90% of Solving a Problem Is Realizing There Is One

6 Obstacles That Stand in Your Way to Financial Independence

On day 3 of the 5 Days to Financial Certainty Challenge I’m hosting this week, we will tackle the obstacles that get in the way of your financial goals.

Most people never achieve financial freedom because of the many obstacles that get in the way of their financial journey. In most cases, they are unaware of the obstacles they face.

And this is a problem.

The first step to solving a problem is realizing there is one.

Obstacles prevent most people from achieving financial freedom. To be clear, there could be millions of obstacles. Some within our control and others outside of our control.

Here, I focus on 6 key financial obstacles that prevent most people from reaching their financial goals.

1. Taxes

“The best things in life are free, but sooner or later the government will find a way to tax them.” — Anonymous

Most Canadians will consider housing costs as their biggest expense.

Unfortunately, they are wrong!

According to a recent report from the Fraser Institute, the average Canadian family spent 43.6 percent of their income on taxes in 2018, more than they spent on housing and other expenses combined.

Can you imagine that? This is significant. The average family’s total tax bill at 44 percent is double the amount they’re paying on housing costs each year.

So, if tax is our biggest expense, why is it that most people don’t pay attention to it? Why is it that most Canadians and the news media get it all wrong?

There are two main reasons for this.

First, the majority of taxpayers are used to withholding taxes. They never see a good part of their money as their employers take it upfront from their salaries and remit to the government.

Second, other forms of taxes you pay on everyday purchases seem insignificant on a transaction by transaction basis.

The total tax bill considered in the Fraser report reflects taxes families paid to the federal, provincial and local governments — including income, payroll, sales, property, carbon, health, fuel and alcohol taxes.

So, there is no doubt that tax is a big obstacle to achieving financial independence.

To be clear, paying taxes is important for the benefits it provides to our society as a whole. What you have to consider is whether you’re paying more than your fair share of taxes.

While I highly recommend that you pay whatever taxes you are legally required to pay, you should consider legal options available in our Tax Act to reduce your tax burden.

So, what can you do about this?

- Start by educating yourself. I share a lot of articles on how you can get started. Some of these include 10 Reasons Why You Pay Too Much In Personal Taxes; Which is Better — Tax Credit or Tax Deduction?; 10 Mistakes the Do-it-yourself Taxpayers Make When Filing Their Tax Returns; Know Your Marginal Tax Rate and Save on Taxes; and many more.

- Seek advice from a professional to help you plan on how you can optimize your taxes.

2. Non-Deductible Interest

“Tax laws favor capital over labor, giving capital gains a lower rate than ordinary income. The rich get humongous mortgage interest deductions while renters get no deduction at all.” — Robert Reich

The biggest asset we own is our primary residence for those that own their own homes. The cost of buying a home continues to rise, and it is getting increasingly unaffordable for most young people today.

As the cost of housing rises, so is our mortgage balance. Added to this is the rising debt of the Canadian household. As a result of all these high debt balances, most Canadians are now burdened with high-interest costs associated with these debts.

Unfortunately, in Canada, our tax rules generally do not permit a deduction for the mortgage interest related to our primary residence.

Furthermore, most interest on other debt we have is also not deductible for tax purposes except the debt that is incurred directly to earn income from a property or business.

Most of us never put a lot of thought on this as we automatically pay our mortgage each month or every two weeks without examining how much of this payment goes towards the reduction of our principal balance.

The fact that you cannot deduct your biggest interest cost is a huge obstacle that will prevent you from achieving your financial goals.

So, what can you do about this?

- I encourage you to start by looking at your mortgage statement or your amortization schedule and see the amount of payment that goes towards interest payment alone. You will quickly notice that it is significant.

- Consider strategies to convert some of these non-deductible interest costs to tax-deductible interest costs. An example is renting part of your home so you can deduct part of the mortgage interest for tax purposes.

- In certain circumstances, taxpayers can obtain an interest deduction for borrowings made for specific purposes. The general rule of thumb is that interest is deductible to the extent the borrowed monies are used to earn income. Consider strategies that will allow you to pay down your mortgage, then borrow the funds as home line equity to invest in an appreciating asset.

3. Endless Desires/Lifestyle Inflation

Endless desire thrives on the myth that “more is better”. As a result, most people buy more and more things that they don’t necessarily need. They buy new clothes for every event, they get a bigger and better house every time they can afford it. And they upgrade every area of their lives.

This eventually leads to lifestyle inflation.

We are all familiar with the term “Inflation”.

Inflation is the rate at which the general level of prices for goods and services is rising. I wrote on this earlier and you can read it here.

Lifestyle inflation happens when your household spending rises to match your rising income. In other words, your lifestyle expands to match the extra income from your paycheck.

Often times, it happens without you noticing it. It sneaks up on you. A little raise here, a bonus there, and pretty soon your expenses get out of control.

It’s so easy to get caught up in lifestyle inflation. After all, you’ve worked hard to earn the extra income and you deserve to reward yourself with a bigger home, nicer car, designer clothes, and luxury vacation.

The challenge is if you’re spending all the extra money you’re making, it’s nearly impossible to save. If you can’t save, you can’t invest and if you can’t invest, you can hardly get ahead.

Lifestyle inflation is certainly one of the reasons why most Canadians live paycheck to paycheck. With many people choosing to keep up appearances rather than stash money away for a rainy day, it’s easy to see how.

So, what can you do about this?

- Resist the pressure to keep up with the Joneses. A lot of our money life is also about how we show up in society. So, there is always enormous pressure to be like the neighbor next door even though we know nothing about this neighbor. The fact that your friend’s daughter is playing soccer, basketball, and taking music classes doesn’t mean your daughter needs to do it too. You’re still a good parent if your child’s only extracurricular activity is swim lessons at the community pool.

