Bayesian Time Series Forecasting in Python with the Uber’s Orbit Package

An easy-to-follow guide of benchmarking Bayesian models to forecast univariate time series data

“The quest for certainty in forecasting outcomes can be the enemy of progress.” — Nate Silver

- Time series forecasting makes predictions for future data and outcomes based on time-stamped past data collected over specified intervals of time.

- Traditional time series forecasting methods rely on deterministic models to predict point forecasts as single-valued predictions of future values.

- In contrast, Bayesian methods treat the model parameters as random variables with known prior distributions. Therefore, these methods quantify the uncertainty associated with the predictions.

- Read more about Bayesian Structural Time Series (BSTS) vs ARIMA here [5].

- In this post, we’ll walk through practical aspects of benchmarking Orbit for Bayesian time series forecasting, while utilizing probabilistic programming packages like PyStan and Uber’s own Pyro under the hood [1–4].

- Orbit currently supports the the following forecasting models:

Exponential Smoothing (ETS), Damped Local Trend (DLT), and Local Global Trend (LGT).

- Blog: Introducing Orbit, An Open Source Package for Time Series Inference and Forecasting GitHub: https://github.com/uber/orbit Documentation: Orbit’s Documentation Paper: Orbit: Probabilistic Forecast with Exponential Smoothing

- Install Orbit from PyPi

!pip install orbit-ml

- Orbit has a wide range of applications in Uber’s marketing data science team for measurement, planning, and forecasting. The latter is an important part of planning future marketing budgets and the optimization of spending across different channels and regions.

Contents

- Grocery Store Sales Forecasting

- Working with US Unemployment Benefits

Let’s delve into the aforementioned list of representative Orbit case studies to discover how analysts and data scientists from various industries can harness the power of Bayesian models.

Grocery Store Sales Forecasting

Input Store Sales Data

- The Kaggle dataset will be used to predict sales for the thousands of product families sold at Favorita stores located in Ecuador. The training data includes dates, store and product information, whether that item was being promoted, as well as the sales numbers.

- For the sake of simplicity, let’s use Orbit to process only one store [1].

Preparing Training/Validation Data

- Importing libraries, reading the input dataset and selecting one store

import orbit

from orbit.models import DLT, ETS

from orbit.diagnostics.backtest import BackTester

import pandas as pd

import numpy as np

# Auxiliary WMAPE function

def wmape(y_true, y_pred):

return np.abs(y_true - y_pred).sum() / np.abs(y_true).sum()

path = 'train.csv'

data = pd.read_csv(path, index_col='id', parse_dates=['date'])

# General data structure

data.tail()

date store_nbr item_nbr unit_sales onpromotion

id

125497035 2017-08-15 54 2089339 4.0 False

125497036 2017-08-15 54 2106464 1.0 True

125497037 2017-08-15 54 2110456 192.0 False

125497038 2017-08-15 54 2113914 198.0 True

125497039 2017-08-15 54 2116416 2.0 False

data.info()

<class 'pandas.core.frame.DataFrame'>

Index: 125497040 entries, 0 to 125497039

Data columns (total 5 columns):

# Column Dtype

--- ------ -----

0 date datetime64[ns]

1 store_nbr int64

2 item_nbr int64

3 unit_sales float64

4 onpromotion object

dtypes: datetime64[ns](1), float64(1), int64(2), object(1)

memory usage: 5.6+ GB

# Selecting store_nbr == 1

data2 = data.loc[((data['store_nbr'] == 1)), ['date', 'unit_sales', 'onpromotion']]

# Selecting training and validation sets

dec25 = list()

for year in range(2013,2017):

dec18 = data2.loc[(data2['date'] == f'{year}-12-18')]

dec25 += [{'date': pd.Timestamp(f'{year}-12-25'), 'unit_sales': dec18['unit_sales'].values[0], 'onpromotion': dec18['onpromotion'].values[0]}]

data2 = pd.concat([data2, pd.DataFrame(dec25)], ignore_index=True).sort_values('date')

train = data2.loc[data2['date'] < '2017-01-01']

valid = data2.loc[(data2['date'] >= '2017-01-01') & (data2['date'] < '2017-04-01')]

df_daily = train.set_index('date').resample('D')["unit_sales"].sum().to_frame()

df_daily.tail()

unit_sales

date

2016-12-27 12157.823

2016-12-28 12144.918

2016-12-29 10244.317

2016-12-30 13584.621

2016-12-31 10741.060Training the ETS Model

- Training the Bayesian Exponential Smoothing (ETS) model that makes use of prior knowledge in order to update their beliefs as new data becomes available.

ets = ETS(date_col='date',

response_col='unit_sales',

seasonality=7,

prediction_percentiles=[5, 95],

seed=1)

