1Y 5 Asset Portfolio Optimization with PyPortfolioOpt: Min Volatility vs Optimal Risky Models

- In algo-trading, Portfolio Optimization (PO) methods [1–5] aim to pick and size positions in financial instruments that achieve the desired risk-return trade-off regarding a benchmark.

- The objective of this post is to evaluate the PO algorithm [3] that implements the PyPortfolioOpt efficient frontier or mean-variance optimization (MVO) techniques for calculating the expected returns and covariance matrix from historical stock data.

- Conventionally, MVO requires knowledge of the expected returns and a risk model.

- The

expected_returnsMVO module provides functions for estimating the expected returns of the assets. By convention, the output of these methods is expected annual returns. It is assumed that daily prices are provided. - The most commonly-used MVO risk model is the covariance matrix, which describes asset volatilities and their co-dependence.

- As a quick example, we’ll optimize a diversified 1Y portfolio of the following 5 US stocks: XOM, LMT, AAPL , LYTS, and VRTX representing energy, aerospace/defense, BigTech, manufactures, and biotech sectors, respectively.

Let’s delve into the specifics of the proposed PO strategy.

Basic Imports & Installations

- Setting the working directory YOURPATH

import os

os.chdir('YOURPATH') # Set working directory

os. getcwd() - Installing Python libraries with pip

!pip install yfinance, pyportfolioopt

- Importing Python libraries/modules

import pandas as pd

import numpy as np

from datetime import datetime

import matplotlib.pyplot as plt

plt.style.use("fivethirtyeight")

from pypfopt.efficient_frontier import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

from pandas_datareader import data as pdr

import yfinance as yfin

yfin.pdr_override()Input Historical Stock Data

- Defining the stock tickers and the time period

#get the stock symbols in the portfolio

assets = ["XOM", "LMT", "AAPL" , "LYTS", "VRTX"]

weights = np.array([0.2,0.2,0.2,0.2,0.2])

start='2022-01-03'

end='2023-03-10'- Fetching the Adj Close price of the above stocks

#create a dataframe to store the adjusted close proce of the stocks

df = pd.DataFrame()

#Store the adjusted close price of the stock into the df

for stock in assets:

df[stock] = pdr.get_data_yahoo(stock, start =start, end=end)["Adj Close"]

df.tail()

XOM LMT AAPL LYTS VRTX

Date

2023-03-03 112.809998 477.890015 151.029999 15.10 290.510010

2023-03-06 113.809998 480.170013 153.830002 15.00 291.619995

2023-03-07 111.610001 478.660004 151.600006 15.04 286.579987

2023-03-08 109.980003 479.500000 152.869995 15.20 285.179993

2023-03-09 109.129997 475.850006 150.589996 15.88 286.880005

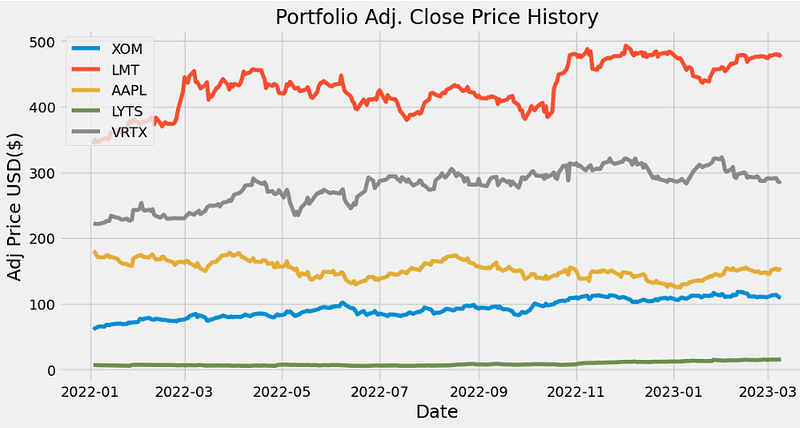

- Plotting the Adj Close Price History

plt.figure(figsize=(12,6))

title = "Portfolio Adj. Close Price History"

my_stocks = df

#create and pllot the graph

for c in my_stocks.columns.values:

plt.plot(my_stocks[c], label = c)

plt.title(title)

plt.xlabel("Date", fontsize =18)

plt.ylabel("Adj Price USD($)", fontsize=18)

plt.legend(my_stocks.columns.values , loc = "upper left")

plt.show()

Simple Annual Portfolio Volatility vs Returns

- Calculating the daily return

returns = df.pct_change()

returns

XOM LMT AAPL LYTS VRTX

Date

2022-01-03 NaN NaN NaN NaN NaN

2022-01-04 0.037614 0.021532 -0.012692 0.005806 -0.003011

2022-01-05 0.012437 -0.010636 -0.026600 -0.014430 -0.001983

2022-01-06 0.023521 -0.000391 -0.016693 -0.026354 0.001039

2022-01-07 0.008197 0.005978 0.000988 0.000000 0.000902

... ... ... ... ... ...

