Pricing Tools & Product Abstraction in Digital Banking: A Complete Guide

(Simplifying Complexities: How Abstraction Tools Empower Faster Digital Banking Innovation; #15 in the Digital Banking and Fintech series)

Table of contents:

· Intro · What are the key features and capabilities of a pricing and product abstraction tool or platform? ∘ 1. Abstraction of Pricing and Product Data ∘ 2. Reduces Complexity ∘ 3. Individual Offers ∘ 4. Audit Trails · Conclusion

Intro

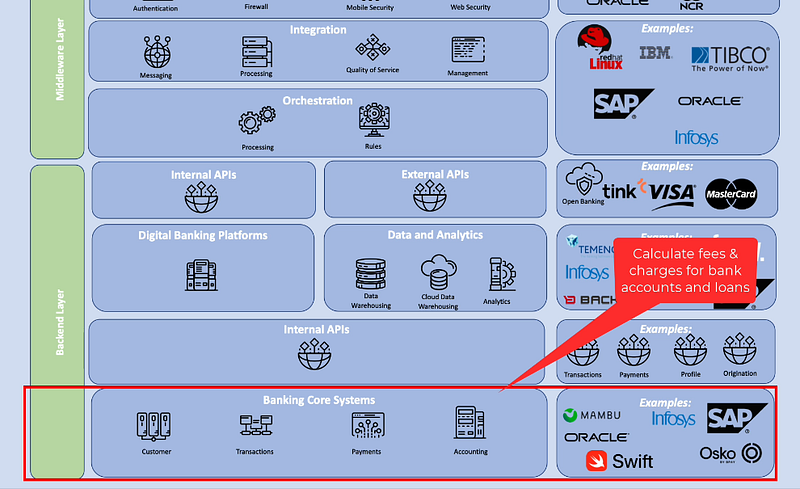

In my recent article covering core systems, I emphasised the ability to host and support software that lets accounts execute payments and calculate fees and charges.

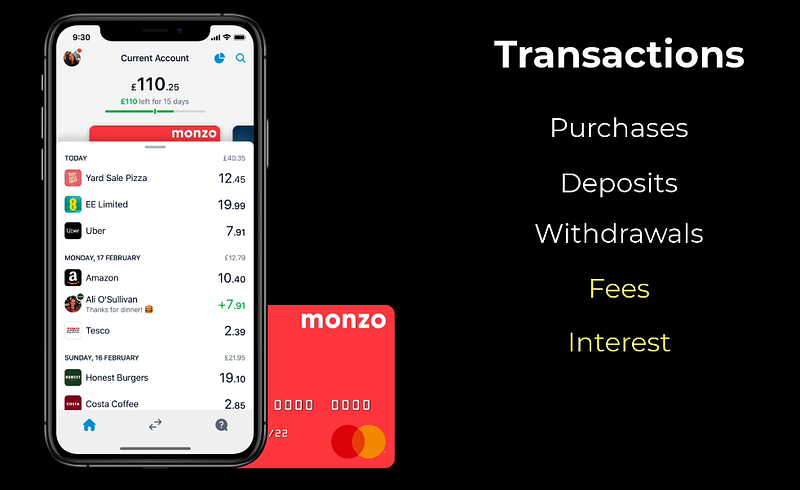

If you stop for a second and consider your digital banking. What do you see when you look at transaction views in your digital banking application?

You’ll see a list of previous transactions that include both items you did and things the bank applied to your account.

These include fees and interest that you must pay, as well as interest paid by the bank to you. All of this must be determined using a bank’s core system.

