How to ACTUALLY Earn Passive Income from Credit Cards

Revealing my NEW credit card strategy for 2023

Can you earn passive income from everyday spending by swiping your credit cards?

If you do it right, absolutely!

And I’m not talking hundreds. I’m talking a thousand or even thousands a year with the right strategies.

Today I’m sharing actionable tips to help you make the most of your credit card usage. This video is perfect for beginners but it’s especially great for anyone who has dipped their toes into the credit card rewards waters but is ready to fully dive in.

I’ll cover:

- How to leverage sign-up bonuses

- How to master point redemptions

- How to maximize cashback

- 10 of my favorite tips and hacks

- My credit card portfolio

- My 2 NEW credit cards added this month

Let’s dive in…

(As always you can watch this story to learn more on YouTube here)

THE BASICS

As you probably know, you can use credit cards strategically to earn bonuses, points, rewards, or even cash directly in your pocket without changing your spending habits.

I haven’t swiped my debit card in over 6 years. If you swipe yours more than once a week or even once a month, you might be doing it wrong.

Let’s cover the 3 best ways you can earn passive income from credit cards you should be thinking about and planning for:

1. EARN SIGN-UP BONUSES

The easiest way to earn passive income from your credit cards is sign-up bonuses. This is usually in the form of cashback or points in one lump sum one time once you hit the required spending in a specific time period.

That might be as little as $1,000 in the first 30 days or as much as $10,000 in a six-month timeframe.

Be sure you earn this offer if it’s a compelling one.

But do NOT spend money you wouldn’t normally spend just to hit the bonus amount. Think about your spending habits and upcoming expenses before you sign up for a new card that has a sign-up bonus, especially if that required spending amount is high.

2. MASTER POINT REDEMPTION

Let’s talk about points. If you have a credit card that earns you points, it can be a little confusing. Generally speaking, $1 spent will earn you 1 point. 100 points can usually be redeemed for $1 or potentially more.

They all work a little differently so I can’t detail it here but spend time learning about your card’s specific point structure. Use this knowledge to redeem points optimally for travel, gift cards, merchandise, cashback, or statement credit.

Again, your points can go further if you master how to redeem them. For example, in my Chase portal, points can be redeemed 1.5:1 when used towards travel. But it’s 1:1 when used for gift cards or cash back as a statement credit.

3. MASTER CASHBACK

Cashback rewards are exactly what they sound like; money back after you spend. In most cases, they provide immediate value by reducing the amount of money you need to pay back on your card. In other cases, you might get a check in the mail or a gift certificate.

There are different types of cashback cards. The main types are flat-rate and category-specific cashback cards.

With a flat rate, you likely earn a set amount no matter the category of spending. A good example is the Citi Double Cash Back Card where you earn 2% back on all purchases.

With a category-specific card, you earn different percentages back depending on your category spending. This is outlined by each specific card.

For example, the Blue Cash Everyday Card from American Express gives you 3% back on groceries and gas and 1% on everything else. One unique card is the Citi Custom Cash Credit Card card which lets you earn 5% back on your top spending category.

10 TIPS FOR MASTERING PASSIVE INCOME WITH CREDIT CARDS

Here are my 10 best quick tips and hacks to help you master your credit card strategy for passive income:

