Understand Core Systems in Digital Banking Architecture

Digital Banking’s Achilles Heel: Navigating the Complexities of Core System Transformation; #14 in the Digital Banking and Fintech series

Table of contents:

· Intro · What are core systems? · Are our core systems capable of handling digital banking challenges? · How to make changes in core systems? ∘ 1. Identifying all impacts of a proposed change: ∘ 2. Coordinating the change: ∘ 3. Testing the change: · Summary · Resources

Intro

They power banks worldwide, processing millions of transactions and hosting millions of consumer accounts. They make all banks run smoothly.

What am I talking about?… Core systems. When it comes to banking, they’re mandatory.

What are core systems?

Core systems or core banking systems are a back-end system that enables the processing of banking transactions and holds the account ledger for products that customers hold with a bank.

Whether they are transaction products, savings products, credit products, or more exotic products like derivatives, they typically include transaction processing. Core systems have an accounting capability, and the ability to host and support functionality that allows accounts to execute payments and calculate fees and charges.

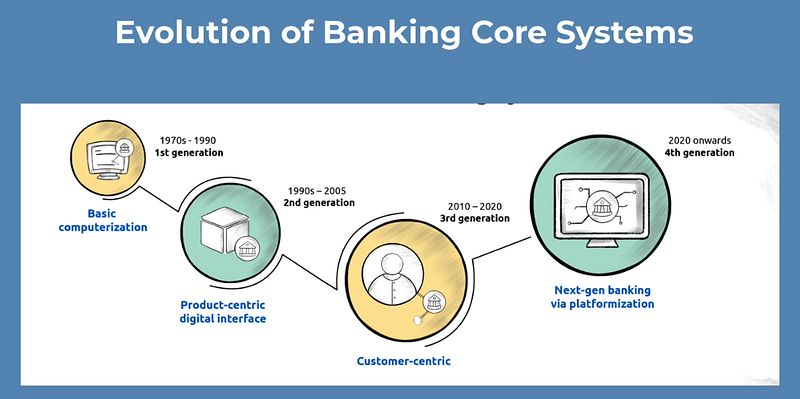

To the surprise of non-bankers, many banks employ the 1970s and 1980s mainframe core banking systems.

Core system operation isn’t affordable. Banks spend millions annually maintaining their core systems, which frequently interface with hundreds of other systems.

Core banking systems handle a large volume of transactions and are supposed to perform continuously. Given the importance of the services they provide to keep a bank running.

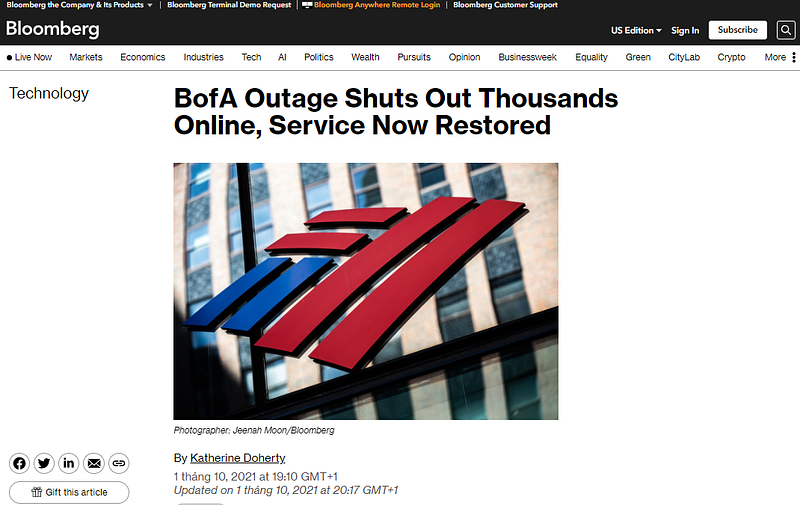

Outages do occur, regrettably, and are frequently met with negative feedback from customers. There is negative media coverage, and it frequently catches the attention of regulators.

