9 Habits of A Poor Person

Get woke or go broke

Remember the shock of opening up your bank account page only to see you have less money than you thought?

Remember the feeling of crushing hopelessness that immediately followed the realization of how hard you worked, but you have less money than when you started?

Have you ever felt like you were on the sidelines watching everyone else rake in the money?

Do you get the Sunday-blues just thinking about another work week?

I put together this list of habits proven to covertly destroy someone’s bank account and unknowingly keep them exactly where they are for decades to come.

Let’s explore some of the very things that could be taking a massive toll on your finances.

Here is a list of small ways you can begin building side hustles and incomes. Feel free to come back to this list after checking out this article.

1. Gambling

Who hasn’t had a run-in with some sort of gambling?

Even as a child playing pretend poker with my friends and fake currency, I felt that rush. The rush of taking a massive chance. The rush of knowing I’m either leaving with nothing or leaving with everything.

According to Debt.com, about 23 million Americans go into debt due to gambling, with the average gambling loss being nearly $55,000.

Gamblers will most-likely take out loans or borrow money, in general, to pay off their losses, but in turn, are now slaves to debt. Debt can wrack up a high monthly payment, which in turn can absolutely rob an individual of savings, investment money, and retirement money.

2. Impulse Purchases

No one is immune from that “holy crap, look at this!” Feeling when walking through a store. Everyone on a whim makes purchases, but do they like their purchases down the road?

Can you think of more than one time you bought something on an impulse and regretted it less than a whole 24 hours later?

Did you know that impulse-spenders are the exact individuals that companies spend millions of dollars to study and target with their marketing?

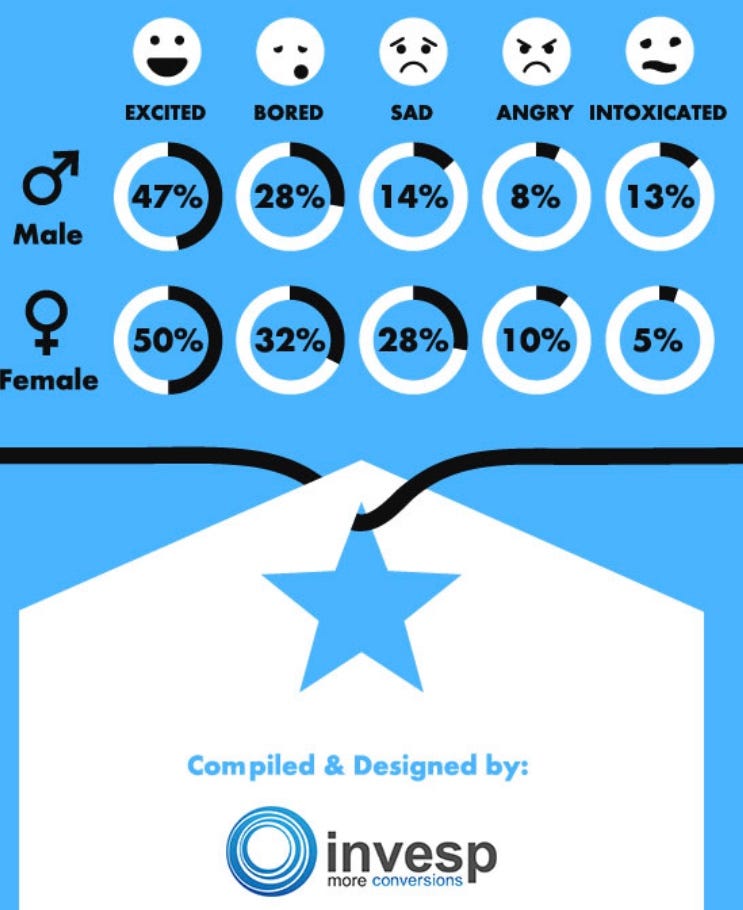

According to Invespcro.com, 84% of all shoppers make impulse purchases on a regular frequency. Over 54% of people who make impulse purchases also spend over $100.

