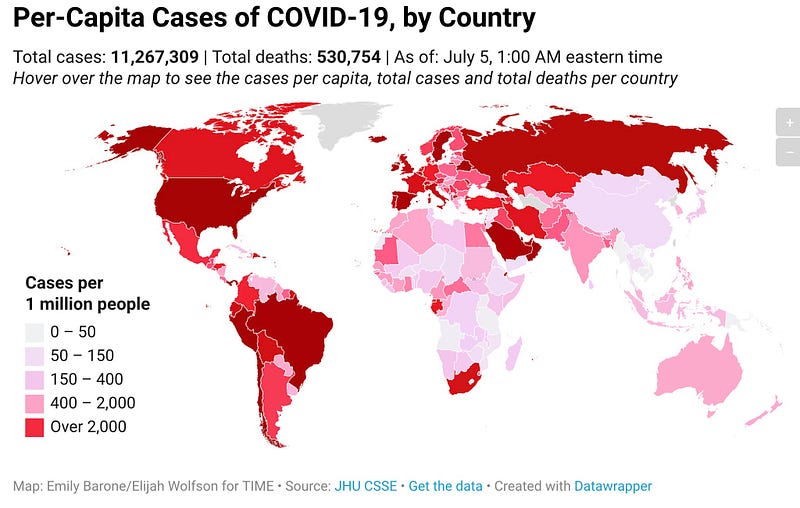

A full 1 in 3 Americans claims they will not take a vaccination once a cure to the current pandemic is found. According to Anthony Fauci, the pandemic cannot be ended if such a large percentage of the population refuses vaccination. However, as badly as America is handling the current pandemic, it seems likely other countries will continue to struggle with their own outbreak issues as well.

Although Japanese citizens generally continue to wear masks in public, social distancing on trains or in tight, small restaurants is nearly impossible. After a short state of emergency, virus infection rates dropped quickly. Yet even with very low levels of testing, it is clear opening the economy has caused virus infection numbers to suddenly increase in the space of only 1 month.

Developing countries are struggling more. Mexico has seen a steady rise in infections since April, now topping 6K cases per day. India also has seen a steady rise in cases since early April. Cases now top 20K per day.

I’ve written before about how difficult it is to develop a vaccine, effective enough to control the pandemic. Without a vaccine, cases will continue to rise in any country or state unable or unwilling to significantly lock down large sections of the economy over long periods of time.

I’ve been told by a number of restaurant owners here in Osaka, that a second state of emergency will bankrupt them. Unfortunately, small business owners around the world are already facing that fate. Medical experts say we are still in the first wave of this pandemic and more difficult-to-control infection clusters are almost certainly on the way this fall and winter.

Unfortunately, knowing all of this, politicians around the world seem determined to ignore the science and push forward with pre-mature economic openings and slow or half-hearted efforts to curb the spread of the pandemic. Without significant changes to the current political climate, it seems the pandemic will be impossible to control.

The question isn’t whether economies will have to shut down again, but how many times will businesses be forced to shut down before a vaccine is widely available? And with more shutdowns, will come more bankruptcies. It is already expected by experts, 2020 bankruptcies will easily rival the Great Recession of 2008–2009. In fact, Edward I. Altman, the creator of the Z score believes 2020 will be a record year for what he refers to as ‘mega-bankrupcies’ — bankruptcies of companies with $1 billion of debt or more.

3. A spending compression will roll through many industries

And a record-breaking series of bankruptcies could easily turn into an economic compression. Although median income growth has steadily decreased since the 1980s, the economy was near a cyclical high before the pandemic struck. (See graphic below).

With 10s of millions out of work and a serious possibility of pandemic-related unemployment payments and a ban on eviction notices coming to an end this month, we could see serious downward pressure on the economy as we did in 2009.

San Francisco renters are already breaking leases in record numbers. About 1 in 13 renters have already broken lease agreements to find better deals or to avoid eviction. In June, rent prices dropped more than 9% in San Francisco, year over year. We are seeing similar problems in a number of expensive urban markets. Downward price pressures could easily spread to other sectors of the economy as businesses compete for dwindling numbers of customers, spending smaller amounts of money.