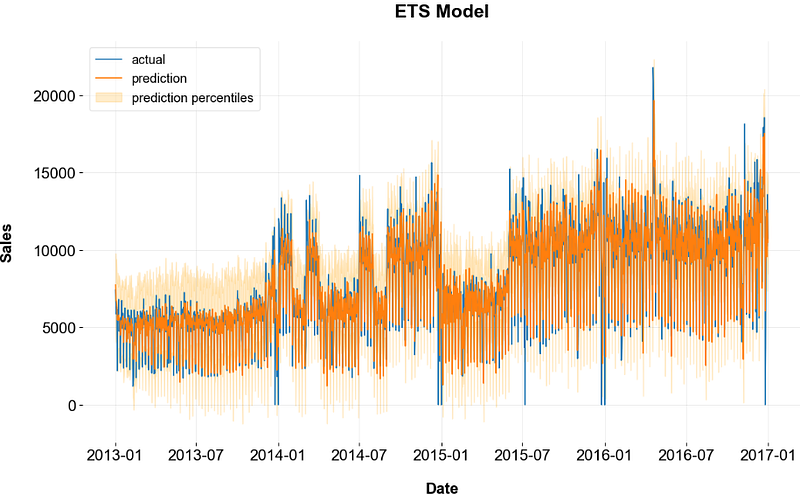

ets.fit(df=df_daily)- Making the ETS in-sample forecast for the training set and plotting the result

p = ets.predict(df=df_daily)

p.tail()

date prediction_5 prediction prediction_95

1455 2016-12-27 7802.727003 10143.287793 12110.888725

1456 2016-12-28 10014.508206 12579.779372 15058.306455

1457 2016-12-29 7358.604807 9569.571616 12158.040635

1458 2016-12-30 9646.606625 12375.098597 14963.530262

1459 2016-12-31 8467.247376 10494.881238 14305.702144

plt.figure(figsize=(15,6))

plt.plot(p['date'],p['prediction'])

plt.plot(p['date'],df_daily['unit_sales'])

- Making the ETS out-of-sample forecast for the validation set and plotting the result

forecast_df = pd.DataFrame({"date": pd.date_range(start='2017-01-01', end='2017-03-31', freq='D')})

p = ets.predict(df=forecast_df)

p = p.merge(valid, on='date', how='left')

import matplotlib.pyplot as plt

fig, ax = plt.subplots(1,1, figsize=(1280/96, 720/96))

ax.plot(p['date'], p['sales'], label='actual')

ax.plot(p['date'], p['prediction'], label='prediction')

ax.fill_between(p['date'], p['prediction_5'], p['prediction_95'], alpha=0.2, color='orange', label='prediction percentiles')

ax.set_title('Error, Trend, Seasonality (ETS)')

ax.set_ylabel('Sales')

ax.set_xlabel('Date')

ax.legend()

plt.show()

Training the DLT Model

- Let’s look at the Damped Local Trend (DLT) Model. DLT is one of the main exponential smoothing models supported in Orbit. The model is a fusion between the classical ETS (Hyndman et. al., 2008)) with some refinement leveraging ideas from Rlgt (Smyl et al., 2019).

- Training the DLT model with backtesting and checking various trend options by comparing their WMAPE scores

scores = dict()

for global_trend_option in ['linear', 'loglinear', 'flat', 'logistic']:

dlt = DLT(date_col='date',

response_col='sales',

seasonality=7,

prediction_percentiles=[5, 95],

regressor_col=['onpromotion'],

regressor_sign=['='],

regression_penalty='auto_ridge',

damped_factor=0.8,

seed=2, # if you get errors due to less than zero values, try a different seed

global_trend_option=global_trend_option,

verbose=False)

bt = BackTester(df=train,

model=dlt,

forecast_len=90,

n_splits=5,

window_type='rolling')

bt.fit_predict()

predicted_df=bt.get_predicted_df()

scores[global_trend_option] = wmape(predicted_df['actual'], predicted_df['prediction'])

print (scores)

{'logistic': 0.1870392532742924}

best_global_trend_option = min(scores, key=scores.get)

print (best_global_trend_option)

logistic- Preparing the trained data

df_daily = train.set_index('date').resample('D')["unit_sales"].sum().to_frame()

df_daily11 = train.set_index('date').resample('D')["onpromotion"].sum()

df_daily11.tail()

date

2016-12-27 259

2016-12-28 502

2016-12-29 258

2016-12-30 424

2016-12-31 252

Freq: D, Name: onpromotion, dtype: object

df_daily1.set_index('date')

df_daily1['date1'] = df_daily1['date']

df_daily1.set_index('date1')

df_daily = pd.concat([df_daily, df_daily1["onpromotion"]], axis=1)

df = df_daily.reset_index()

df.tail()

