Execute Algorithmic trades with higher confidence.

How to backtest trading strategies using python feat. MACD

Leverage historical data for backtesting the MACD trading strategy for ANY ticker using Toucan and Python.

- Moving Averages Convergence Divergence (MACD) is a widely used trading signal for detecting trend reversals.

- By design, moving averages lag the underlying time series. As a result, the triggers from trading strategies purely based on Simple Moving Averages are often delayed resulting in missed opportunities or even losses.

- MACD signal overcomes this drawback to some extent. The MACD signal is defined by three components -

1. MACD line: Difference between a slower EWMA and a faster EWMA.

2. Signal Line: EWMA of the MACD Line.

3. MACD histogram: Difference between the MACD line and the Signal Line.

The MACD Crossover Trading Strategy :

- The MACD crossover strategy triggers a buy signal when the MACD line crosses above the MACD signal line.

- On the other hand, an exit/short signal is triggered when the MACD line crosses below the MACD line.

Backtesting the MACD Trading Strategy Using Python:

- In this section, we shall implement a python code to backtest the MACD trading strategy using 3 Steps using Python.

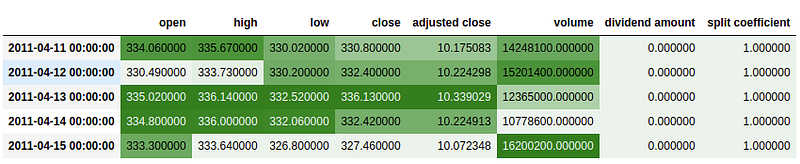

Step 1: Load Data for a Ticker :

- We shall use the Alpha Vantage API for fetching the data for a ticker. I have implemented a lightweight python wrapper, Toucan, for fetching the data using Alpha Vantage.

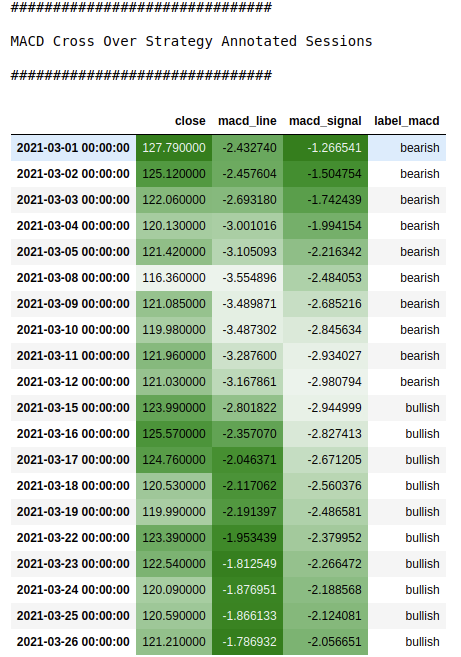

Step 2: Compute and Annotate MACD Crossover sessions

- In this section, we shall compute all the instances when MACD cross-over was triggered for the given scrip.

- It is important to note that the computation includes bullish as well as bearish sessions.

- A long trade is initiated when the MACD line crosses above the MACD signal line. The trade is squared-off when the MACD line crosses below the MACD signal line.

- Similarly, a short trade is initiated when the MACD line crosses below the MACD signal line and the short trade is squared off when the MACD line crosses above the MACD signal line.

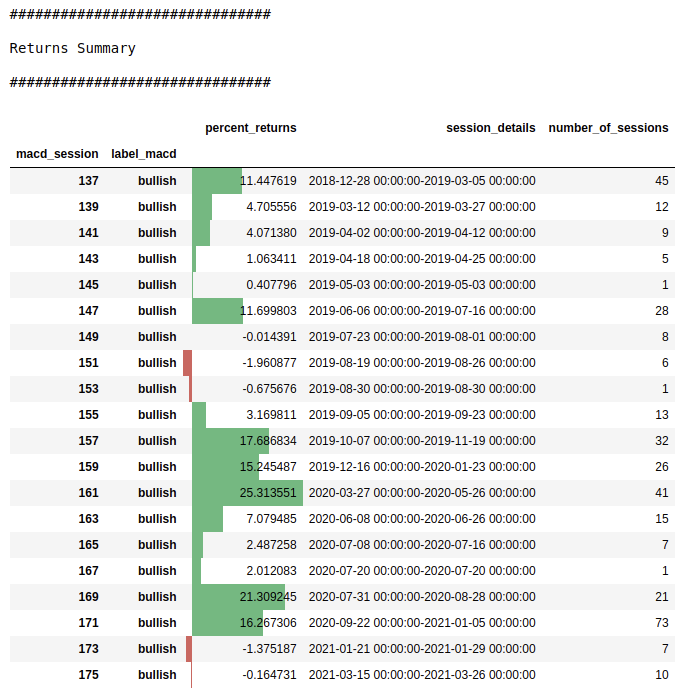

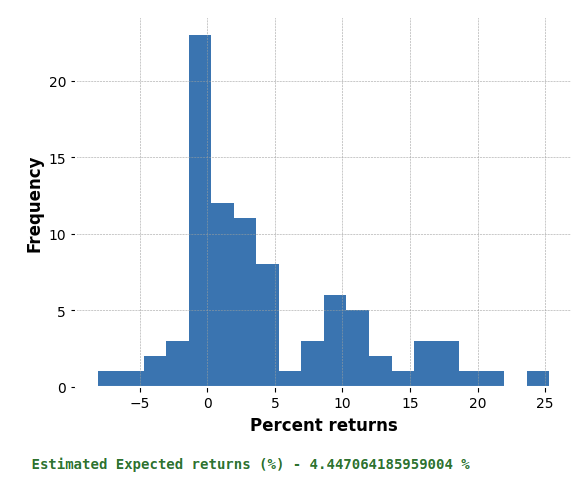

Step 3: Visualize and Analyze the results to make an informed decision:

- It is now time to visualize the results from the backtest. The summary of backtesting results should help us determine how well the MACD cross-over strategy works for AAPL (Apple Inc).

Final Comments:

- Reaping benefits consistently in a volatile market requires a process that is robust, reproducible, and scalable.

- While trading strategies are a good way to automate trades, it is important to backtest them before setting them up.

- The jupyter notebook and source code for backtesting the MACD crossover strategy can be found on my GitHub account.

- If you are wondering how the MACD crossover strategy stacks up against the Moving Averages-based strategy, check out my previous blog that walks through the entire process in-depth.

Let's have a chat :

Comment with your favorite trading strategy or reach out to me on Linkedin to brainstorm ideas.

PS: I would love to collaborate on Toucan and add more features to it. Feel free to get in touch with me if you are interested in collaborating.

Gain Access to Expert View — Subscribe to DDI Intel