2023-03-03 0.012657 -0.000878 0.035090 0.010710 -0.000860

2023-03-06 0.008864 0.004771 0.018539 -0.006623 0.003821

2023-03-07 -0.019330 -0.003145 -0.014496 0.002667 -0.017283

2023-03-08 -0.014604 0.001755 0.008377 0.010638 -0.004885

2023-03-09 -0.007729 -0.007612 -0.014915 0.044737 0.005961

297 rows × 5 columns- Creating the annualized covariance matrix

cov_matrix_annual = returns.cov() * 252

cov_matrix_annual

XOM LMT AAPL LYTS VRTX

XOM 0.114765 0.029406 0.031630 0.023136 0.022189

LMT 0.029406 0.063479 0.018394 -0.000315 0.016949

AAPL 0.031630 0.018394 0.118594 0.030997 0.046592

LYTS 0.023136 -0.000315 0.030997 0.262411 0.013499

VRTX 0.022189 0.016949 0.046592 0.013499 0.094169- Computing the portfolio variance as the dot product of (uniform) weights and the above matrix

port_variance = np.dot(weights.T, np.dot(cov_matrix_annual, weights))

port_variance

0.044734897834191295- Calculating the portfolio volatility aka standard deviation (std)

port_volatility = np.sqrt(port_variance)

port_volatility

0.21150625956266944- Calculating the annual portfolio return

portfolioSimpleAnnualReturn = np.sum(returns.mean()* weights)*252

portfolioSimpleAnnualReturn

0.37951677200034234

- Printing the the expected annual return, volatility (risk), and variance

percent_var = str(round(port_variance,2)*100) + "%"

percent_vols = str(round(port_volatility,2)*100) + "%"

percent_ret = str(round(portfolioSimpleAnnualReturn,2)*100) + "%"

print("Expected annual return:" + percent_ret)

print("Annual volatility/risk:" + percent_vols)

print("Annual variance:" + percent_var)

Expected annual return:38.0%

Annual volatility/risk:21.0%

Annual variance:4.0%The Efficient Frontier Optimal Portfolio: Min Volatility vs Max Sharpe Ratio

- Calculating the expected returns the annualized sample covariance matrix of asset returns

mu = expected_returns.mean_historical_return(df)

S = risk_models.sample_cov(df)

#optimize for max sharpe ratio

ef = EfficientFrontier(mu , S)

weights = ef.max_sharpe()

cleaned_weights = ef.clean_weights()

print(cleaned_weights)

ef.portfolio_performance(verbose= True)

OrderedDict([('XOM', 0.36259), ('LMT', 0.26129), ('AAPL', 0.0), ('LYTS', 0.34074), ('VRTX', 0.03539)])

Expected annual return: 69.8%

Annual volatility: 25.0%

Sharpe Ratio: 2.71

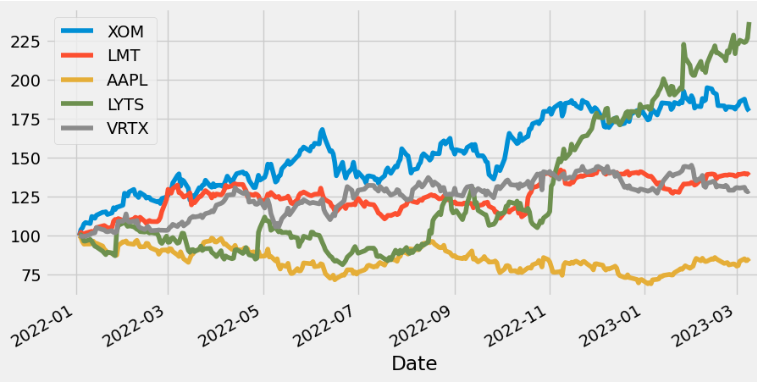

(0.6975504213382199, 0.24989435276114166, 2.711347470848402)- Plotting the cumulative returns (%) of our assets

(df / df.iloc[0]*100).plot(figsize=(10,5))