date unit_sales

1455 2016-12-27 12157.823

1456 2016-12-28 12144.918

1457 2016-12-29 10244.317

1458 2016-12-30 13584.621

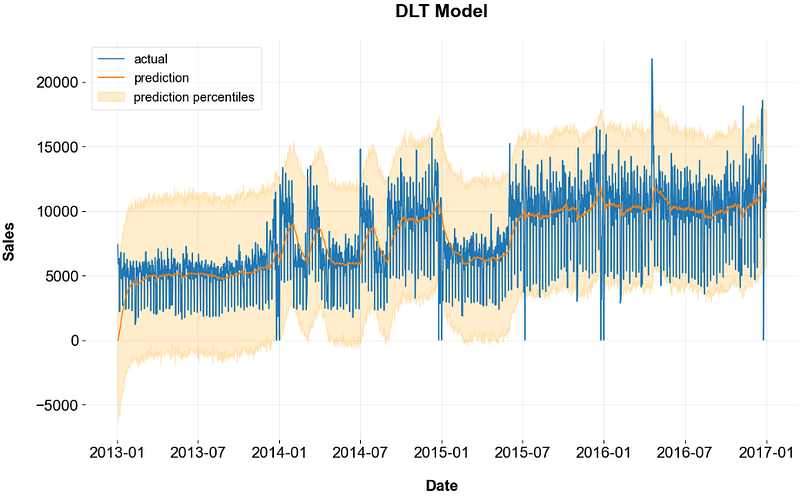

1459 2016-12-31 10741.060- Fitting and predicting the trained data

dlt = DLT(

response_col='unit_sales',

date_col='date',

estimator='stan-map',

seasonality=52,

seed=8888,

global_trend_option='logistic',

# for prediction uncertainty

n_bootstrap_draws=1000,

)

dlt.fit(df)

p1 = dlt.predict(df)

p1.tail()

date prediction_5 prediction prediction_95

1455 2016-12-27 5459.263164 11730.18620 17904.642854

1456 2016-12-28 5672.749046 11715.39130 17625.631483

1457 2016-12-29 5819.880134 11716.52832 17927.297250

1458 2016-12-30 5553.716924 11625.78863 17753.949989

1459 2016-12-31 5770.091870 11692.68270 17509.058712- Plotting the trained data

fig, ax = plt.subplots(1,1, figsize=(1280/96, 720/96))

ax.plot(p1['date'], df['unit_sales'], label='actual')

ax.plot(p1['date'], p1['prediction'], label='prediction')

ax.fill_between(p1['date'], p1['prediction_5'], p1['prediction_95'], alpha=0.2, color='orange', label='prediction percentiles')

ax.set_title('DLT Model')

ax.set_ylabel('Sales')

ax.set_xlabel('Date')

ax.legend()

plt.show()

- Let’s train/fit the DLT model with the logistic trend and make predictions on the validation set

dlt = DLT(date_col='date',

response_col='sales',

seasonality=7,

prediction_percentiles=[5, 95],

regressor_col=['onpromotion'],

regressor_sign=['='],

regression_penalty='auto_ridge',

damped_factor=0.8,

seed=2, # if you get errors due to less than zero values, try a different seed

global_trend_option=best_global_trend_option,

verbose=False)

dlt.fit(df=train)

p = dlt.predict(df=valid[['date', 'onpromotion']])

p = p.merge(valid, on='date', how='left')

print(wmape(p['sales'], p['prediction']))

0.20177138495275543

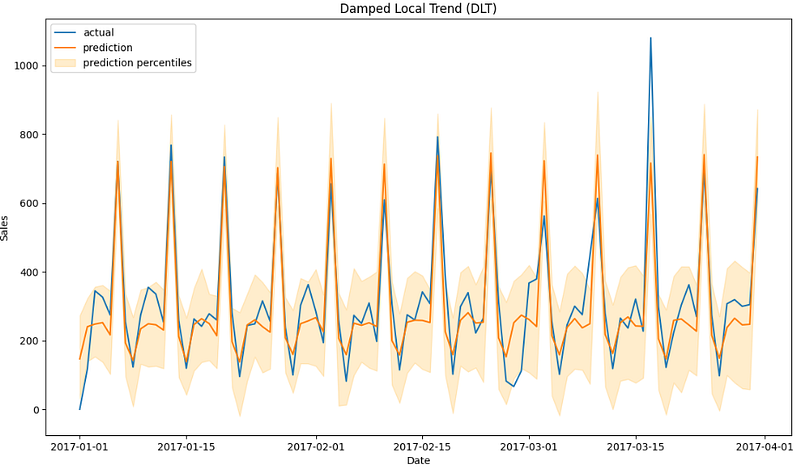

fig, ax = plt.subplots(1,1, figsize=(1280/96, 720/96))

ax.plot(p['date'], p['sales'], label='actual')

ax.plot(p['date'], p['prediction'], label='prediction')

ax.fill_between(p['date'], p['prediction_5'], p['prediction_95'], alpha=0.2, color='orange', label='prediction percentiles')

ax.set_title('Damped Local Trend (DLT)')

ax.set_ylabel('Sales')

ax.set_xlabel('Date')

ax.legend()

plt.show()

- We can see a remarkable similarity between the ETS and DLT predictions on both training and validation sets.

- It turns out that the KTR model yields the less accurate result (in terms of WMAPE) on the validation data

from orbit.models import KTR

ktr = KTR(date_col='date',

response_col='sales',

seasonality=[7, 28],

prediction_percentiles=[5, 95],

regressor_col=['onpromotion'],

seed=2,

verbose=False)

ktr.fit(df=train)

p = ktr.predict(df=valid[['date', 'onpromotion']])

p = p.merge(valid, on='date', how='left')

print(wmape(p['sales'], p['prediction']))

0.23352631577089197Working with US Unemployment Benefits

- Following the Orbit demo example, let’s address a forecast task on the iclaims dataset.

