Will China Bounce Back in 2024?

After three years of lockdowns and economic turmoil, China is hoping for sunnier days in 2024.

But significant headwinds remain. The government is facing difficult decisions about how much stimulus to provide and what growth targets to set.

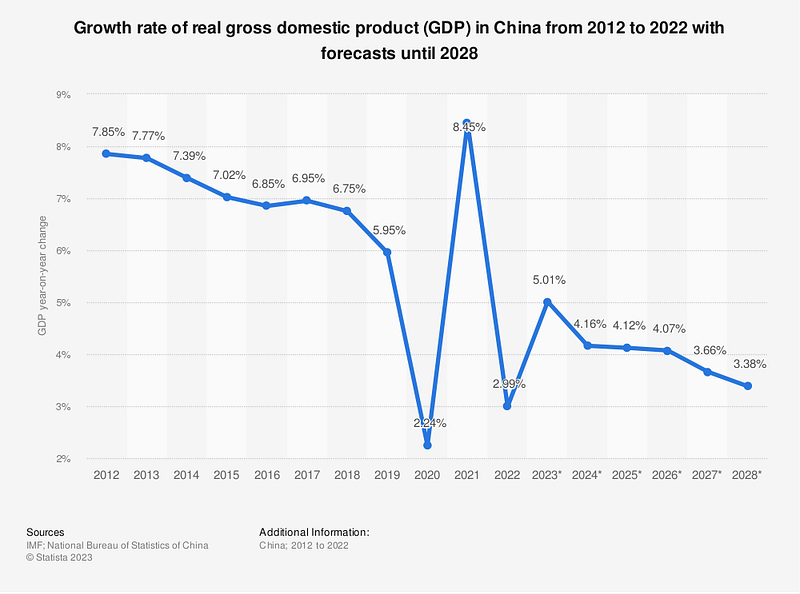

Most forecasters expect GDP expansion of around 4–5% next year, down from over 5% in 2023. Achieving even modest growth will require deft policymaking.

The property market remains China’s Achilles heel. Despite repeated government efforts to shore it up, housing sales plummeted in 2022, construction starts slowed dramatically, and developers struggled with massive debts.

These woes filtered through the economy, depressing demand for raw materials and crimping consumer spending. Although recent policy support has stabilized the sector, a quick, V-shaped rebound looks unlikely.

Most analysts expect a drawn-out recovery over several years. If pessimists are right that oversupply and demographic decline have structurally diminished housing demand, the property drag could persist.

Lacklustre global growth presents another headwind. As major Western economies flirt with recession and worldwide trade slows, external demand for China’s manufactured goods will falter.

Exports held up better than expected this year, but that resilience may not continue as the world economy cools. Russia’s invasion of Ukraine and deteriorating China-U.S. relations add further uncertainty.

On the bright side, China’s pandemic reopening and infrastructure push should buoy domestic consumption and investment.

Consumers still have pent-up demand and excess savings after years of restraint. Capital spending got a late start under the current 5-year plan but should accelerate with ample room in local government budgets. Meanwhile, tax cuts and special bonds have given a fiscal boost.

The policy dilemma facing officials is how aggressively to double down on stimulus given the mixed outlook. Growth could potentially surpass 5% with enough policy support, but that risks inflating new bubbles and adding to already dangerous debt levels. Alternatively, accepting slower growth around 4% would facilitate structural deleveraging while still keeping alive long-term doubling ambitions.

Threading the needle will require nuanced policy calibration. More infrastructure spending is needed but with tighter guardrails to prevent waste. Cheap credit for productive enterprises should continue, but tighter scrutiny of unproductive real estate lending.

The housing market needs targeted life support, not another tidal wave of credit.

In short, while China has bounced back from the pandemic, its economic challenges remain formidable.

Avoiding a protracted slowdown will demand wise policies that balance short-term support with long-term stability. Whether Beijing has the vision and discipline to walk this tightrope will become clearer in 2024.

© Buzzedison

Get step-by-step game plans to secure funding, build efficient systems, and scale your business the smart way delivered to your inbox weekly.