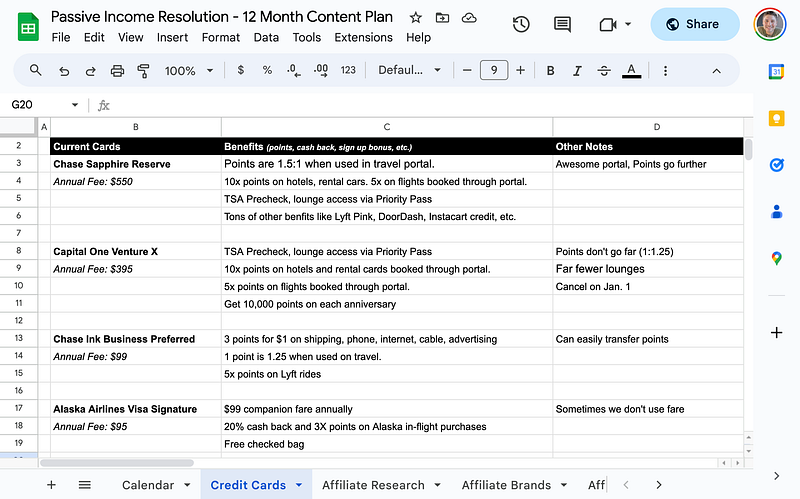

1. Understand Your Cards: I have to reiterate this point — know each card’s reward structure, spending categories, and benefits. Document this and review this annually because it can change. Here’s a look at how I did that this month.

2. Spend Strategically: Use specific cards for specific spending categories to earn higher rewards. Again, use your card knowledge to make sure you’re using each card for the right spending. There are ways you can ensure you do this. For example, keep your gas card in your car or only save one card in your Amazon account.

3. Pay Cards in Full: This is credit card 101. Avoid interest charges by paying off your balance in full each month. Interest and late payment fees can wipe out any earnings.

4. Combine Rewards: Consider having multiple cards to maximize rewards across various categories. You can choose to keep it simple and have 1 to 2 good cards. But I encourage you to go beyond and spend time researching as I did to see if there are better cards you can add to your credit card mix. Do this responsibly of course.

5. Redeem Wisely: Choose redemption options that offer the highest value per point or dollar. My example earlier was my Chase Ultimate Rewards points go further when redeemed for travel. Alternatively, I get 80 cents on the dollar if I were to use Chase points at checkout on Amazon.

6. Referral Bonuses: Refer friends and family to earn additional rewards. This is simple but something people often forget about. Here’s a referral link to my favorite travel card!

7. Annual Fees: Evaluate whether the rewards justify any annual fees your cards have. Cards with higher fees often offer better rewards and even perks (example: lounge access or TSA precheck). But if you don’t spend the card correctly, redeem points smartly, or take advantage of the perks, a high-fee card won’t be worth it. Some can be as much as $695 or more, but there are dozens of fantastic cards with zero annual fees. Reminder, annual fees can increase annually.

8. Keep Accounts Active: Regularly use your cards to prevent points from expiring. For some cards, points might expire after 5 years or you lose them if your card gets closed due to inactivity.

9. Utilize Online Portals: Some credit card companies offer extra rewards for shopping through their online portals. Chase has an excellent portal. Capital One… not so much in my opinion.

Am I crazy or does anyone else notice that most portals are very slow?! Why is that?

10. Don’t change your spending. Do not use cashback, points, or perks as a reason to spend more money. Don’t let welcome bonuses turn into shiny object syndrome. Use credit cards responsibly and avoid overspending for the sake of rewards.

MY CREDIT CARD PORTFOLIO

Here are the cards I’ve been using for the last 5+ years, what cards I’ve added this month, and what cards I’m closing.