- The iclaims data contains the weekly initial claims for US unemployment benefits against a few related google trend queries from Jan 2010 — June 2018. This aims to demo a similar dataset from the Bayesian Structural Time Series (BSTS) model (Scott and Varian 2014).

- Importing the necessary Python libraries

import pandas as pd

import numpy as np

import orbit

import matplotlib.pyplot as plt

from orbit.utils.dataset import load_iclaims

from orbit.diagnostics.plot import plot_predicted_data, plot_predicted_components

from orbit.utils.plot import get_orbit_style

plt.style.use(get_orbit_style())

from orbit.models import ETS

orbit.__version__

'1.1.4.2'- Loading the log-log transformed weekly input data

raw_df = load_iclaims(transform=True)

raw_df.dtypes

week datetime64[ns]

claims float64

trend.unemploy float64

trend.filling float64

trend.job float64

sp500 float64

vix float64

dtype: object

df = raw_df.copy()

df.head()

week claims trend.unemploy trend.filling trend.job sp500 vix

0 2010-01-03 13.386595 0.219882 -0.318452 0.117500 -0.417633 0.122654

1 2010-01-10 13.624218 0.219882 -0.194838 0.168794 -0.425480 0.110445

2 2010-01-17 13.398741 0.236143 -0.292477 0.117500 -0.465229 0.532339

3 2010-01-24 13.137549 0.203353 -0.194838 0.106918 -0.481751 0.428645

4 2010-01-31 13.196760 0.134360 -0.242466 0.074483 -0.488929 0.487404

# Train/test data split

test_size=52

train_df=df[:-test_size]

test_df=df[-test_size:]Training the ETS Model

- Training, fitting the ETS model and predicting the train/test data

ets = ETS(

response_col='claims',

date_col='week',

seasonality=52,

seed=2020,

estimator='stan-mcmc',

)

ets.fit(train_df)

predicted_df = ets.predict(df=df, decompose=True)

predicted_df

week prediction_5 prediction prediction_95 trend_5 trend trend_95 seasonality_5 seasonality seasonality_95

0 2010-01-03 13.256093 13.386911 13.498341 12.922438 13.061019 13.179558 0.283892 0.324221 0.371806

1 2010-01-10 13.514679 13.625450 13.737572 12.959882 13.065062 13.158126 0.490289 0.562439 0.634173

2 2010-01-17 13.254438 13.382063 13.558862 12.943429 13.057401 13.205435 0.239650 0.324396 0.402475

3 2010-01-24 13.000500 13.158529 13.272095 12.917984 13.060074 13.169505 -0.006310 0.095894 0.171658

4 2010-01-31 13.052791 13.174475 13.322294 12.934345 13.077561 13.169154 0.017701 0.120735 0.213370

... ... ... ... ... ... ... ... ... ... ...

438 2018-05-27 12.119949 12.338702 12.548791 12.229486 12.443958 12.647680 -0.112899 -0.098516 -0.081082

439 2018-06-03 12.072402 12.280543 12.462557 12.238955 12.445619 12.640632 -0.183100 -0.169004 -0.147315

440 2018-06-10 12.147087 12.372973 12.578345 12.200795 12.442474 12.634412 -0.082059 -0.067508 -0.048729

441 2018-06-17 12.146767 12.328751 12.557206 12.239426 12.424625 12.657444 -0.112707 -0.097486 -0.077062

442 2018-06-24 12.183477 12.404675 12.562173 12.221322 12.457154 12.611574 -0.064576 -0.048535 -0.027940

443 rows × 10 columns- Plotting the above train/test data predictions vs actual data

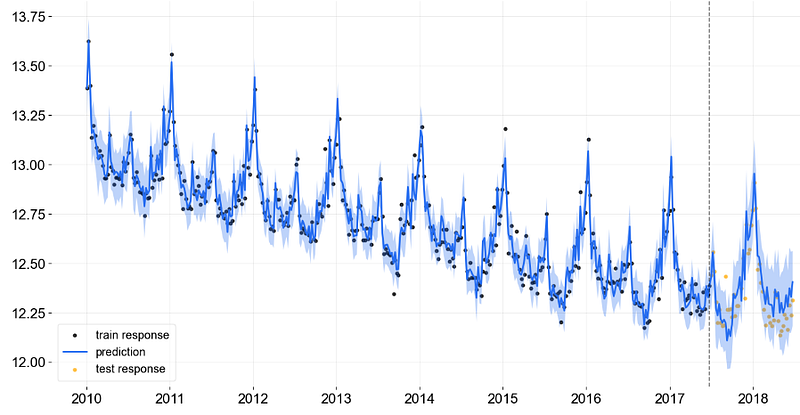

_ = plot_predicted_data(training_actual_df=train_df,

predicted_df=predicted_df,

date_col='week',

actual_col='claims',

test_actual_df=test_df)