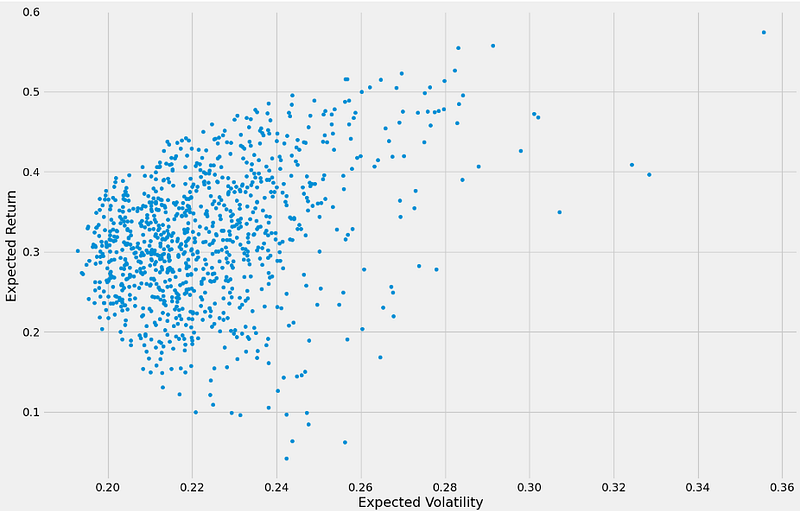

- Performing 1k random simulations of portfolio returns vs volatilities

log_returns = np.log(df/df.shift(1))

portfolio_returns = []

portfolio_volatilities = []

for x in range(1000):

weights = np.random.random(len(assets))

weights /= np.sum(weights)

portfolio_returns.append(np.sum(weights * log_returns.mean()) * 250)

portfolio_volatilities.append(np.sqrt(np.dot(weights.T,np.dot(log_returns.cov() * 250, weights))))

portfolio_returns = np.array(portfolio_returns)

portfolio_volatilities = np.array(portfolio_volatilities)

- Plotting the efficient frontier in the xy-domain (x=’Volatility’, y=’Return')

portfolios = pd.DataFrame({'Return': portfolio_returns, 'Volatility':portfolio_volatilities })

portfolios.plot(x='Volatility', y='Return', kind='scatter', figsize=(15,10));

plt.xlabel('Expected Volatility')

plt.ylabel('Expected Return')

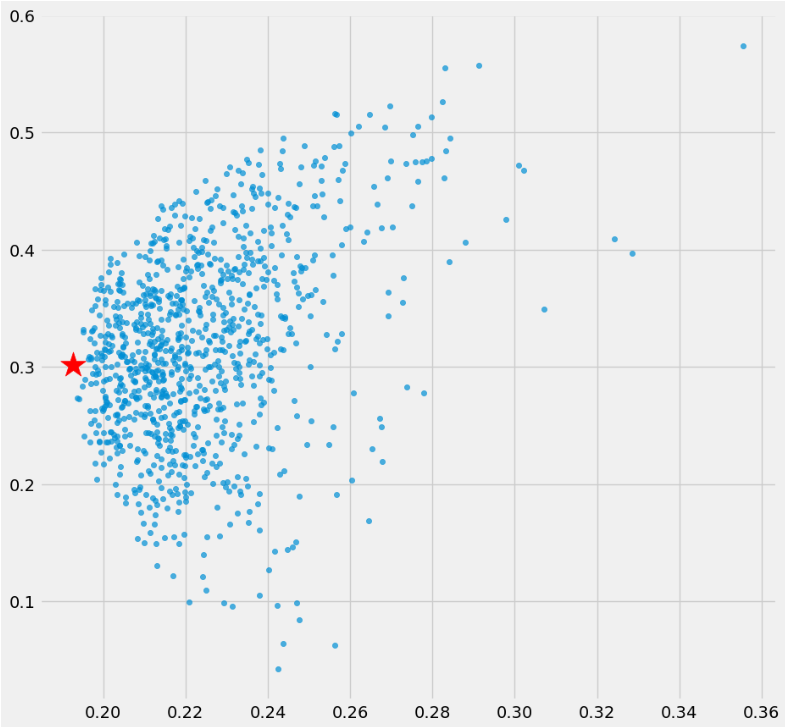

- Calculating and plotting the minimum volatility portfolio (red star marker) vs the efficient frontier

min_vol_port = portfolios.iloc[portfolios['Volatility'].idxmin()]

# idxmin() gives us the minimum value in the column specified.

min_vol_port

Return 0.301451

Volatility 0.192731

Name: 670, dtype: float64

plt.subplots(figsize=[10,10])

plt.scatter(portfolios['Volatility'], portfolios['Return'],marker='o', s=20, alpha=0.7)

plt.scatter(min_vol_port[1], min_vol_port[0], color='r', marker='*', s=500);

