Know Your Marginal Tax Rate and Save On Taxes

Did you know that you could plan your affairs to save on taxes if you know your marginal tax rate?

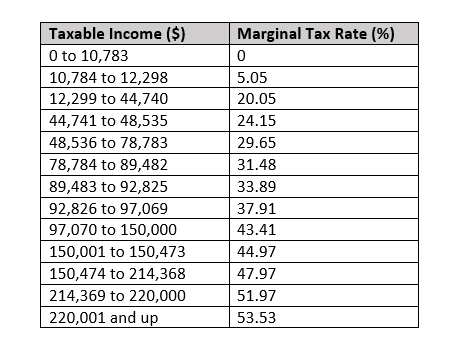

The Canadian tax system is based on marginal tax rates. This simply means that the more money you make, the more taxes you pay. As your income increases, so does your marginal tax rate. Marginal tax is the dollar amount of tax you pay on any additional dollar of taxable income. Let me illustrate this with a simple example for an individual tax payer residing in Ontario earning regular income. In Ontario, below is the 2020 marginal tax rates (Combined Ontario and Federal Tax Rates):

Based on these rates, if you live in Ontario and earn $50,000 of employment income, you would be in the 29.65% marginal tax bracket and you would pay 29.65% in taxes for every dollar you earn above $48,535. If you earn $100,000 of employment income, you would be in the 43.41% marginal tax bracket and you would pay 43.41% in taxes for every dollar you earn above $97,070.

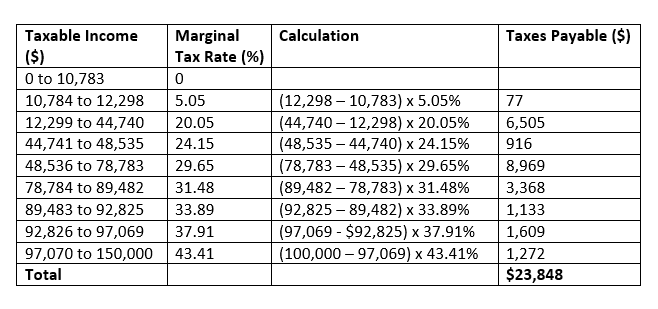

Most people often misunderstand marginal tax rates by thinking that your marginal tax rate will be applied to your entire income to determine your total taxes. For example, you may think that if you earn $100,000 in regular income, your taxes payable will be $43,410 because you’re in the 43.41% marginal tax rate. This is incorrect, and it is a general misconception. Rather, if you earn $100,000 of income, your taxable income will be $23,848 calculated as shown in the table below:

Knowing your marginal tax rate is critical for tax planning and other financial decisions. Without this knowledge, you may end up paying more than your fair share of taxes and keeping less of your income. Remember, wealth accelerates based on how much you can keep, not necessarily how much you make in gross earnings. Understanding marginal taxes will play a key role in building and accelerating the growth of your wealth.

In the example above, with adequate planning it is possible to avoid the additional $1,272 in taxes by keeping your income below $97,070 in the tax year. You could even save more taxes if you plan properly and keep your taxable income below $92,826. You may wonder, what can I do to keep my taxable income below a certain threshold? It’s all about changing your situation. If you change you situation, you will change your taxes…this is a topic for another day.

So, take a look at your most recent tax return and determine what your marginal tax rate is and start thinking of ways you can keep your income below that marginal tax rate a year from now. Remember, every dollar saved in taxes will help accelerate your wealth.