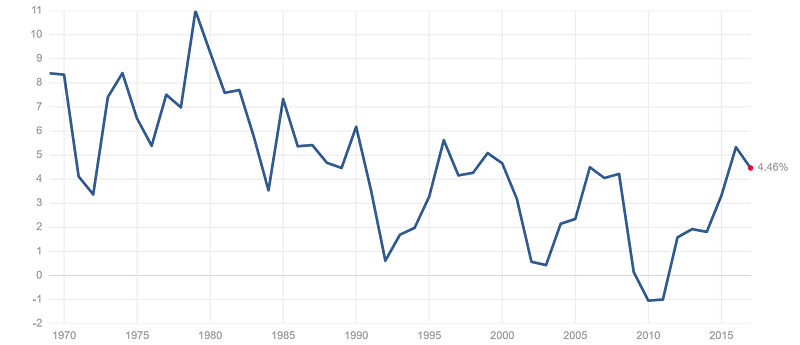

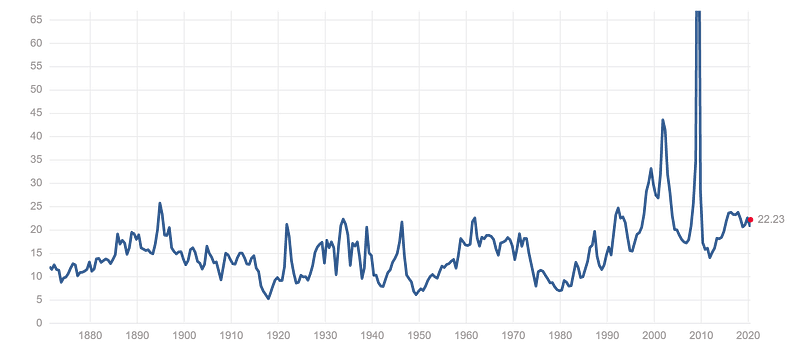

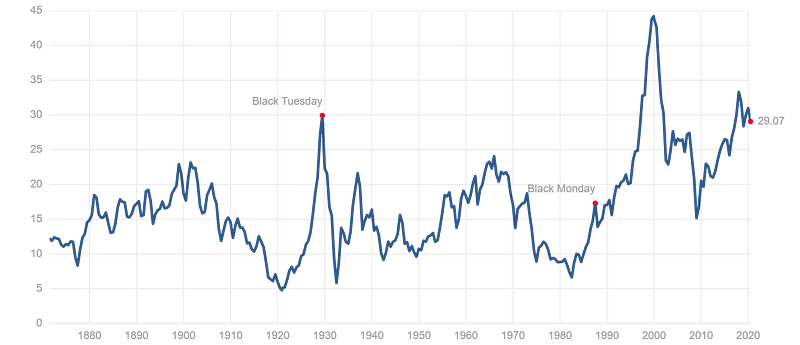

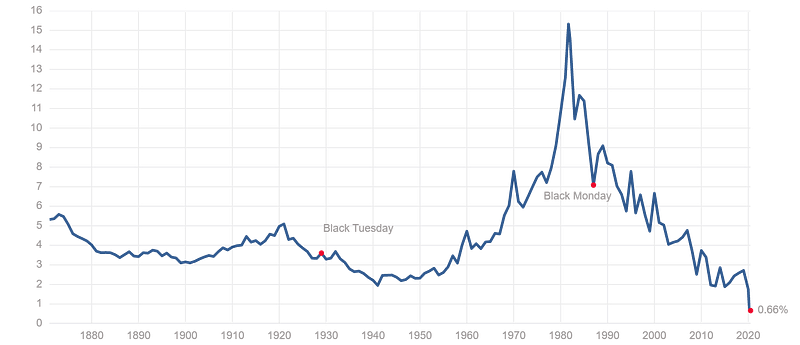

4. Underlying economic fundamentals do not look encouraging

S&P 500 PE Ratio

- We can clearly see 4 cyclical PE Ratio events starting from the mid-1800s until today. It appears we are on the tail-end of the 4th PE Ratio cycle. If history is any guide, we could see PE ratios fall from around 20, today, to 10 or less over the next decade. Could we see a lost decade the way Japan did after it’s bubble economy burst in the early 1990s or stagflation like North America faced in the 1970s?