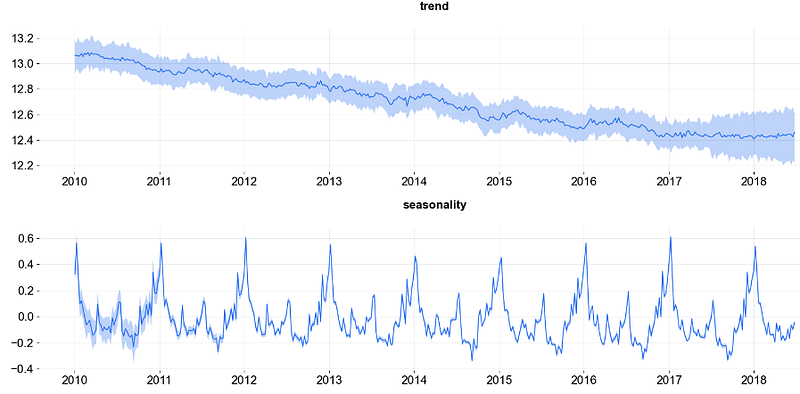

- Plotting the predicted trend and seasonality components for the entire dataset

_ = plot_predicted_components(predicted_df=predicted_df, date_col='week')

- Analyzing the ETS posterior prediction samples

posterior_samples = ets.get_posterior_samples()

posterior_samples.keys()

dict_keys(['l', 'lev_sm', 'obs_sigma', 's', 'sea_sm', 'loglk'])- Posterior predictive checks (PPCs) are a great way to validate a model. The idea is to generate data from the model using parameters from draws from the posterior.

- In doing so, we need a Python package for exploratory analysis of Bayesian models. ArviZ includes functions for posterior analysis, data storage, sample diagnostics, model checking, and comparison.

- Installing ArviZ using pip

!pip install arviz

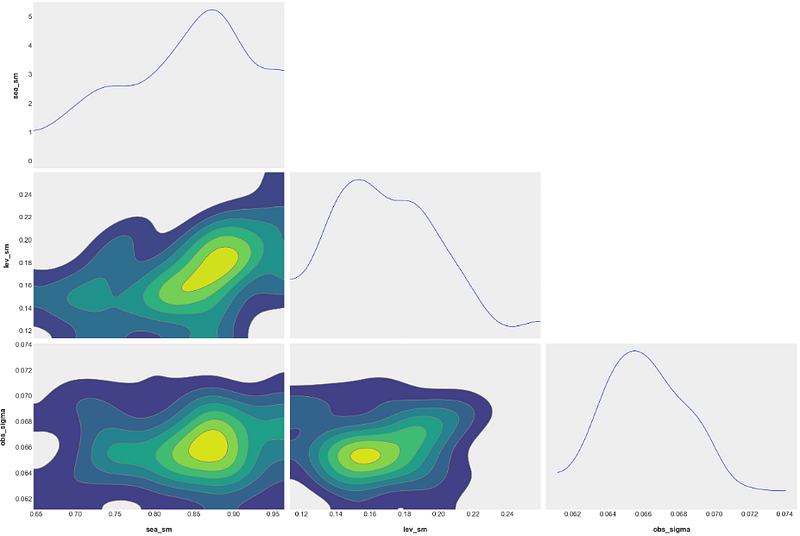

- Plotting the ETS posterior samples “sea_sm”, “lev_sm”, and “obs_sigma”

import arviz as az

posterior_samples = ets.get_posterior_samples(permute=False)

# example from https://arviz-devs.github.io/arviz/index.html

az.style.use("arviz-darkgrid")

az.plot_pair(

posterior_samples,

var_names=["sea_sm", "lev_sm", "obs_sigma"],

kind="kde",

marginals=True,

textsize=15,

)

plt.show()

- The above semi-unimodal distributions quantify the “uniqueness of fit”. That is, these probability density plots quantify how much model “ambiguity” there is when choosing from the possible interpretations.

Training the LGT Model

- Let’s evaluate the Local Global Trend (LGT) model. It converts an additive log-transformed response into a multiplicative model with some advantages (Ng and Wang et al., 2020).

- Specifically, the Orbit’s LGT model is a variant based on the multiplicative model proposed by Smyl in Rlgt. Its advantages over the original Rlgt models are two-fold: first, the computation is more effective with the additive form; second, in Rlgt is parameterized with that introduces dependency in noise generation, while is refined as an independent noise in LGT.