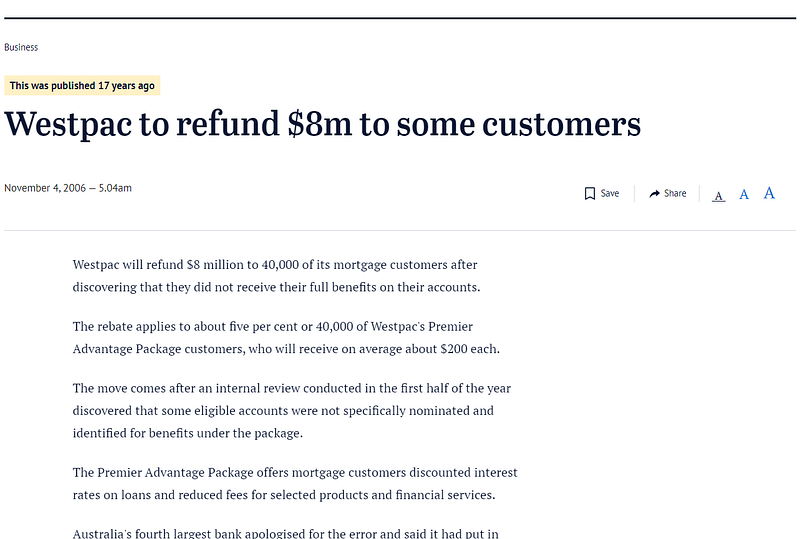

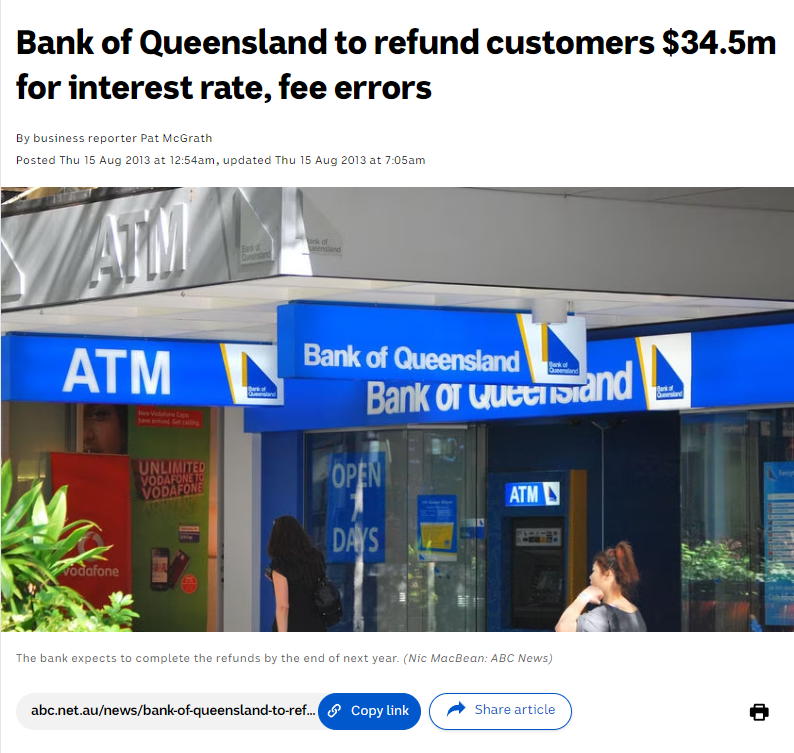

And calculating fees and interest over millions of accounts is really difficult. A bank must get this right because clients would be upset if they’re overcharged interest or fees, and since its profit and loss depend on these calculations.

Thus, pricing tools have become a significant concern and component of a financial system architecture that allows for digital banking.

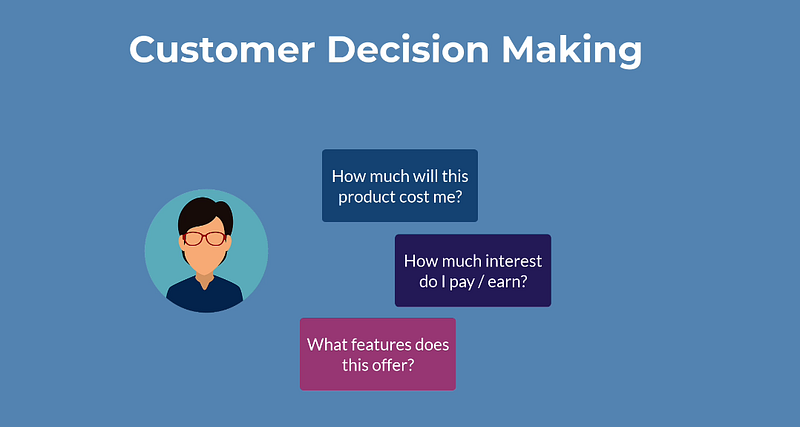

Customers examine the interest rate they can earn or be charged and the fees connected with having products at a bank when choosing a bank.