Maintaining core systems is crucial. The subject arises frequently for bank executives as digital banking grows.

Are our core systems capable of handling digital banking challenges?

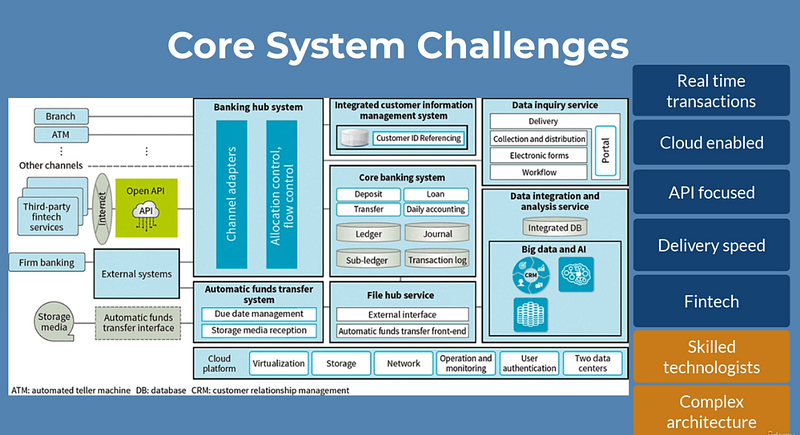

Those problems include real-time transaction processing, not batch or overnight. This is common in banking as the ability to host data and systems on the cloud and use more APIs.

Additionally, client demands are higher today. Digital banking teams must release new digital banking features often, sometimes monthly if not weekly, via mobile, online, and other media. In this digital age, core systems must interface with fintech.

Core systems were intended for a different paradigm, thus managing these constraints might be difficult.

Moreover, banks face daily practical issues like skill, technology, and human resources, who know and have experience with specific core systems, and spaghetti trees of code that are often poorly documented, which means that changes to any part of a core banking solution can have unknown consequences elsewhere in the stack.

However, one of the most difficult difficulties I’ve encountered with core systems is the capacity to make changes.

In digital banking, change is rapid. Customers demand quick product and digital banking experience development. Other fintechs and banks adopt this as their norm.

If it takes months to ship a digital banking experience that a rival can ship in weeks, you’re at a disadvantage.

“Getting changes made to core systems, particularly older — legacy type systems, is a long and complex process.”

However, this issue is not limited to the digital banking experience. Creating excellent customer experiences in mobile web wearables and chat is not that difficult. It takes a clear vision, excellent talent, motivation, and a well-defined product roadmap overseen by experienced product leaders.

How to make changes in core systems?

Making changes in core systems is hard work, the process may include:

1. Identifying all impacts of a proposed change:

Complex core systems may have hundreds of impacts and touchpoints.

2. Coordinating the change:

Working with many teams that maintain distinct sections of a core system makes prioritising and coordinating updates concurrently difficult.

3. Testing the change:

From my experience, this is one of the most difficult issues. Testing a change that involves many touchpoints in core systems is not just complicated; it also necessitates substantial work to create suitable test environments to adequately test these types of changes.

And don’t get me started on what it takes to generate test data. I’ve seen it take months and months to generate the necessary test data to validate what is typically a minor modification. This includes ensuring that the existing core infrastructure and digital banking are not broken.

Making modifications to core systems can take months, sometimes even a year, making it difficult to coordinate all the necessary adjustments and deliver a digital banking experience.

From my experience, it can feel like ascending a mountain and be stressful. Working in digital transformation has its ironies.

Customers think a mobile app feature or product took weeks to construct. Thus the work behind the scenes to update core systems has taken months, sometimes years.

