5 Charts show Developed economies are outpacing the Emerging markets

After more than two decades of robust growth, the developing countries are showing signs of economic stagnation

As the Central banks around the World scramble to lower the interest rates to mitigate the risks of a global slowdown emerging from the on-going trade war between the United States & China, this looming threat to globalization is an even bigger worry for developing countries or so-called emerging markets.

Last week, The U.S Federal Reserve cut the benchmark interest rate for the first time in a decade citing growth concerns. Following the lead, RBNZ (Central bank of New Zeland) surprised the markets with a 50 basis point cut followed by India & Thailand which dropped their interest rates by 35 & 25 basis points respectively.

For two decades ever since its inception in 1988, the MSCI Emerging Markets (EM) equities index outperformed the U.S benchmark S&P index and other in the developed world by a wide margin. Ever since the global financial crisis of 2008, emerging markets stocks have lagged or even stagnated, while US stocks have shown consistent growth doubling their gains.

The rapid growth in these developing economies lifted millions of people out of poverty creating bigger middle classes with greater purchasing power. This created opportunities for domestic & foreign companies for investment in finance, technology & infrastructure which kept the growth momentum going in these countries. This also created an important role of emerging markets in the diversified portfolio of international investors.

The situation has changed drastically for Emerging economies with weak commodity prices, disruption in the global supply chain by the trade dispute and tight monetary conditions. Add controversial departures of two senior Economic policy officials recently — one in Turkey & another one in Mexico and these EM don’t look so attractive after all. Let’s back up this hypothesis with some figures.

Developed economies have grown at a faster rate in recent years. The globalization that kicked off in the early 1990s resulted in an increase in cross border trade, coupled with a commodity supercycle and rise of global supply chains driving the developing countries towards the path of convergence with the developed world. For many investors emerging markets became an essential part of their portfolios.

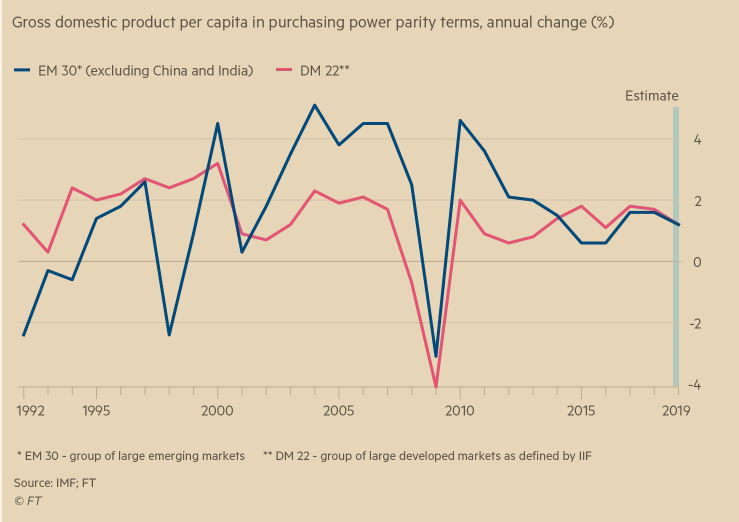

Looking at the GDP comparison of the EM 30 & DM 22 (Figure 1) shows you a vivid picture for the past 27 years. EM 30 outpaced the DM 22 initially, with a sharp drop coming in 1997 due to the Asian Currency crisis. Things picked up again & peaked in 2000, just before the dot com bubble which caused a fall in both regions.

There was sustained growth in both regions for the next 8 years with EM 30 growing at double the rate of the developed economies. The financial crisis of 2008 saw the biggest fall in growth rates for both regions before recovering to pre-crisis levels in 2010. It took almost 14 years for developed economies to overtake the emerging markets growth rate in 2015, and have maintained an edge with the convergence happening recently in 2019.

The emerging markets have become a disparate group. It is not an asset class where a crisis in one of the countries had a huge contagion effect on the others as well. Fiscal & monetary reforms by individual countries have changed the dynamics of this group in such a way that some investors even question the logic of calling them “emerging markets” anymore.