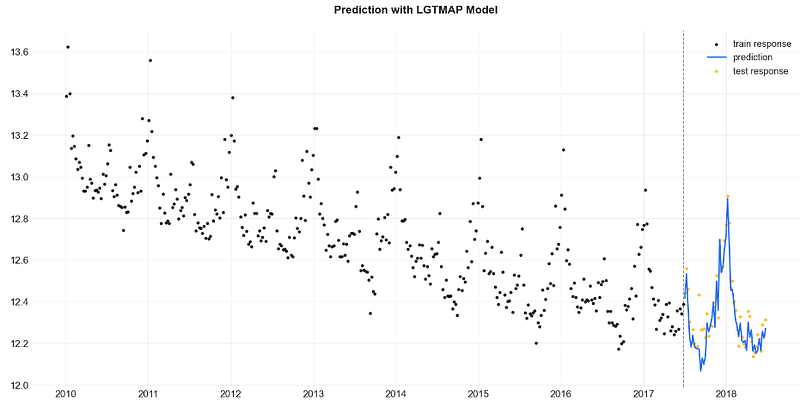

- Importing libraries, loading the input dataset, train/test data split, training the LGT+MAP model and validating the LGT+MAP model predictions on test data

#Imports

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import orbit

from orbit.models import LGT

from orbit.diagnostics.plot import plot_predicted_data

from orbit.diagnostics.plot import plot_predicted_components

from orbit.utils.dataset import load_iclaims

# load data

df = load_iclaims()

# define date and response column

date_col = 'week'

response_col = 'claims'

df.dtypes

test_size = 52

train_df = df[:-test_size]

test_df = df[-test_size:]

lgt = LGT(

response_col=response_col,

date_col=date_col,

estimator='stan-map',

seasonality=52,

seed=8888,

)

lgt.fit(df=train_df)

predicted_df = lgt.predict(df=test_df)

_ = plot_predicted_data(training_actual_df=train_df, predicted_df=predicted_df,

date_col=date_col, actual_col=response_col,

test_actual_df=test_df, title='Prediction with LGTMAP Model')

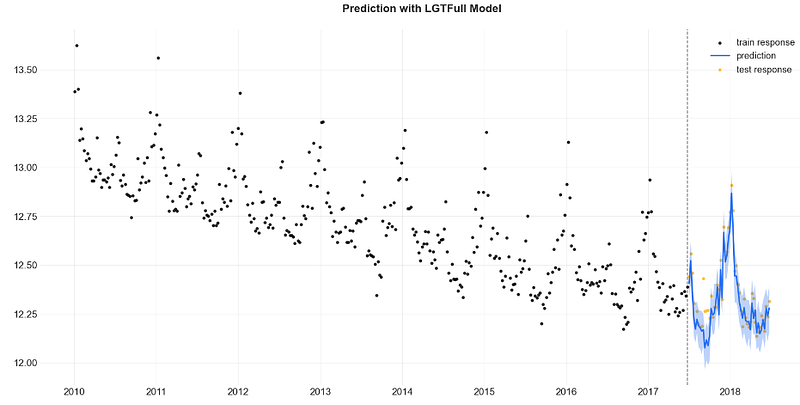

- Training the LGT model with MCMC sampling (default) and validating the LGT+MCMC model (ref. LGTFull) predictions on test data

#LGT - MCMC

lgt = LGT(

response_col=response_col,

date_col=date_col,

seasonality=52,

seed=8888,

)

%%time

lgt.fit(df=train_df)

2023-12-03 15:57:45 - orbit - INFO - Sampling (PyStan) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

CPU times: total: 281 ms

Wall time: 8.72 s

<orbit.forecaster.full_bayes.FullBayesianForecaster at 0x1f540348130>

predicted_df = lgt.predict(df=test_df)

predicted_df.tail(5)

week prediction_5 prediction prediction_95

47 2018-05-27 12.128395 12.218377 12.314531

48 2018-06-03 12.070700 12.171635 12.344855

49 2018-06-10 12.153305 12.278967 12.377019

50 2018-06-17 12.108882 12.239528 12.335686

51 2018-06-24 12.158394 12.278686 12.394868

lgt.get_posterior_samples().keys()

dict_keys(['l', 'b', 'lev_sm', 'slp_sm', 'obs_sigma', 'nu', 'lgt_sum', 'gt_pow', 'lt_coef', 'gt_coef', 's', 'sea_sm', 'loglk'])

_ = plot_predicted_data(training_actual_df=train_df, predicted_df=predicted_df,

date_col=lgt.date_col, actual_col=lgt.response_col,

test_actual_df=test_df, title='Prediction with LGTFull Model')

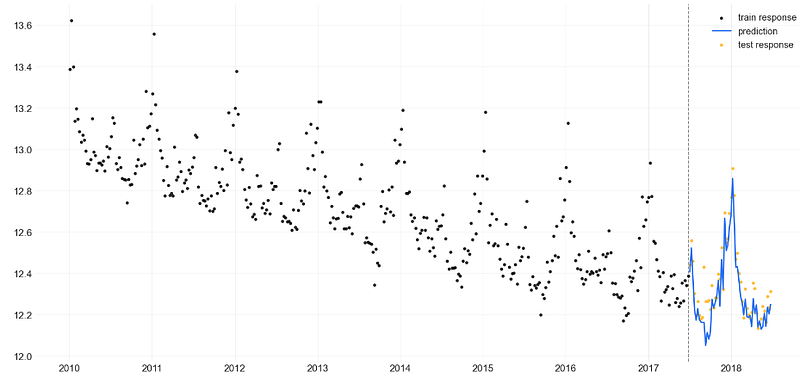

- Training the LGT model with the mean point estimate method and validating the LGTAggregated model predictions on test data