Shiller PE Ratio

- Only 2 times in history has the Shiller PE Ratio been so high — 1929 (Black Monday was the start of a massive stock market crash that lead to the Great Depression) and 1999 (the peak of the dot.com bubble). Clearly, we are in dangerous territory as stock markets continue to rally.

10-year treasury

- Treasury rates spiked in the early 1980s to kill stagflation, however historically, rates have floated between 5 and 2%. Today’s rates are unprecedented at sub 1%. Again, you have to look at Japan’s post-bubble economy to see anything similar.

- The unprecedented low 10-year yield is forcing conservative investors into stocks. This pushes up stock prices but when conservative investors start experiencing massive losses, how long do you think they will hold out before throwing in the towel?

Retail Sales

- Retail sales have seen a predictable bounce off the pandemic shut-down lows. Where do they go from here if we continue to see rolling shutdowns over the next year or two? Most economists are suggesting sideways. If so, earnings will continue to be depressed for the foreseeable future.

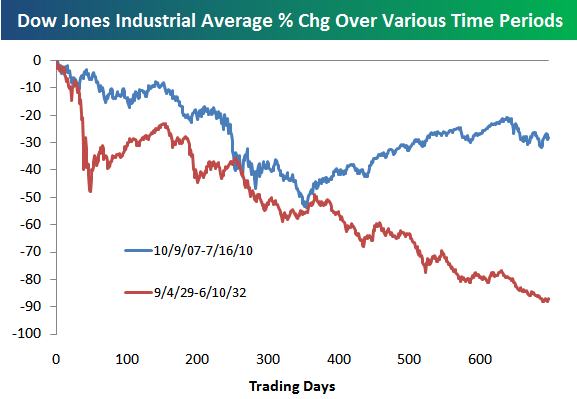

Markets from history

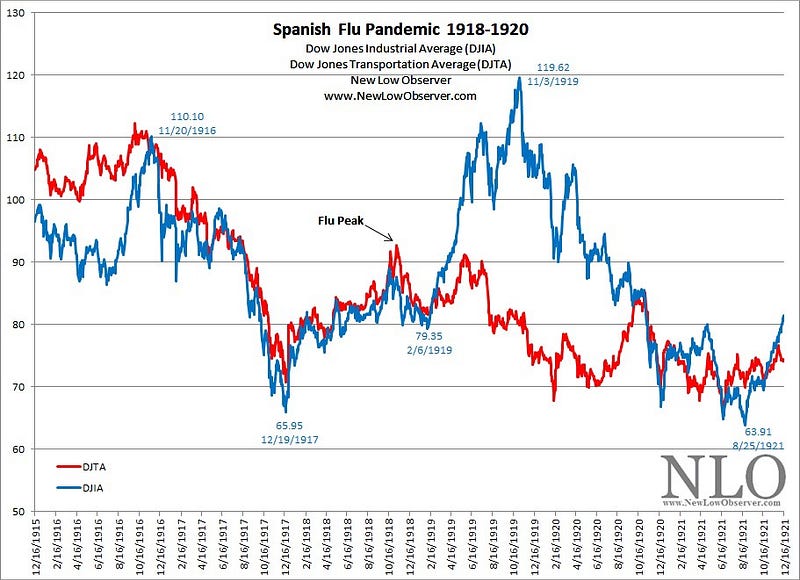

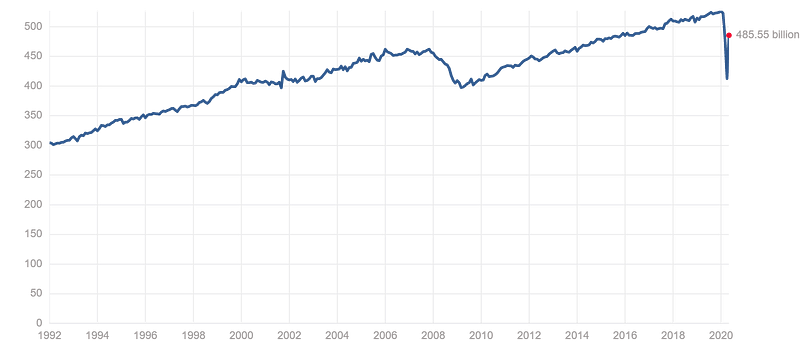

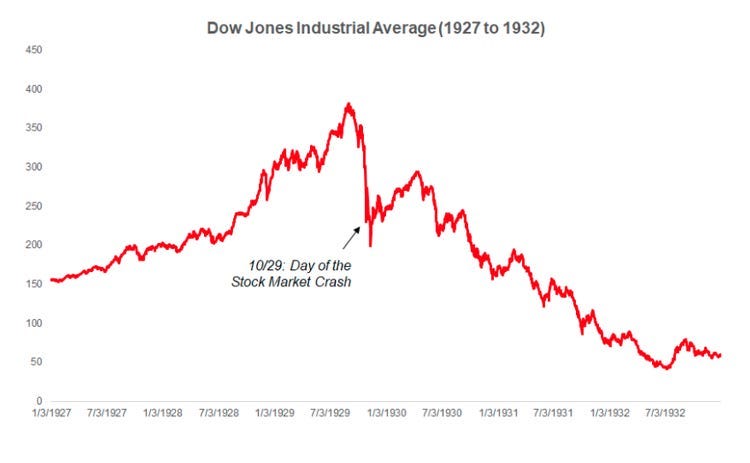

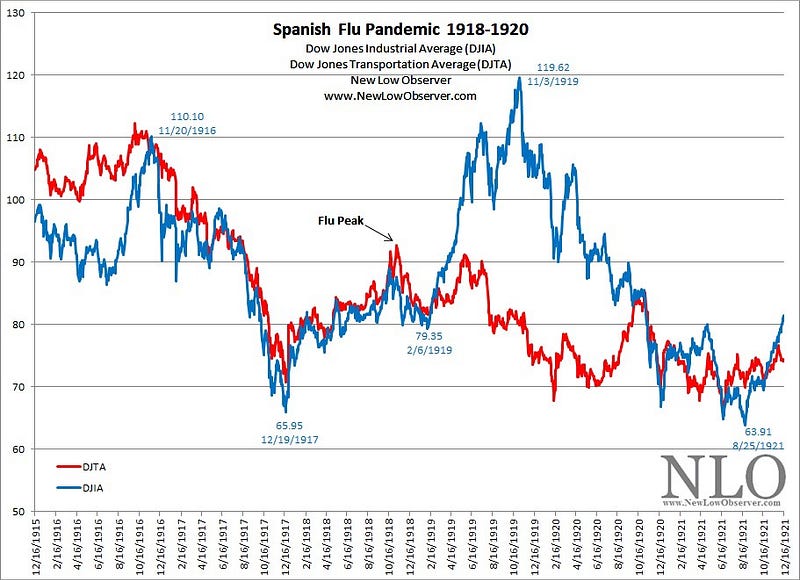

No two markets are the same but if history is any guide, we are a long way from being out of the woods. Below, I’ve displayed the crash of 1929, the Spanish flu pandemic of 1918, and the current Nasdaq and DOW indexes for your review and consideration.

It’s interesting to note, the real damage to the financial markets didn’t occur until after the peak of the Spanish flu pandemic had been passed in October of 1918. Following the peak of flu cases, both the DJIA and DJTA double-dipped, and in fact, both indexes ultimately dropped to new lows before recovering.

