Why I keep $0 in a Savings Account and do not regret it one bit!

{kind=link}

Now you might be thinking that this is a foolish idea, right? After all, conventional financial wisdom teaches us that savings accounts are a fundamental component of a sound, financial strategy.

They are a safe and accessible way to store your money and earn reliable interest, typically paid into your account monthly. With interest rates remaining resilient at around 5% — 5.5% in both the U.K & U.S (as of February 2024), now seems like a great time to be storing your money in a savings account, right?

We all have different financial circumstances and this plays a crucial role in how you construct your financial portfolio but this is going to be the perspective of someone in their 20s since your age also plays a crucial role in how you save and invest your money.

I personally was never drawn to savings account as I viewed them as a mediocre way to get mediocre returns and realised early on that I could never get a meaningful return from savings accounts unless I invested at least a seven figure amount at which point, why bother with interest from savings account.

Growing up during the great recession and its aftermath, I had gotten used to being in a low interest rate environment for many years like many others and I had gotten used to the low interest rates offered by banks during the 2010s.

From 2010–2019, we witnessed one of the greatest bull runs in the stock market with the S&P 500 returning an average of 13.3% per annum. Although I personally wasn’t investing in stocks during that period, I closely followed the stock market and financial news in general and realised that what my parents were teaching me about putting money in a savings account was not going to cut it for me.

Now we all know what happened at the start of the 2020s and I saw this as a great opportunity to start pouring money into stocks so I put everything, and I mean literally every liquid capital I had to my name into stocks which was not much but a good place to start.

I viewed myself as a student of value investing after reading “The Intelligent Investor” by Benjamin Graham which is famously recommended by Warren Buffett.

I poured my capital into blue chip, dividend stocks which had taken a haircut in their valuations as a result of the pandemic and within months, I started seeing returns that I had never seen before as the market rapidly rebounded thanks to the trillions of dollars being pumped into the market by central banks along with the interest rate cuts.

I did make the mistake of selling a lot of my stock investments too early which does contradict what Benjamin Graham teaches in his book but I allowed my emotions to take over me from all the excitement to be making such quick, easy returns.

I do realise that it was the favourable market conditions that allowed me to get these returns, not my stock picking abilities and would always recommend anyone to hold their dividend stock investments for the long term by re-investing dividends for additional gains.

The point I am making is that the returns from investing in stocks has always been greater than putting your money in savings account and it will likely always remain this way if you are taking a long term approach to investing. In fact, the dividends alone are often far greater than the interest you receive from savings account, and once you take account of the capital appreciation of stocks, there is simply no comparison.

Now, obviously investing in stocks carries more risk which is why experts such as Warren Buffet recommends people to put their money in a low cost index fund such as the S&P 500 which carries little to no risk since you are essentially investing in the prosperity of the largest economy on the planet by backing the 500 largest companies in the U.S public markets.

There are also other indexes you can invest in such as the FTSE 100 if you are based in the UK like myself, but make sure to do your own research to decide which index is most suitable and which brokerage platforms offer the lowest fees.

I am no financial advisor, but if you are under 30 or have no dependents with little expenses, then the opportunity cost of leaving your capital in savings accounts is far too great due to the power of compounding returns.

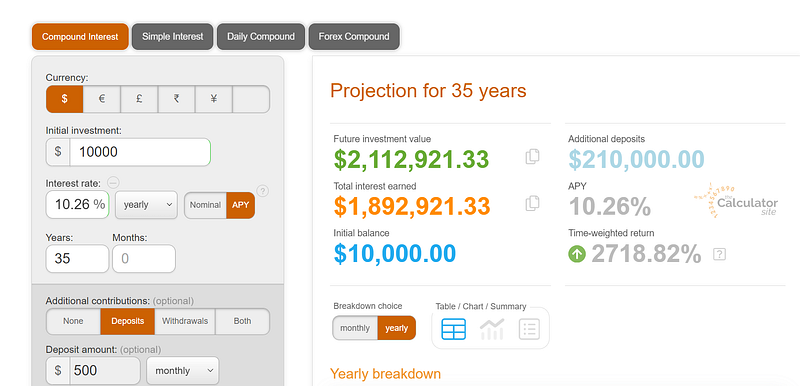

I will give you an example to illustrate the power of compounding returns by comparing the returns of the S&P 500 vs the very best savings accounts in the market today. The S&P 500 has returned on average 10.26% since its 1957 inception through the end of 2023 so this is the return I’ll be using in my demonstration.

Let’s say you are a 30 year old with $10,000 in savings to invest into the S&P 500 index and you continue investing $500 every month until you are 65 which is roughly the retirement age depending on where you live. The $500 that you invest monthly will not increase yearly with inflation to keep the math simple. This is what the numbers will look like:

By the time you retire at 65 years old, your investment value would be over $2.1 million with a time-weighted return of 2,718.82%. No wonder compound interest is known as the 8th wonder of the world.

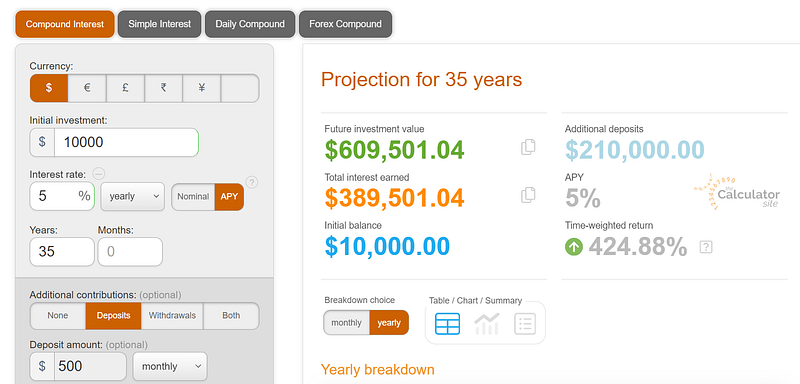

Using the same example, had you only used a savings account paying a competitive 5% interest per annum over 35 years, this is what the numbers would have looked like:

$609,501.04 is still a decent amount if you plan to retire somewhere like Thailand or Sri Lanka by using the 4% rule but it will certainly not be enough to retire in a developed country, especially not in 35 years.

This is why it is crucial to get the best risk-adjusted returns as early as possible and deciding to move your money from a savings account to an index fund that pays dividends like the S&P 500 is a good place to start.

Your future self and future children will thank you for the financial decisions you make today so always keep the opportunity cost in mind when deciding where to allocate your money and always think long term when it comes to saving & investing by remembering the power of compounding.

Disclaimer: Not Financial Advice

The content provided in this article is for informational purposes only and does not constitute financial advice. It is essential to conduct your own research or consult with a qualified financial advisor before making any investment decisions. The author is not responsible for any financial actions taken based on the information presented.