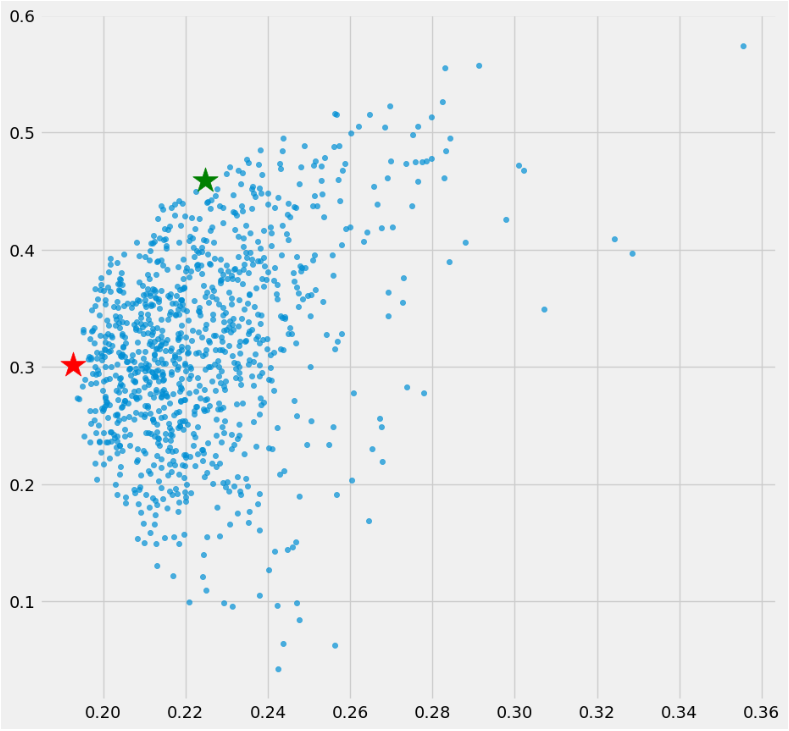

- Finding and plotting the minimum volatility portfolio (red star marker) vs the optimal risky portfolio (green star marker) overlaid by the efficient frontier

# Finding the optimal portfolio

rf = 0.01 # risk factor

optimal_risky_port = portfolios.iloc[((portfolios['Return']-rf)/portfolios['Volatility']).idxmax()]

optimal_risky_port

Return 0.458918

Volatility 0.224676

Name: 42, dtype: float64

# Plotting the optimal portfolio

plt.subplots(figsize=(10, 10))

plt.scatter(portfolios['Volatility'], portfolios['Return'],marker='o', s=20, alpha=0.7)

plt.scatter(min_vol_port[1], min_vol_port[0], color='r', marker='*', s=500)

plt.scatter(optimal_risky_port[1], optimal_risky_port[0], color='g', marker='*', s=500);

Conclusions

- We have calculated the risk adjusted return using the PyPortfolioOpt efficient frontier.

- We have optimized a diversified 1Y portfolio of the following 5 US stocks: XOM, LMT, AAPL , LYTS, and VRTX.

- Our optimal risky portfolio yields

Return 0.458918

Volatility 0.224676- Despite the wide use of Sharpe Ratios to compute risk adjusted returns, it is not without its disadvantages. Thus, if the expected returns do not follow a normal distribution or if the portfolios possess non-linear risks, the present PO approach may not deliver results.

- The Road Ahead: Constrained Portfolio Optimization (CPO). Besides the objectives of maximizing return and minimizing risk, CPO is constrained by the investor’s preference for certain asset classes or assets.

Explore More

- Stock Portfolio Risk/Return Optimization

- Risk/Return QC via Portfolio Optimization — Current Positions of The Dividend Breeder

- Portfolio Optimization Risk/Return QC — Positions of Humble Div vs Dividend Glenn

- Risk/Return POA — Dr. Dividend’s Positions

- Towards Max(ROI/Risk) Ratios Trading

- Portfolio Optimization of 20 Dividend Growth Stocks

- Applying a Risk-Aware Portfolio Rebalancing Strategy to ETF, Energy, Pharma, and Aerospace/Defense Stocks in 2023

- Risk-Aware Strategies for DCA Investors

- Blue-Chip Stock Portfolios for Quant Traders

- Returns-Volatility Domain K-Means Clustering and LSTM Anomaly Detection of S&P 500 Stocks

- A Market-Neutral Strategy

References

- Chapter 15- Portfolio Optimization: Algorithmic Trading 101 series

- Algorithmic trading simplified: Value at Risk and Portfolio Optimization

- Portfolio Optimization

- Portfolio Optimization with Sharpe Ratio

- Portfolio Trading using PyPortfolioOpt (A Python Library for Portfolio Optimization)

Contacts

Disclaimer

- The following disclaimer clarifies that the information provided in this article is for educational use only and should not be considered financial or investment advice.

- The information provided does not take into account your individual financial situation, objectives, or risk tolerance.

- Any investment decisions or actions you undertake are solely your responsibility.

- You should independently evaluate the suitability of any investment based on your financial objectives, risk tolerance, and investment timeframe.

- It is recommended to seek advice from a certified financial professional who can provide personalized guidance tailored to your specific needs.

- The tools, data, content, and information offered are impersonal and not customized to meet the investment needs of any individual. As such, the tools, data, content, and information are provided solely for informational and educational purposes only.