Credit Card #1

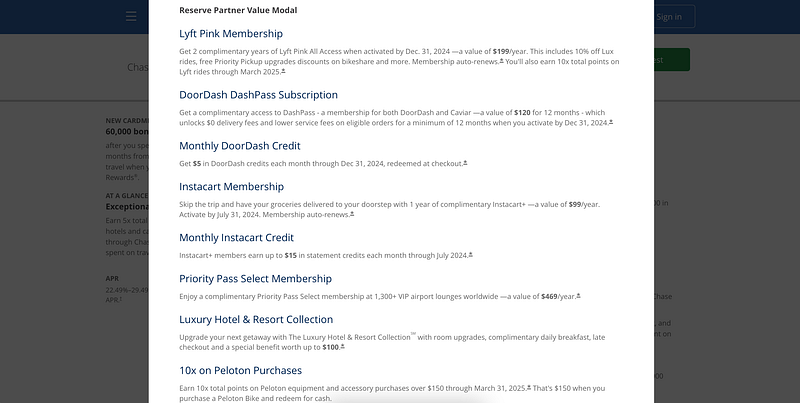

My go-to main card is the Chase Sapphire Reserve. This is a very expensive card so I only recommend it if you’re going to take full advantage of the benefits. It comes in at $550 a year but has loads of benefits I’ll show below — it’s far too many to summarize. Keep in mind, I do always earn $300 back in travel statement credit annually so it’s actually $250 a year. Much more palatable.

Credit Card #2

The card I used the next most is one I paired with my Reserve — the Chase Ink Business Preferred. This card is used to get me 3x points back on most expenses related to my business such as cable and cell phone bills. It costs $99 a year and I love how easily I can transfer points from this card to my Reserve card.

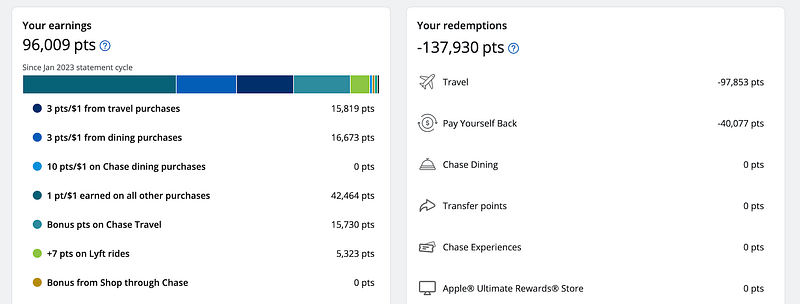

Between these two cards, I’ve redeemed 138,000 points in the last 12 months which was worth $1,868 between travel bookings and the pay-yourself-back feature. We took two trips this year and over half of our airfare, lodging, and transportation were covered by points which I earned passively.

Credit Card #3

The card I regret that I plan to close before my renewal in January is the Capital One Venture X card. This card had an attractive sign-up bonus at the time that I couldn’t resist but the points don’t go nearly as far as Chase points. Plus, several of the benefits overlap with my Reserve card because it’s also a travel card. Not to mention the high fee at $395 a year. I cannot recommend this card and I definitely regret it…

Canceled Credit Card

Last year I had one card get canceled on me due to inactivity and it was the card I had the longest so that wasn’t ideal for my credit score. It was the Alaska Airlines Visa Signature. Luckily, my wife still has this card. It does cost us $95 a year but we take advantage of the $99 companion fare credit annually. We honestly don’t need two as a couple so I don’t miss it.

MY NEW CREDIT CARD #1

Most of my current cards are focused on travel cards so I decided to dip my toes into the cash-back waters.

It didn’t take me long to identify 2 easy wins for myself and my family. Both of these cards I added this month are no-fee cards, which was non-negotiable for me. Both are store-specific because I don’t want to have to think about categories and cards when spending on the go.

