A Complete Introduction To Time Series Analysis (with R):: Semi-parametric Models

In the last article, we saw the general strategy to think about any time series model, and how we don’t want either too much or too little dependence in our models. We would now like to explore this more in-depth.

Notation

Just a quick note; remember that

is just a shorthand for

i.e. some time series. Keeping this in mind, let’s dive into the examples.

Semi-Parametric Models

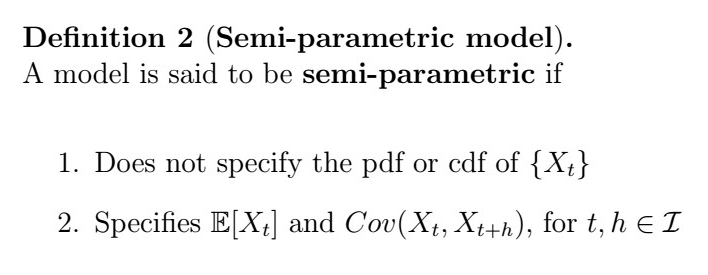

Let’s first take a look at the definition of semi-parametric models

So essentially a model is semi-parametric if we don’t specify its distribution, but we know what it’s expectation and covariance (note the funky h, this is called a lag).

Let’s see some examples!

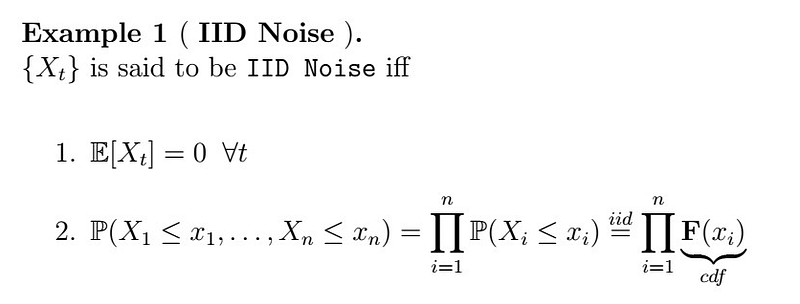

IID Noise

IID stands for “Independent and Identically Distributed”, i.e., each observation does not depend on any other so that by the definition of independence of probability, the joint distribution is just the product of the independent distributions, or in simpler terms, the probability that all of these happen together is no more than the product of their independent probabilities. In addition, we require this process to be mean zero.

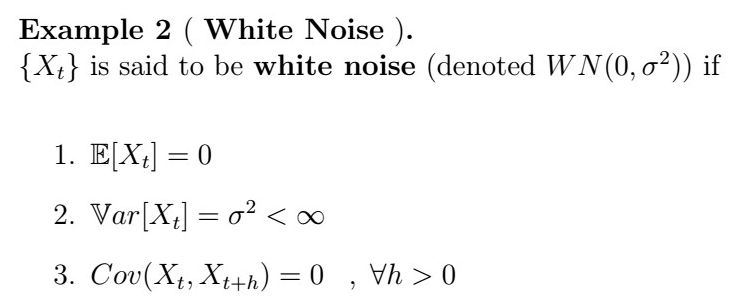

White Noise

Let’s see what these conditions are saying: 1) says that the process has to have a zero-mean or zero-trend, 2) says that the variance of the process is constant, and less than infinity (indeed, imagine what would happen if the variability explodes!), 3) says that the covariance at every lag h is 0; i.e. observations are no longer dependent when being as far as some lag h.

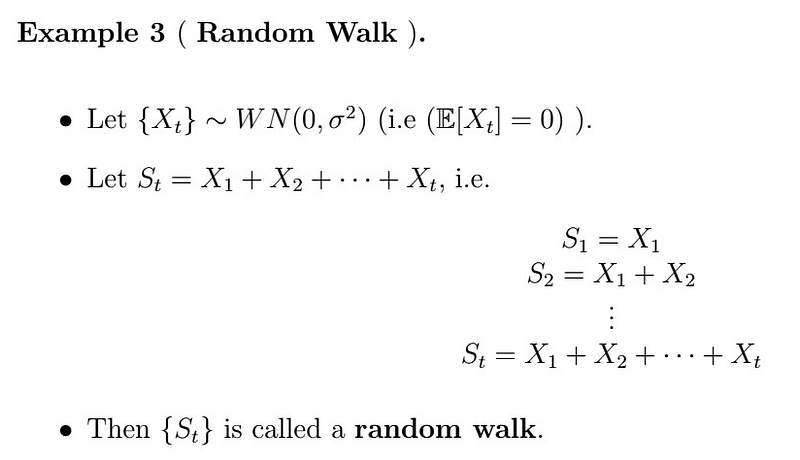

Random Walk

As funny as it may sound, as random walk might not be as random as you would think. This is how it’s done:

- Take some white noise process

- At each step, sample one random variable from the WN sequentially, and add all of these together.

- The result is called a random walk

Here’s an interesting question for you to think:

The answer is no! However, you can verify that this is indeed a mean-zero process.

Next time

That’s it for today! Next time we will take a look at models with structure, the trend, and seasonal decomposition models, and some cool plotting with R. Stay tuned!