Final thoughts

- A deepening trade war with China,

- record-breaking unemployment,

- China’s political takeover of Hong Kong, currently one of the most influential financial centers of Asia,

- social unrest continuing to simmer across North America, with demands for sweeping police reform in America and Canada which could easily lead to significant political change in the near future,

- at last count, 132K deaths in the largest economy in the world and 537K deaths worldwide in the first wave of a global pandemic,

- Near $0 household savings with individual stimulus checks and pandemic-related unemployment benefits coming to an end in a matter of weeks.

Even one of these events in ‘normal’ times would cause markets to tumble. However, investors continue to look past all of this terrible news because the Federal Reserve has increased its balance sheet to levels never imagined.

The simple explanation offered by the media is, ‘stock markets tend to rise and fall with the inflating and deflating of the Federal Reserve balance sheet’. I get it, who doesn’t love a simple story? Cause and effect is so much easier to understand than domino theory, or ripple effect. Nevertheless, let’s speculate what would cause the Federal Reserve to expand its balance sheet so dramatically in such a short period of time.

Through the monetary tools at its disposal, the Federal Reserve attempts to smooth the booms and busts of the economic cycle and maintain adequate bases of money and credit for current production levels. — Investopedia

Investors need to understand the job of the Federal Reserve is to smooth the economic cycle, not the stock markets. At one point earlier this year, there were no offers for some fixed-income investments, meaning there was no market for a significant number of fixed income products (see video below for details – jump ahead to 1:40). The Federal Reserve had no choice but to step into the fixed income markets – not to boost bond prices, but as a last-ditch, throw-in-the-kitchen-sink attempt to avoid a total collapse of the economy.

The Federal Reserve has already pumped in more stimulus in a matter of weeks than throughout the entire Great Recession and recovery. $7 trillion has already been flooded into the markets and Wall Street expects this to rise to nearly $10 trillion dollars before all is said and done.

I don’t know how much more stimulus is in the cards, however, this central bank reaction was triggered because economies around the world are severely damaged and likely to get much worse before they get better. If more stimulus is needed, it’s not because the economy has recovered. The current bull trap and FANG bubble is simply a side-effect of the central banks trying to save a very distressed and destabilized world economy.

The Federal Reserve continues to fight 3 serious problems and none of them look easy to fix;

- REITs, airlines, and energy companies were over-leveraged before the pandemic. Debt continues to accumulate as the pandemic continues and oil prices remain low, making future profitability extremely challenging and bankruptcy more and more likely.

- No amount of QE will stop the pandemic. Only shutting down an economy and remaining partially shut down after gaining control of the virus outbreak will keep infection numbers manageable — for many politicians, this is a political impossibility.

- It looks increasingly unlikely Congress and the Senate will be unable to agree on an appropriate rescue package to help support the QE of the Federal Reserve.

Big questions investors should be thinking about

First, if the economy were to unexpectedly start recovering in a V-shaped fashion, there would be no need for more central bank intervention, right? The question investors need to start asking themselves is, ‘what happens to financial markets if the central banks do start pulling back support?’ Alternatively, if as Wall Street is expecting, the Federal Reserve is going to pump in another $2.8 billion of stimulus to support corporate debt markets, then what the hell is so terribly wrong with the economy?

Second, many investors appear to have an unshakable belief the government will not let businesses go broke. This is simply not the case. As mentioned before, we are running at record-breaking bankruptcy numbers. Any bricks and mortar retailer, any travel, hotel, or restaurant-related business is in for a very difficult time for the foreseeable future. A very large percentage of households continue to live month-to-month with no significant savings. The number of personal and business bankruptcies before this pandemic is over can only go up from here.

Call me crazy, but additional record-breaking stimulus to fight a record-breaking number of bankruptcies does not sound like the makings of a V-shaped economic recovery to me. It sounds like basic survival.

ASTEROID AHEAD! …

Disclosure — I hold approximately 95% cash as I publish this article. Please seek professional advice before making any investment decisions.

If you found this article useful, please forward it to someone you care about.

I’m Edward Iftody — If you’d like to learn more about disruptive investing, I encourage you to read more at www.blockchainin.Asia