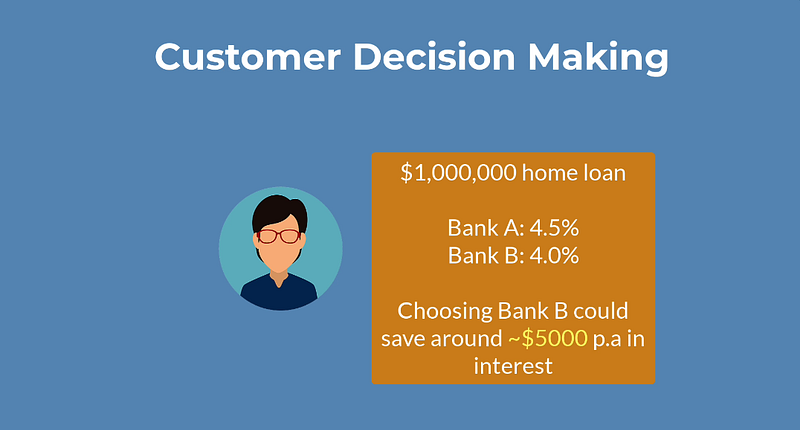

For instance, if I want to borrow $1 million for a property, and I check around the market and find that there are many interest rates available, I will want to spend time researching those interest rates to determine which bank will offer me the greatest deal.

A 50 basis point differential in interest rates between two banks may cost me $5,000 per year on $1 million.

A millionaire who can afford a $1 million property won’t think $5,000 is much. However, it’s extra money they’re paying a bank that they could be saving for larger expenses like flying across the world on a private plane. So pricing matters in this context.

“Pricing refers to the fees and interest that a bank will charge or pay you. When most consumers compare banks, it serves as a point of competitive differentiation.

Digital banking experiences matter when choosing a bank. However, ultimately, how much a consumer spends to keep banking products with a bank matters most.

In addition to pricing, digital banking and banking in general have linked features and capabilities incorporated into their products.

For instance, do transaction accounts come with debit cards? Can I use that debit card for Visa or Mastercard online purchases? Are there payment constraints on that transaction account that may prevent me from completing my usual banking?

Hence, for every bank product, the core system must build a set of features and capabilities to ensure that products perform what the bank promotes and expects. And even in digital banking channels, product features and permissions for what they can and can’t do must be defined and regulated.

For example, can I use a credit card for making rental payments? Probably improbable, but these are the kinds of problems that every product supplied through a digital banking channel must assess and resolve.

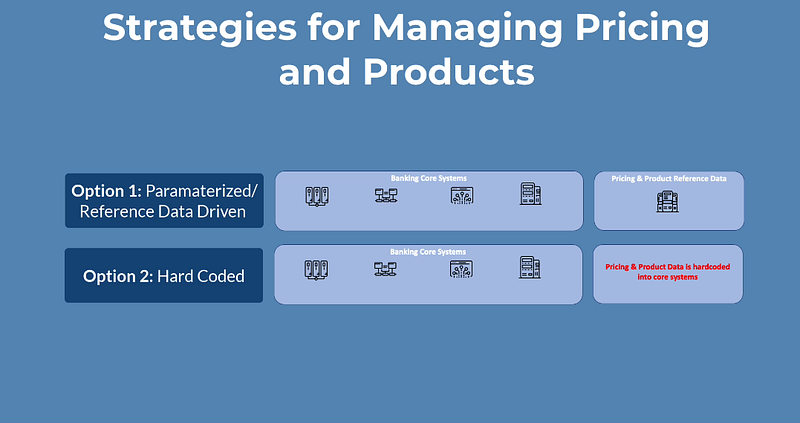

Typically, interest rates, as well as the features and permissions connected with items, are built into core systems.

If it was well-designed, these settings might be adjusted simply, such as when interest rates change. However, a poor design could imply these characteristics are hard-coded into core system functionality. Hence, if this logic is baked into a core system, changing these parameters is more complicated and time-consuming. Moreover, it’s also risky because you’re changing code that could affect the core system.

Over time, several banks have mismatched pricing and feature logic for banking products. Some have been proactive and written highly parameterized components, while others have hard-coded this into a logic that makes updates difficult.