#LGT - point estimate

lgt = LGT(

response_col=response_col,

date_col=date_col,

seasonality=52,

seed=8888,

)

lgt.fit(df=train_df, point_method='mean')

2023-12-03 16:05:48 - orbit - INFO - Sampling (PyStan) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

predicted_df = lgt.predict(df=test_df)

_ = plot_predicted_data(training_actual_df=train_df, predicted_df=predicted_df,

date_col=lgt.date_col, actual_col=lgt.response_col,

test_actual_df=test_df, title='Prediction with LGTAggregated Model')

- Observe a remarkable similarity between the LGTMAP and LGTFull model predictions on the test set.

- Notice the least accurate LGTAggregated model predictions on the test set as compared to the LGTMAP and LGTFull validation results.

Training the DLT Regression Model

- Let’s examine the DLT regression option of log-transformed iclaims data with the following obligatory settings

response_col = 'claims'

date_col = 'week'

regressor_col = ['trend.unemploy', 'trend.filling', 'trend.job']- Importing libraries, loading the input dataset, train/test set splitting, training the DLT model, and making in-sample predictions of the training set with decompose=True

%matplotlib inline

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import orbit

from orbit.models import DLT

from orbit.diagnostics.plot import plot_predicted_data,plot_predicted_components

from orbit.utils.dataset import load_iclaims

import warnings

warnings.filterwarnings('ignore')

print(orbit.__version__)

1.1.4.2

# load log-transformed data

df = load_iclaims()

# train/test split

train_df = df[df['week'] < '2017-01-01']

test_df = df[df['week'] >= '2017-01-01']

# regression parameters

response_col = 'claims'

date_col = 'week'

regressor_col = ['trend.unemploy', 'trend.filling', 'trend.job']

#training the model

dlt = DLT(

response_col=response_col,

regressor_col=regressor_col,

date_col=date_col,

seasonality=52,

prediction_percentiles=[5, 95],

)

dlt.fit(train_df)

2023-12-03 16:09:08 - orbit - INFO - Sampling (PyStan) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

#making in-sample predictions of the training set

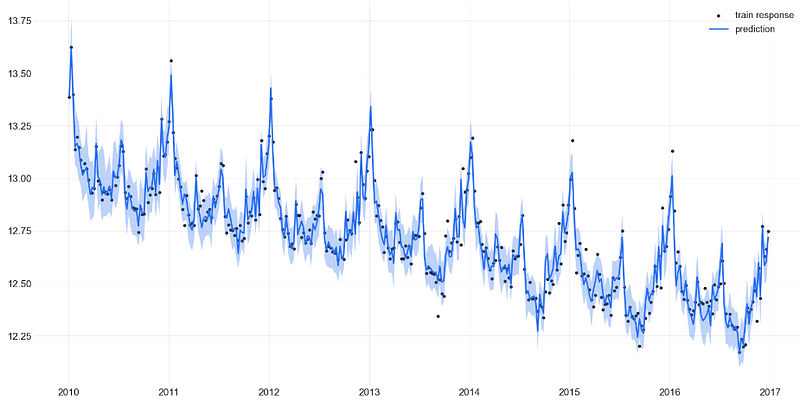

predicted_df = dlt.predict(df=train_df, decompose=True)

#plotting in-sample predictions of the training set

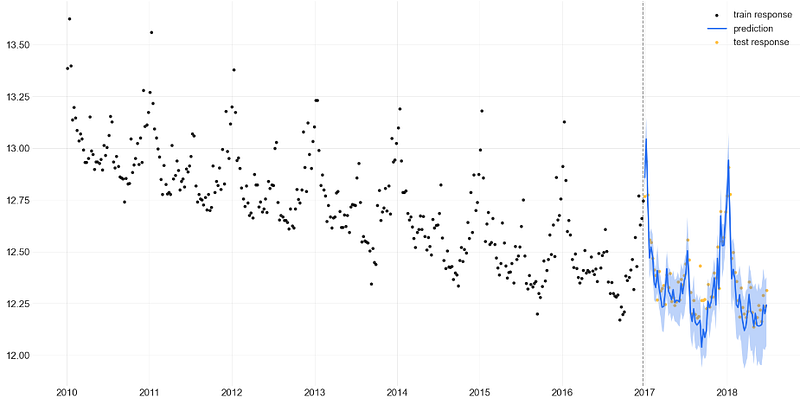

_ = plot_predicted_data(train_df, predicted_df,

date_col=dlt.date_col, actual_col=dlt.response_col)

- Applying the DLT regression to the test set and plotting the result

predicted_df = dlt.predict(df=test_df, decompose=True)

_ = plot_predicted_data(training_actual_df=train_df, predicted_df=predicted_df,

date_col=dlt.date_col, actual_col=dlt.response_col,

test_actual_df=test_df)