- Don’t take on new debt because you can “afford” it. This is particularly important when it comes to non-tax-deductible consumer debt. Very often, as soon as we get a raise, we can afford to upgrade our home, buy a new car, or new furniture all on debt. With the extra income, we can justify making the extra payment on the new debt. Just because you can “afford” the monthly payment on something does not mean you can truly afford to buy it. The interest alone could make you pay far more than the original price.

- Know your GAP and live on a budget. I wrote about the GAP in an earlier article. You can read it here. GAP is what is left of your income after you pay your expenses and taxes. To avoid lifestyle inflation, you need to obsess about your GAP. If you do this, you will automatically pay attention to all the variables that make up the GAP — your income, your expenses, and your taxes. Your goal is to keep your GAP positive and high. You do this by living within your means.

4. Living in Denial

“Most men would rather deny a hard truth than face it.” — George R. R. Martin

When it comes to your finances, there is often shame you have to deal with, particularly with your poor financial decisions. As a result…

You avoid talking about the financial issues you have.

You use other people’s behaviors as evidence that you don’t have any financial issues.

You deny a problem absolutely when confronted.

You rationalize your uncontrollable spending.

And you ignore the advice and concern of loved ones.

By failing to realize there’s a problem, you cannot fix it and you hinder your chances of achieving financial freedom.

So, what can you do about this?

- You must confront your financial issues by recognizing the problems and admitting your failures. In addition, you must also see what could hinder your move toward financial fitness.

- Remember, 90% of solving a problem is realizing there is one.

- Once you admit your money issues, focused intensity is required for you to reset your money-spending patterns to set yourself up for success.

5. Employee Mentality

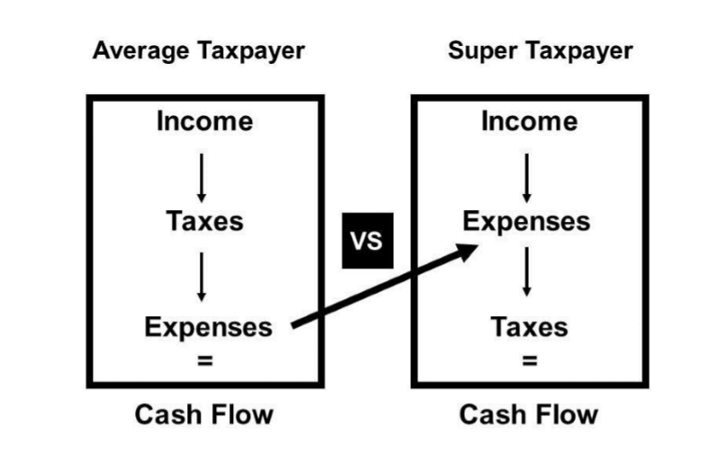

Have you wondered why you have very little or no money left shortly after your payday?

Are you one of those high-income earners that make over $100,000 per annum and still wonder, where is all my money?

The clue may be in the diagram below:

For the average Canadian employee, taxes are taken upfront through payroll withholdings before they see the money.

With the funds left, they pay their expenses, the majority of which are non-deductible for tax purposes. Payments like mortgages or rent, car payments, childcare expenses, gas, food, clothing, and other household expenses deplete your cash.

At the end of the day, you have little or no cash to invest.

By staying trapped in the employee mindset, you don’t consider opportunities provided by owning a side business to reverse-engineer the cash flow pattern so that there is more cash left over to invest and grow your wealth.

So, what can you do about this?

- Consider obtaining tax planning advice that will enable you to make changes to your lifestyle so you can save more of your cash to grow and accelerate your wealth.

- Contact your employer to reduce the amount of upfront deductions from your salary.

- Develop a business mindset so you can convert some of the after-tax expenses to before-tax expenses and also convert some of your non-deductible interest costs to tax-deductible interest costs.

6. Inflation

“Inflation is like sin; every government denounces it and every government practices it.” — Frederick Leith-Ross

What is inflation?

Inflation is the rate at which the general level of prices for goods and services is rising.

I refer to this as the silent killer as we often don’t see it.

While most Canadians are familiar with inflation, we often underestimate the powerful impact it has on our ability to grow our wealth and eventually achieve financial freedom. Ironically, we often think of financial freedom in terms of dollar value rather than in terms of the purchasing power of our dollars (the amount of goods and services you can buy).

At the end of the day, if you’re unable to acquire what you need when you need it, then you’re not necessarily financially free.

I discuss inflation in detail in the article “The Silent Killer — Inflation”. I encourage you to read this for a deeper understanding of the devastating impact of inflation.

Inflation will rob you. It will reduce your purchasing power. And it will kill you financially if you don’t pay attention.

So, what can you do about this?

- Invest in real estate — it is a great hedge for inflation.

- Invest in precious metals like gold and silver — history suggests that these metals hold their values when everything else crumbles.

- Invest in yourself — arm yourself with the knowledge that no one can take away.

In Conclusion

You now have a better understanding of what may be holding you back from achieving financial freedom.

You are now aware of the major obstacles.

In my book, Tax-Efficient Wealth, I go into some details on how you can tackle these obstacles in a tax-efficient manner.

P.S. It’s not late to join the FREE training I’m providing this week. You can watch the replays for the sessions you missed. This week, I’m sharing all I’ve learned about personal finance. I will show you how you can move from a place of uncertainty in a time such as this to a place of confidence and certainty with your finances.

This is a different learning experience as you will have the opportunity to ask questions, work on implementing what you learn each day, and actually get some great results at the end of the week.

Also, I will give you my brand new book, TAX-EFFICIENT WEALTH as a thank you for joining.

Join the Challenge here and get a FREE eBook version of my new book!