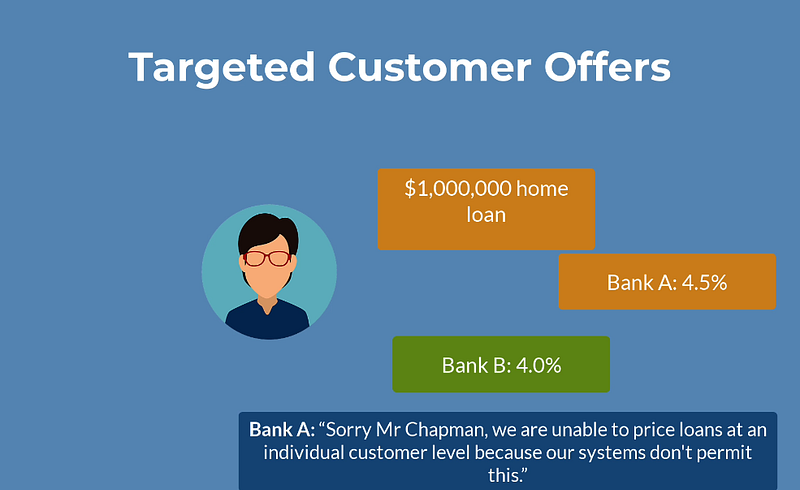

There’s also another factor that has historically limited banks. When you run pricing and core systems at scale, your bank’s ability to offer competitive pricing at the individual customer level is limited.

For a practical example, Imagine I’m getting a $1 million house loan from Bank A, but Bank B contacts me and says they can undercut the interest rate. As a current customer, Bank B will negotiate a 4% interest rate instead of 5%. When I tell Bank A about this, they can’t match this rate, not because they don’t want to, but because their core systems prevent them from pricing per customer.

Because it lets you make tailored offers to individual customers, pricing becomes a competitive differentiator in digital banking and banking as a whole.

Additionally, digital banking success requires the capacity to ship rapidly in a market driven by the demand for responsive and timely creation of new banking and digital products.

Other advanced fintech banks have shown this to customers. This is another example of their standard.

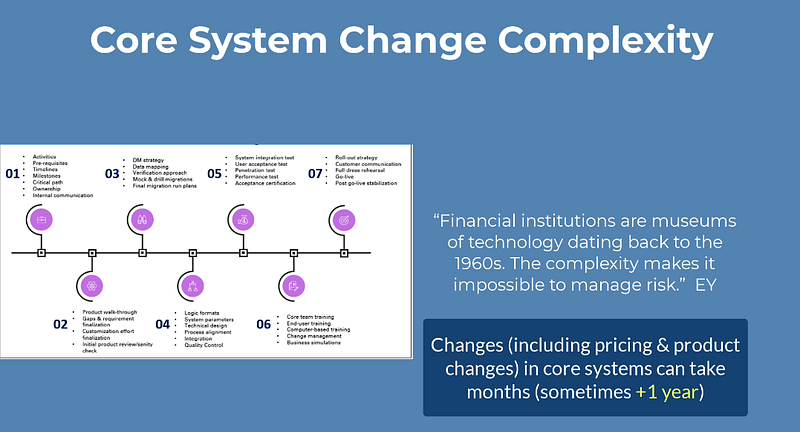

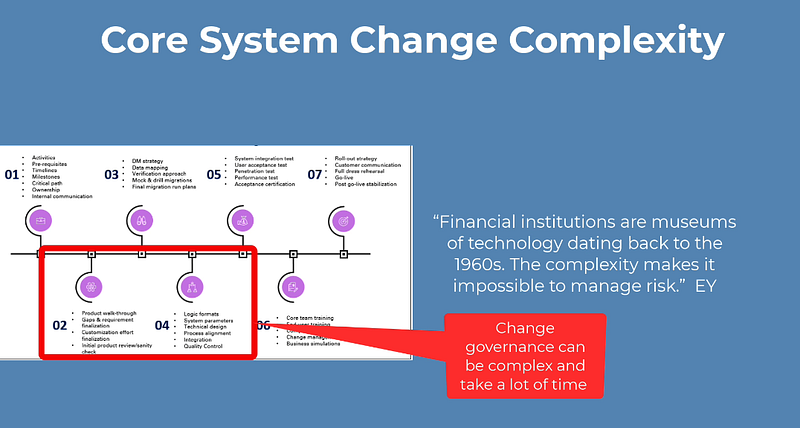

Thus, in many banks today, providing new products or changing digital banking features requires several procedures, protocols, and governance and management approval. Changing core systems to accommodate new product pricing and features compounds this problem.