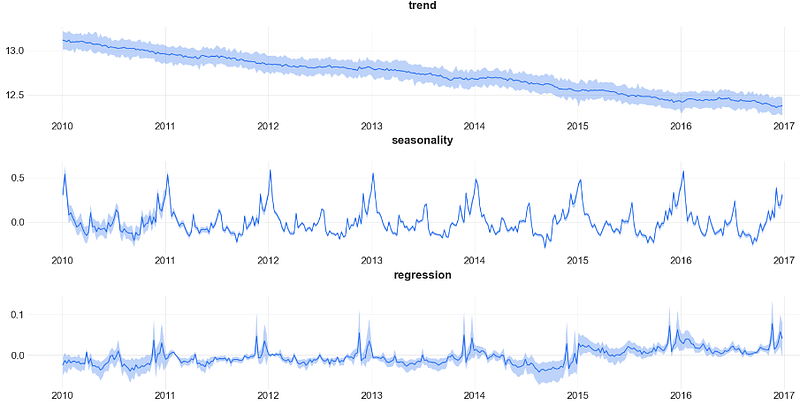

- Plotting the key components vs error of DLT regression applied to the training set

predicted_df = dlt.predict(df=train_df, decompose=True)

_ = plot_predicted_components(predicted_df, date_col)

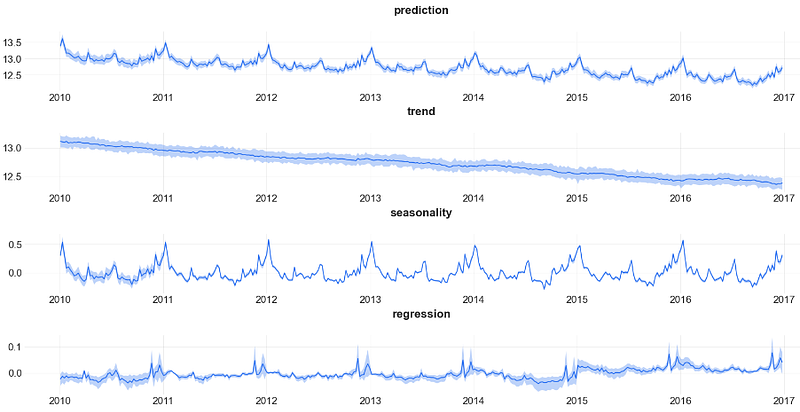

- Adding the training prediction result of DLT regression to the above plot

_ = plot_predicted_components(predicted_df, date_col,

plot_components=['prediction', 'trend', 'seasonality', 'regression'])

Inferences:

- Observe negligible errors of the DLT regression applied to the training set.

- We can see a remarkable similarity between the LGTMAP, LGTFull model predictions and DLT regression (with acceptable 95% confidence intervals) on the test set.

- The DLT decomposition unveils a significant downturn trend and a remarkable 1Y seasonal component.

Conclusions

- Time series forecasting (TSF) is very important because it can be used to make informed decisions in a variety of industries and fields.

- In this post, we have addressed the Bayesian TSF approach based on an assumption about the data’s patterns (prior probability), collecting evidence (e.g., new time series data), and continuously updating that assumption to form a posterior probability distribution.

- Orbit is a general interface for the above approach used to conduct time series inferences and forecasting with structural Bayesian time series models for real-world cases.

- As any other Bayesian TSF techniques, Orbit treats the model parameters as random variables with known prior distributions. Therefore, Orbit can quantify the uncertainty associated with the predictions.

- We have shown that Orbit is the unique tool that allows for easy and accurate statistical modeling while not limiting itself to a small subset of models.

- As with SARIMA and Prophet, Orbit enables the easy decomposition of a KPI time series into trend and seasonality components.

- Overall, our two use cases of TSF have confirmed that Orbit can deliver robust end-to-end forecasting, provide explainability, quantify uncertainty, and perform a fast what-if scenario testing.

References

- Bayesian Time Series Forecasting in Python with Orbit

- Orbit: Probabilistic Forecast with Exponential Smoothing

- Forecasting with Bayesian Statistics in Time Series Analysis

- Hands-On Guide To Orbit: Uber’s Python Framework For Bayesian Forecasting & Inference.

- Bayesian Structural Time Series and ARIMA; why not both?

Explore More

- Stock Time Series Forecasting in a Nutshell: AI/ML Regression/Classification, Statistical Modeling & Cross-Validation QC in Python

- Uber’s Orbit Full Bayesian Time Series Forecasting & Inference

Contacts

Disclaimer

- The following disclaimer clarifies that the information provided in this article is for educational use only and should not be considered financial or investment advice.

- The information provided does not take into account your individual financial situation, objectives, or risk tolerance.

- Any investment decisions or actions you undertake are solely your responsibility.

- You should independently evaluate the suitability of any investment based on your financial objectives, risk tolerance, and investment timeframe.

- It is recommended to seek advice from a certified financial professional who can provide personalized guidance tailored to your specific needs.

- The tools, data, content, and information offered are impersonal and not customized to meet the investment needs of any individual. As such, the tools, data, content, and information are provided solely for informational and educational purposes only.