20% of impulse shoppers make a sudden purchase of over $1,000. Statistically, you can reduce your chances of impulse buying on average by 13% by simply planning out your shopping trip.

- Men regret their impulse buys 46% of the time.

- Women regret their impulse buys 52% of the time.

3. Waiting For Miracles

Sometimes hopelessness can breed an extreme response to fixing the problem of having no money. This can appear like waiting for the universe to send some cash your way in ways that are so profound and downright miraculous. What is the problem with that, though?

It looks like foolish investing. As a victim of my own foolish investing, I felt this one personally. If you are hit with sudden expenses and feel as though your life is falling apart, you turn to desperation.

This could take the form of throwing everything you have into a stock you didn’t research in hopes it will explode and make you a vast sum.

It also comes out in the form of buying into the lottery.

According to Vox.com, here are some facts about the Lottery system:

- Most lottery tickets are sold in poor neighborhoods. People who make less than $10,000 a hear spend almost $600 (6% of their year’s income) hoping to win the lottery.

- Statistically, the lottery preys upon areas where minorities tend to congregate. Nationally, African Americans spend nearly five times more on lottery tickets than white people.

- Most money that enters the lottery system is through quick picks and scratch off tickets. Both of which lead to addictions to gambling and lottery playing.

- A majority of people living in poverty or have money trouble think that betting and lottery winnings are the only way to gain wealth.

Chasing the miraculous will statistically leave you with less money, more debt, and probably an addiction on some level.

4. Avoiding Debt

Going into debt seems like a common theme in the United States. You accumulate debt by purchasing new cars, a new house, going to college, etc.

While these things can be good to acquire, they come at a massive price.

According to Lendingtree.com, the average total debt payments per month for a single household is around $1,200 a month.

Next time you are tempted to buy a fancy car, ask yourself if it is worth the monthly payment. You can combat this debt by sticking to what you can afford and buying with cash instead of credit.

For example: if you make $3,000 a month, you cannot afford to take a mortgage out on a house that is worth $400,000 no matter what the bank tells you.

The first car I bought was a 2000 Toyota Camry, and I bought it for $2,000, which meant I didn’t pay anything at the end of the month to own it.

The first house I bought was a little small and was only listed for $120,000. My wife and I together made around $75,000 a year at the time. Our monthly payments started at $748, which was only $23 higher than what we paid at our apartment.

Do not buy what you cannot afford with cash. Debt will enslave you to monthly payments and ensure you never get ahead.

5. Never Follows A Budget

To some, the word “budget” is a haunting word. It conjures up thoughts of mindlessly plugging away on the calculator and doing math into the late hours of the night. In reality, even having a small grasp on your expenses and incomes could entirely change your life, literally.

The majority of people think it is easy to track their budget without looking because they have one source of income, and they know exactly what they get paid. However, most people have no clue what their total expenses were in a given month.

According to Debt.com, the average American spends less than 4.5 hours a year figuring out and looking at their own budget. Here are a few other statistics from Debt.com:

- Only 30% of Americans have a long-term financial plan that includes savings and investment goals.

- You’re most likely to budget if you make at least $75,000 per year.

It is easy to rattle your largest expenses of the month off the top of your head, but most people get slaughtered by the small expenses you forget about. It might be scary to think about, but you probably aren’t aware of all of the wasteful spending taking place. You are most-likely letting money slip through your fingers.

Action Step: Sit down and track how much money your household brings in first. Then for a month, track every dollar you spend. This will give you an accurate depiction of your yearly spending habits. As I write this, I am reminded that when I did this, I was shocked to find out that almost 30% of my income was going to gas station food and coffee.

6. Has No Financial Plan

Do you have a financial plan? Have you ever thought about what that would look like? Most people put minimal thought and energy into their money yet still expect financial miracles and then complain when they don't have any money.

Without something to work for, you may as well never make progress in anything. This is why it is important to have a plan.