As I mentioned in a recent article, making changes in core systems takes a large amount of time. This lead period is frequently months. To make matters even more difficult, there are frequent blackout periods each year when updates to core systems are not permitted.

As a product manager trying to alter digital banking and provide new solutions, you can directly notice some of the biggest challenges.

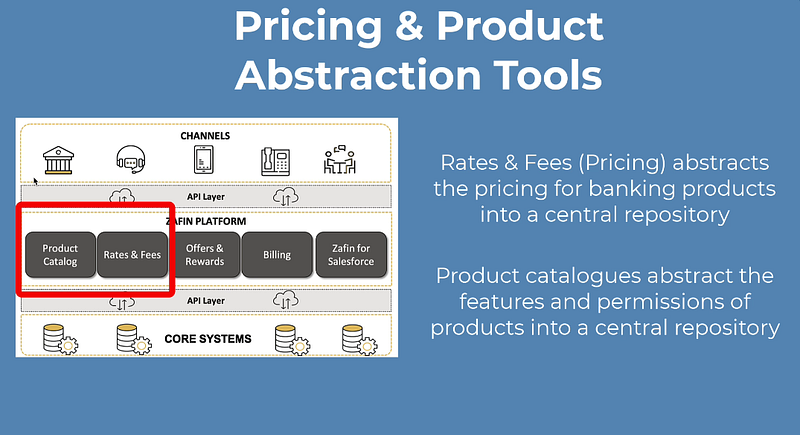

Pricing and product abstraction techniques provide instant utility in this situation. They are becoming essential to the design of any digital bank. They provide speedier, more transparent modifications and customer-level pricing by abstracting core systems, pricing factors, and product parameters.

What are the key features and capabilities of a pricing and product abstraction tool or platform?

1. Abstraction of Pricing and Product Data

Abstracting core systems, pricing, and product parameterization are their first capabilities.

Because of its various benefits, you can make adjustments faster and simpler. You can also get all your product pricing and parameterization reference information in one spot. This avoids the need to navigate tens or hundreds of core system touchpoints to figure this out.

2. Reduces Complexity

Secondly, it reduces the complexity of the change.

Product or pricing parameterization adjustments usually require several assessments and governance checks. Even minor adjustments might require a lot of work from product leaders, which can distract them from more critical tasks like choosing digital banking services for clients.

Many pricing and product abstraction technologies offer workflows for change review and approval, making the process faster and more efficient.

3. Individual Offers

These tools are now available to deliver individualised customer-level solutions, allowing banks to be more competitive in their efforts to attract and keep clients.

4. Audit Trails

Finally, pricing and product abstraction tools offer transparency and audit trails for price changes and product features. This is crucial to ensuring that at any one time, a snapshot of the fees charged and the interest rates applicable to them is available. This significantly reduces the risk of erroneous fees, improper interest, and even incorrect product features being applied, which may be costly to remedy when a bank makes a mistake like this.

Overall, digital banking, pricing and product abstraction tools are vital components in creating fast delivery and compelling product propositions.

Conclusion

In the fast-paced world of digital banking, agility is king. Pricing and product abstraction tools are no longer optional — they’re essential weapons in the battle for customer loyalty and market share. By abstracting core systems and enabling dynamic pricing, these tools unlock a new level of speed, flexibility, and personalization.

Banks can ditch one-size-fits-all offerings and craft tailored solutions for individual customers, all while streamlining approval processes and minimizing downtime. With these superpowers in their back pocket, banks can accelerate innovation, deliver compelling product propositions, and build a digital banking experience that truly stands out.

The future of banking is not static; it’s dynamic, personalized, and driven by tools that break free from the limitations of yesterday. Embrace the power of abstraction and watch your digital banking journey take flight.

Take your understanding of Digital Banking and FinTech to the next level with my series!