The Truth Is You Can Never Save for Retirement — Here’s Why

Life’s a beach… and there’s a hole in your bucket.

As I’m sure you’ve noticed recently, prices won’t stop rising.

In fact, this has been going on since day dot.

The famous Big Mac Index is an economic beacon — a standard measure of prices around the world and over time. And, no matter where you live in the world, I think we can all agree that this classic burger is not getting any cheaper.

I swear, when I was a kid the McDonald’s coupons offered me two Big Macs for $4. And they actually looked like a Big Mac.

Seriously, what are they now? $8 for one?

And they’re probably the size of a double cheeseburger with lettuce.

Pathetic.

The Invisible Tax

How much did your grandparents pay for their first house?

$3 plus a sack of potatoes?

OK, so maybe it was more like $103. But it was a mere fraction of the cost of a house today.

And what’s that house worth now? A cool, half million… at least.

Granny’s ballin’!

But what does this tell us about the value of money?

Money is nothing more than a number on a banknote or screen. A piece of paper has essentially zero value and a digital number has literally zero value. And yet, money is nothing more than pieces of paper and digital numbers.

So what is your money really worth?

Money, as we know it, is nothing real — it’s just a stored piece of perceived value. What we can afford to buy with it is called “purchasing power”. This is the true value of money, and it’s all based on what the economic system decides a certain number is worth in the bigger picture.

Losing Change

Today, the issue of “rising inflation” is a hot topic. In case you didn’t know, inflation is the general increase in the prices of goods and services over time.

Food, clothes, rent, and everything else that you can possibly pay for, continue to go up in price.

But what does this really mean for your money?

As prices are going up, the value of your money is going down.

Therefore, as inflation continues to take effect as prices rise, part of the value of the cash that’s stashed in your bedroom and bank account is lost.

Your money is slowly disappearing over time… and no one is sneaking into your room to steal any quarters!

Inflation is not a physical loss of money — it’s an invisible loss of your money’s worth. And now, that old $100 of pocket money that you could have spent on a new skateboard in 1997 can only afford you a few local Avocados from Wholefoods.

Bummer.

Historical figures estimate that the rate of inflation hovers around 3% per year. Over an average year, this means you lose 3% of what you’re worth.

Recently, however, inflation has been hovering dangerously at around 8% or more.

Every year, value is being lost.

The question is, where does this value go?

The Money Supply

“Americans are getting stronger. 20 years ago, it took two people to carry $10 worth of groceries.

Today, a 5 year old can do it” — Henny Youngman

There can be many reasons why money loses purchasing power as prices rise over time, but this broad trend has one major cause — more money being created.

Over time, there is an increasing supply of money coming from the banks and lenders who can generate new money like magic.

Under normal conditions, more money must equal higher prices. Why? Because the relative value of yesterday’s dollar is being diluted in a rising pool of money!

When money is being created at a faster rate than an economy is growing, more money is available to buy relatively less “stuff”, so the average price of that stuff must rise.

In simple terms, the amount of money in the system determines what piece of the pie your money represents.

Through the creation of new money, you must unfortunately pay a hidden, but very real, price.

It Rains, It Pours

Here is a simple example of inflation at work.

Imagine living on Coke Planet — a strange land with only 100 cans of Cola for sale and $100 of money in circulation.

Because all the money affords all the Coke, each can will cost $1.

However, one day the sneaky Bank of Coke decides to print another $100. Now there’s $200 of money is circulating on Coke Planet. The money supply has suddenly doubled, but there has been no economic growth — there are still only 100 cans of Coke to purchase.

So what’s the outcome?

With twice as much money in the system, one of these cans of Coke will now cost you $2.

Or, in fact, your shiny dollar has just lost half of its purchasing power!

In very simplified terms, this is how inflation works. The real value of your money — its purchasing power — is being diluted over time as more money is injected into the system.