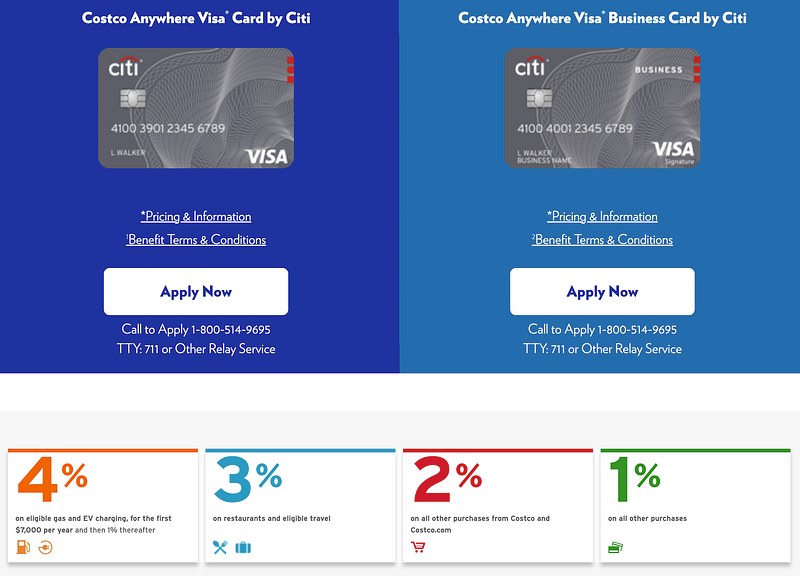

First, I signed up for the Costco Anywhere Visa Card by Citi. Since buying our first house almost 2 years ago, our Costco spending has doubled. We’ve had big purchases. We have more bathrooms to keep stocked. We have more houses to clean. We like to cost which gets spendy. You get the idea…

With this card I get 2% back on all purchases in addition to the 2% back I already get as an Executive Member. That’s 4% back on all Costco purchases. Plus, it’s a rare card that earns you 5% back on EV charging and we drive an electric so that’s awesome!

Looking back at my spending last year I spent $7,650 at Costco. I earned roughly 7,650 Chase points which equates to around $100 in redemptions. With the Costco card I would have earned $153.

Net Annual Earnings: $53

MY NEW CREDIT CARD #2

The other place we spend a lot of money is Amazon. And, fun announcement, WE’RE EXPECTING(!!!) so we expect to spend even more there in the next few years with a growing family. The Amazon Prime Visa makes sense for us. We get a whopping 5% back at Amazon.

Looking back at the last year we spent $2,340 at Amazon. We earned 2,340 Chase points worth around $30. With the Amazon card, we would have earned $117 in cashback the easy, automatic way.

Net Annual Earnings: $87

With these two cards, we are set to earn an additional $140 in passive income from everyday spending every year. I expect this number to be closer to $200 with a newborn plus EV charging. Plus, that $100 Amazon gift card bonus.

It’s not huge but it’s essentially free money after researching and making the credit card adjustment.

CREDIT CARD PRO TIPS

Pro Tip #1: If you are thinking about a cashback card don’t settle for less than 4% back on your top stores or spending categories. I strongly considered the Citi Custom Cash Card as well for 5% back on groceries. I’ll probably add a card specifically for groceries next year. Let me know if you have a recommendation.

Pro Tip #2: If your credit card mix gets complicated because you have to track by category, literally label your credit cards so you know which to use when you’re on the go.

Pro Tip #3: I challenge you to do what I did the last 30 days as a challenge. Review your spending. Review your credit cards and current benefits. Determine if you need to change which card you use per category, cancel cards, or add cards to the mix. Perhaps you too can earn hundreds or even thousands a year in passive income as I have in point redemptions.

Bottom line: With careful planning, credit cards can be a valuable tool for financial growth and passive income.

Important Reminder: Adding and removing credit cards will have an impact on your credit score. I recommend you track your credit for free as I do with Experian. Skip the paid plan when you sign up and you can still track your score.

What credit card is your go-to favorite? Mine is the Chase Sapphire Reserve. Which cards are you thinking about adding or subtracting from your credit card mix? What do you think of my cards and changes? I’d love to hear from you in the comments.

Check out one of my most popular 30-day challenges. Click here to learn about my selling Stock Photography or click here to watch my attempt at getting monetized on YouTube in 30 days.

This article contains affiliate links, which means I may earn a commission if you make a purchase using these links.

Wait a second. If you want to start writing on Medium yourself and earn money passively you only need a membership for $5 a month. If you sign up with my link, you support me with a part of your fee without additional costs to you.

Frankie Calkins (M. Ed) is a Digital Marketing Director by day. On nights and weekends, he’s an author, YouTuber, and course creator. He lives in the Seattle, Washington area. Contact: [email protected]