Withdraw it All ; The Collapse of Silicon Valley Bank (SVB)

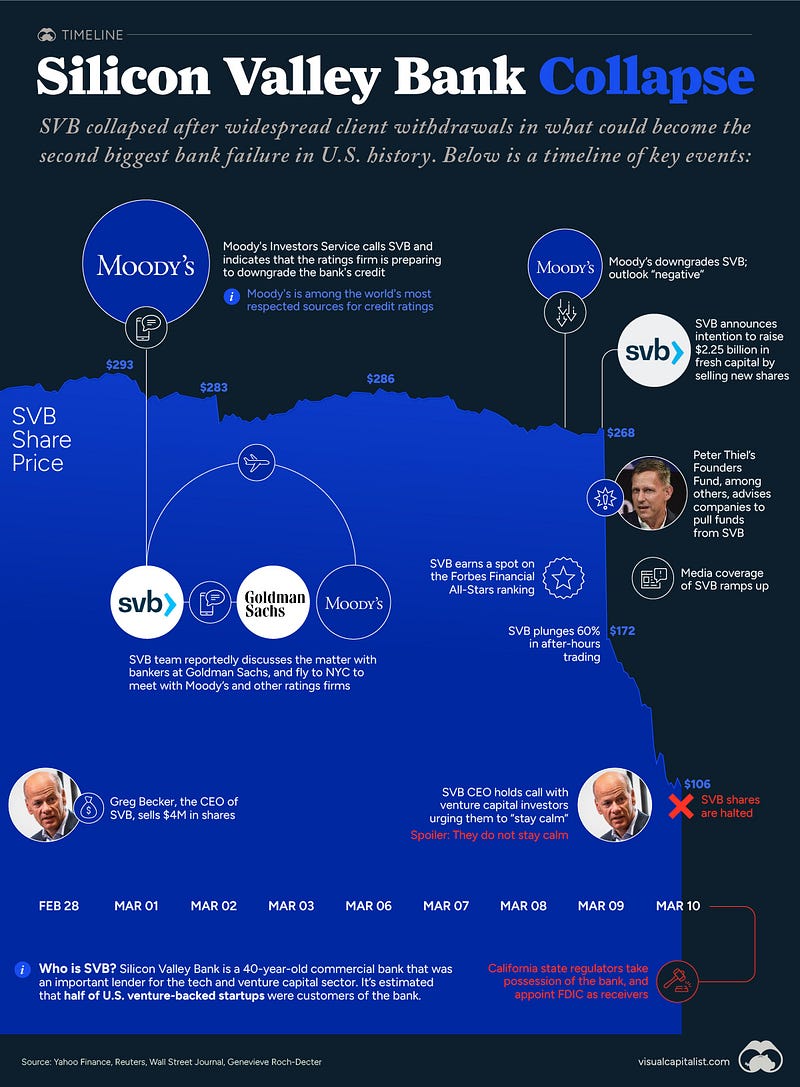

On March 12, 2023, Silicon Valley Bank (SVB) collapsed after a panic-induced bank run.

This is shocking news since just a few days ago, SVB was viewed as a highly-respected player in the tech space, with thousands of U.S. venture capital-backed startups as its customers.

How did this happen?

The bank found itself more exposed to risk than a typical bank as interest rates rose.

However, at the end of 2022, the bank’s balance sheet showed no cause for alarm. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list.

Outward signs of trouble emerged on March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moved to limit exposure to the 40-year-old bank, and a bank run ensued.

SVB had the highest percentage of uninsured domestic deposits of all big banks, totaling nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

The roots of the SVB collapse trace back to the early pandemic years when U.S. venture capital-backed companies raised a record $330 billion, and interest rates were at rock-bottom levels to help buoy the economy. However, as interest rates rose, all the money that was rushing to SVB’s customers was suddenly cut off.

In conclusion, the collapse of SVB is a stark reminder of the importance of managing risk and the potential fallout when things go wrong.

The tech industry and the wider financial world will undoubtedly feel the impact of this collapse, and it remains to be seen how this will affect the ecosystem of venture capital-backed startups that relied on SVB’s services.