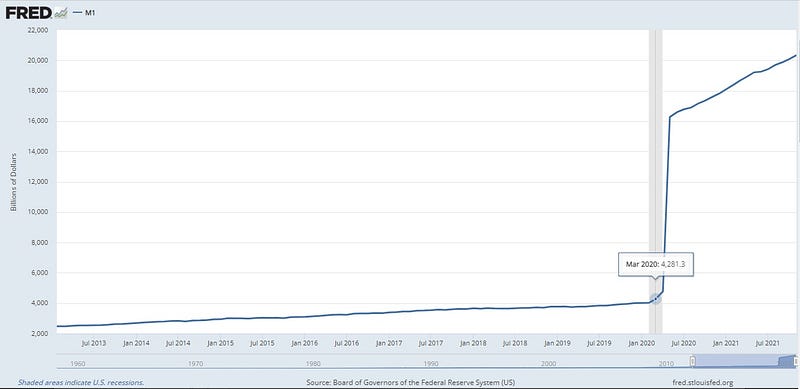

Forget about Coke Planet, here is what sudden money printing looks like in our world…

And with prices now soaring in 2022, we are just starting to feel the ripple effects.

The Power Strings

It’s normal for a country to experience some inflation as a by-product of economic growth. However, the rate of inflation must be carefully controlled by the “money composers” — the big banks and lenders that function under the watchful eye of the central bank.

The central banks largely maintain this control by adjusting interest rates.

Interest rates dictate the cost of borrowing money, which influences how people use their money and the amount of new money that is created.

Setting a low interest rate can help to stimulate an economy and increase inflation by encouraging people to borrow more money at a lower cost.

Lower interest makes money cheaper. Therefore, when interest rates are low and debt is most affordable, we tend to spend more money on credit, borrow more to buy houses, and we are more likely to take out loans to start new businesses.

The money creators are now pumping out money at a faster rate. And as more money starts flowing through the town to buy relatively less stuff, the price of this stuff must rise at a faster rate.

In recent times, interest rates around the world have recently been experiencing record lows as debt-driven markets — like stocks and real estate — reach record-high prices.

Notice the trend?

At the other end, increasing interest rates can help to slow down economic growth and the rate of inflation.

Higher interest rates make it more expensive to borrow money, which lowers the demand for debt and reduces the amount of new money being created.

High interest rates also encourage us to save our money in the bank, rather than spend it or try to cleverly invest it. We can simply keep our money in a savings account and earn a higher rate of return with little risk or hassle.

And what’s the flow-on effect here? Less spending, less new businesses and company investment and less demand for houses.

Ultimately, this helps to slow the rate of inflation.

The Cost of Convenience

Some people choose to save their money in the bank, while others stash it under the mattress. No matter how you store money, it’s cash that you can access and spend at any time.

When accessing your money is easy and convenient, the system is doing you a favor.

Most bank accounts cost us nothing — yet as we know, there are no freebies in this world!

So what’s the real cost?

The easier it is for you to access and play around with your money, the less financial reward you will receive.

Most convenient, everyday bank accounts offer us 0% interest on our money.

So, according to the simple laws of inflation, this means our money continues to fade at the exact rate of inflation.

This loss is 100% guaranteed.

Don’t be fooled, you are certainly paying a real price to keep your money in the “free” bank.

Banks make it easy and convenient for a reason, and that reason is not to be nice!

The Illusion of Saving

Ask a friend if they smartly manage their money and they may tell you about their new online savings account — with an annual interest rate of 1.5%.

For the time and effort it takes to move a few thousand dollars of hard-earned money around, they can watch in excitement as their “investment” earns them a free cup of coffee each month.

“$3 free money!”

Well, that’s at least what the numbers appear to be giving them…

Remember, the number in your bank account is not what’s important — what matters is what that number will ultimately afford you in this world.

Obviously, your friend doesn’t know about that greasy slimeball called “Inflation”, who is shaking us down this year for 8% or more of everything we’ve got.

So, what’s really left for your friend?

The truth is, far less than what they started with.

Plus, to only make matters worse, this small amount of interest earned must then be taxed as personal income!

Savings accounts are very rarely an investment.

Most often, they are a liability.

Final Thoughts

As we are all seeing right now, time is a force working against the average person’s money.

There is, therefore, only one way to turn money and time into progress — by doing more than the average person.

“The secret to success is in doing what most people will avoid.”

By learning how to invest smartly and follow an “inconvenient” plan, you can outrun inflation and encourage real growth of your money over time.

This is how you allow time to work for your money instead of against it.

This is how you really get ahead in life.