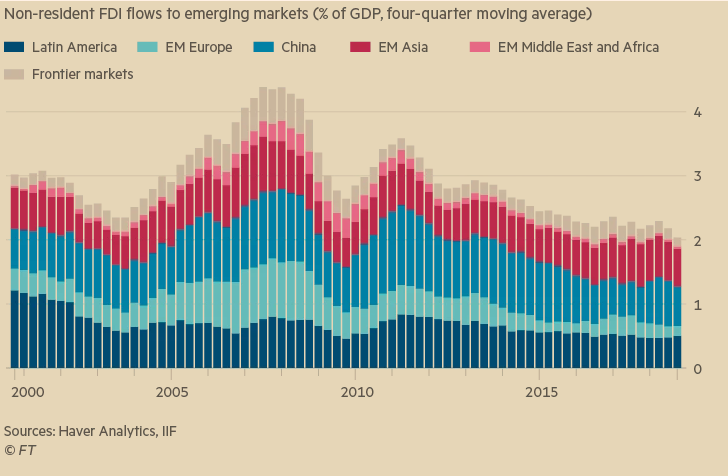

An example of this is how Argentina & Turkey got hit the worst last year with the rising US dollar, while others got away relatively unscathed. Similarly, a shift from China has helped economies like Vietnam to prosper offering an alternative to cheap labor & products. Looking at the varied FDI (Foreign direct investment) data (Figure 2), different regions are showing varied capital flows based on the financial conditions of that particular region or country. The general trend, however, seems to be on the downside.

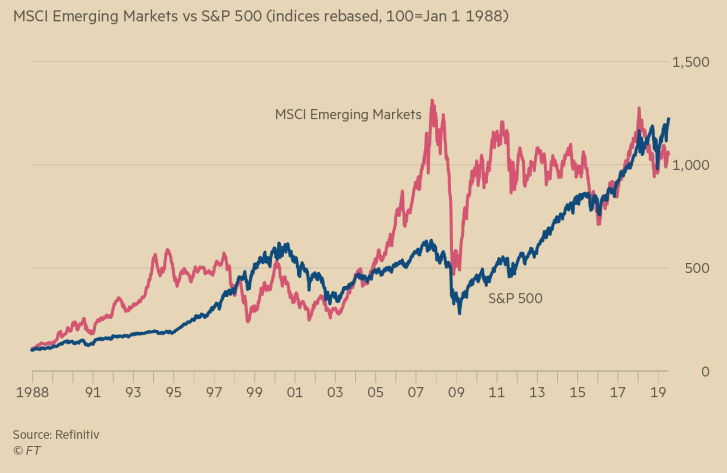

Equities confirm the hypothesis that money has been flowing into the developed world markets since 2015 as shown by the comparison between the MSCI emerging markets index against the benchmark U.S index S&P 500 (Figure 3). After the MSCI index led the American market for the decade between 2005–2015, it has finally tracked below the S&P as the longest bull run in the U.S continues. While the MSCI index is at a comparable level to S&P, they are beginning to show signs of divergence.

In terms of Productivity, emerging markets have been more than disappointing where they could barely match the levels of the developed economies (Figure 4). The anomaly in this comparison is China which gained from the technology transfers it received after joining the World Trade Organization (WTO) in 2001. Despite the growing populations in many of these developing economies, the investment has lagged raising a red flag for future growth prospects.

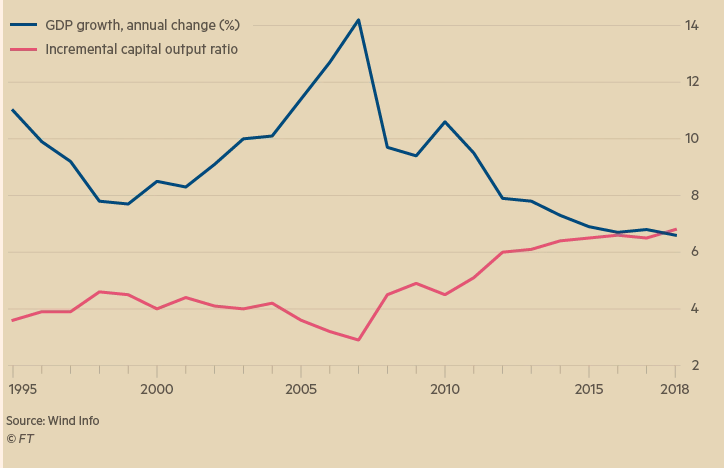

Another warning sign for emerging markets is the economic slowdown in China, which has been a growth model for not just the region but for the whole world. The power of credit to drive growth in China has declined significantly (Figure 5) — capital needed to produce each additional unit of Chinese output has increased by more than two-thirds since the early 2000s.

Simply pumping more money into markets is not producing the desired results. The trade war with the U.S and a strong dollar are not helping the cause of investors who are looking to borrow credit to invest. This uncertainty has added to the challenges of the emerging markets who are already struggling with changing financial conditions.

According to the Institute of International Finance (IIF), total corporate debt in emerging markets (excluding the financial sector) has jumped to 93% of GDP at the end of March from 60% two decades ago. In developed markets, the same was equal to 91% of GDP.

This borrowed money was mostly spent on services & consumption over the years, rather than paying down previous debts or on productive investment, which has become the primary reason for the financial problems they find themselves in today.