Now by “plan,” we are not talking about, “I want to be a millionaire, that is my plan.” No, instead, we are talking about setting small, reachable goals.

When my wife and I had to pay back our $27,000 in college loans, we had to set smaller goals to stay motivated. Instead of saying, “our goal is to pay off $27,000,” we said, “our first goal is to get this loan down to $25,00”.

Every $2k-$3k became our next goal, and so we were always within arms reach of our desire, and before we knew it, the loan was completely paid off. What is your goal?

Here is a list of potential milestone goal examples to help come up with your own plan:

- Increase savings account by $500

- Pay $1,000 off of my current debt.

- Invest $500 more into stocks

- Earn my first $10 on Medium

You need to formulate small goals to maintain your motivation, or else you will fizzle out. Imagine if my wife and I had kept the “pay off $27,000” goal. Every time we would have put an extra $300 into the loan, it would have felt inconsequential and as if it was simply a drop in the bucket.

Action Step: based on your own financial situation, come up with a small goal that is reasonable and able to be accomplished through a little added effort.

7. Continually Has Credit Card Balances

Your credit card is not free money. Credit cards are built to provide a service that attempts to secretly rob you in the end.

According to Nerdwallet.com, credit card companies earn their money on the interest that card users accumulate and card users that miss their payments. Every time you use your credit card, the company is praying that you mess up the payments.

Not surprisingly, the lender companies that specialize in card users with bad credit earn more money. Your credit card company is not your friend, no matter what they try to convince you of.

Here is how these companies make their money on individuals with bad credit:

- They will charge annual fees.

- The company charges a small percentage for those individuals who get cash from an ATM.

- If you transfer your card debts to another card to acquire a lower interest rate, you will be charged a small percentage.

- The company will charge you if you fail to make a payment date on-time. This will also result in your credit score dropping.

Do not play games with your credit card company. They have designed the system to suck as much money out of your pockets as possible without you even thinking about it.

8. Does Not Save For Emergencies

Did you know that the average American either is not or cannot afford to save up even $400 for an emergency fund each month, according to Financialsamurai.com?

For some, that may seem like a lot of money understandably, but according to Healthcostinstitute.org, the average emergency room visit in the United States is roughly $1,389.

It is absolute of the utmost importance that you start growing an emergency fund because you never know when you will need it. No one knows when emergencies will pop up, and so you need to be prepared at all times.

If you cannot afford to cover your car breaking down, your plumbing going down the tubes, or a trip to the hospital, then you are far more prone to take a loan to cover the expenses. Here we go again. You will more than likely incur some sort of debt if you are not prepared.

9. “Get Rich Quick” Schemes

Last but not least, if you set your heart on getting rich quickly, you will ultimately come out poorer on the other side than when you started. Pyramid schemes and Multi-level Marketing are designed to prey upon the poor while also empowering them to keep pumping money into the system.

A real-life example that personally impacted me early on in college came through a pyramid scheme group called Wake Up Now.

I had never heard of a pyramid scheme before, and I was enthralled with the prospect of earning passive income. All I had to do was pay $100 a month to buy into the system. Then I had to get others to sign up under my team, and I would then make $600 a month, and it would just scale exponentially after that.

I lost $800 and had to freeze my account later when I realized I couldn’t stop payments to the group. After a few years, the group disbanded, and a vast majority of everyone in the group lost a lot of money.

The truth is there is no way to make money quickly with little to no effort.

Here are some key indicators that you are in a pyramid scheme:

- They do not sell a product.

- There is a monthly membership fee.

- You have to get others to sign up to start making money.

- Your team layout literally looks like a pyramid.

- Those on your team are also tasked with getting people under them on the bracket.

If you are in such a group, RUN FAST!

Summary

All of these money pits can be avoided with just a little effort and some knowledge. By setting small goals and knowing how you want to accomplish them through creative working and budgeting, you don’t have to be another poverty statistic.

Get woke, or go broke.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.