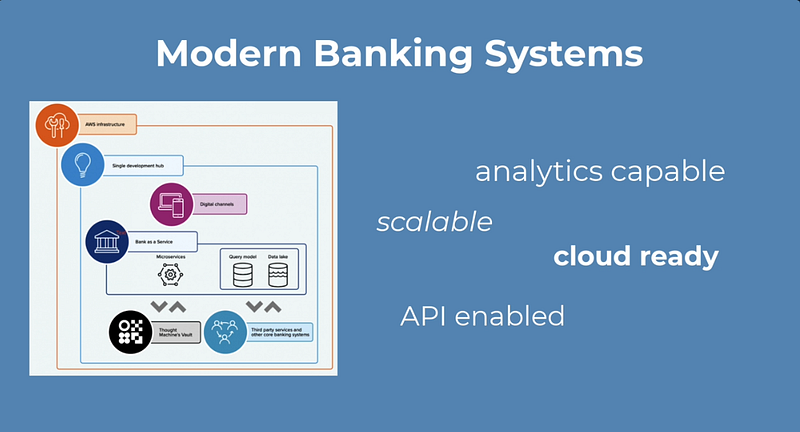

However, new core banking systems have arisen to address this complexity and change difficulty. Their cloud-ready, open-banking-compliant solutions are easily scalable and enable speedier transformation. So, they’re digital banking ready.

I’m not criticising legacy core systems, they excel. However, they were designed for a time when changes were little and individuals wanted stability and scalability as their consumer base grew. Digital banking requires faster change more often with less complexity and risk, yet 40-year-old core systems aren’t ready for that.

That does not mean that banks are lined up to replace their core systems. 99% of banks are risk-averse, and executives begin to twitch when these three words are mentioned: Core system replacement.

Due to unknowns, banks are reluctant to decommission core systems because they’re so interwoven and embedded. I don’t think they have much of a choice because digital banking is pushing the need for additional functionality, products, and procedures leveraging APIs, AI, and big data at reduced cost. That could compel many executives to face the unthinkable: change their beloved core systems.

Summary

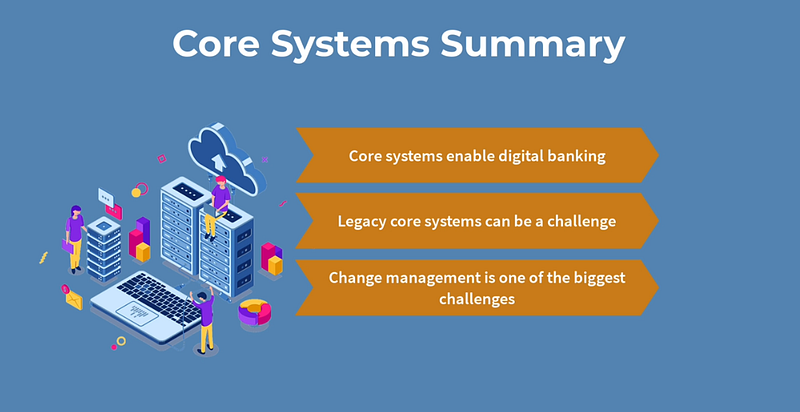

In summary, core systems support digital banking. They handle banking, including transaction processing, accounting, and integration with many bank systems.

Although they facilitate digital banking delivery, they can also slow it down. This can frustrate clients and the folks who provide digital banking services. They are motivated to make customer value delivery a reality in digital banking, but this can be hampered by the slow pace of delivery in core systems.

Keep track of the reference resources at the end, as they will help you solidify your understanding of the topics presented. There’s still a lot to learn, but as you can see, digital banking is a fascinating, albeit slightly complex aspect of the digital world we all live in.

Resources

Elkins, J. (2022, April 28). Modern Treasury Journal — How Do Core Banking Systems Work? Modern Treasury. https://www.moderntreasury.com/journal/how-do-core-banking-systems-work

Lambrinov, K. (2022, September 23). What is core banking? Sopra Banking Software | Banking & Financing Platforms. https://www.soprabanking.com/insights/what-is-core-banking/