Why High Income Earners Go Broke: 5 Wealth Killers

An investigative look at the paradox driving 51% of six-figure salaries into living paycheck-to-paycheck

If you find yourself among the 51% of Americans earning $100,000 or more per year who are still living paycheck-to-paycheck, you’re probably wondering — how did this happen? How can someone making a six-figure salary be broke? As counterintuitive as it sounds, a high income is no guarantee of wealth accumulation.

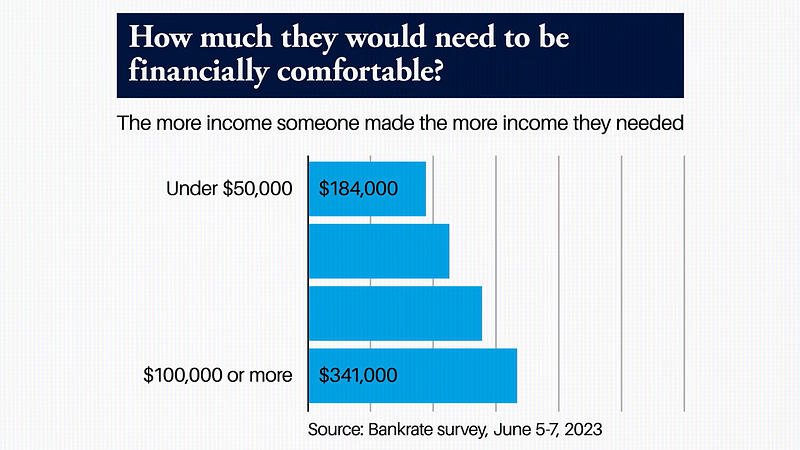

In an eye-opening survey, Americans across income levels revealed a startling disconnect between earnings and perceived financial comfort. Those earning under $35,000 per year said on average they needed just $184,000 in total income to feel truly comfortable. But for those already earning over $100,000? Their target “comfortable” income level skyrocketed to $341,000.

So what’s going on here? Why are so many high earners, despite their lofty salaries, still struggling to get ahead? This investigative blog dives deep into 5 key factors driving this income-wealth paradox.

Spending Your Raise Before You Get It: The Lifestyle Inflation Trap

For many professionals just entering the upper-income brackets, their current high earnings represent the first real taste of financial abundance after growing up in less affluent circumstances.

“Most of my friends including me grew up poor but are now considered high-income earners,” shared Vincent Chan — a finance YouTuber. “The problem is this is their first experience with having money, naturally they want to treat themselves and spend it in a way to compensate for their childhood when they didn’t have anything.”

This phenomenon, known as “lifestyle inflation”, occurs when consumption habits increase alongside income, leaving little leftover for saving or investing despite earning more.

It often starts small, like upgrading to a pricier apartment or smarter car. But over the years, ballooning costs on housing, dining, fashion, travel, and other lifestyle expenses can easily consume even a very healthy paycheck.

“It might start off as upgrading to a nicer apartment that costs $2,500 a month from one that costs $2,000,” Vincent Chan described. “Five years later you find out you’re spending $7,000 a month to live in a prime location with a Whole Foods around the corner.”

The allure of finally having disposable income to enjoy life’s luxuries is undeniable after years of scrimping and saving. But when this indulgence goes unchecked, even a high income can quickly be spent into oblivion. Setting clear financial goals and ringfencing a portion for saving/investing is critical to avoid lifestyle inflation.

The Great Deflation: Paychecks That Don’t Go As Far

While income and wealth are often used interchangeably, they are vastly different concepts.

Income represents the active inflow of money from employment, investments, or business revenues. Wealth is a stockpile of productive assets that generate income streams and increase exponentially over time through investing.

“Wealth isn’t about how much money you earn, it’s about how much money you keep,” as financial guru Dave Ramsey emphatically states.

Yet for many high earners, actively converting their income into wealth-producing assets is an afterthought or avoided entirely.

Part of the challenge? Despite earning higher salaries, the actual purchasing power of those incomes has been significantly eroded for major costs like education and housing by years of inflation outpacing wage growth.

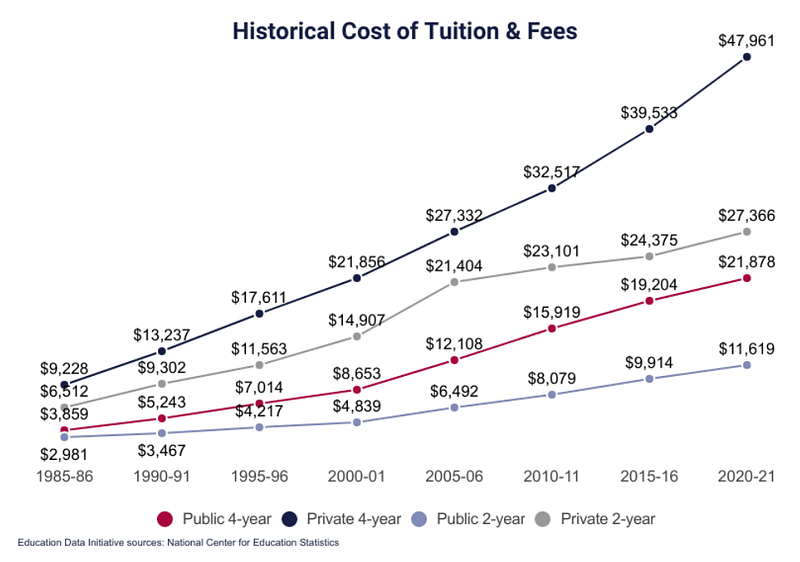

Consider the soaring costs of a college degree — increasingly a requirement for even entering the ranks of higher-income professions. “The average annual cost of tuition at a public 4-year college is now 37 times higher than it was in 1963,” according to the latest report from Education Data Initiative. With such exorbitant price tags, it’s no surprise that “higher income earners have more student debt — those earning over $97,000 owe $52,000 on average.”

Housing is equally problematic, with median home prices more than doubling since 2000, while incomes haven’t kept up. In major cities like New York and San Francisco where high earners concentrate, median monthly rents of $4,700 and $3,200 respectively are not uncommon. With 30% as the recommended maximum portion of income allocated to housing, these costs threaten to consume the majority of even a six-figure salary.

The net result? Despite higher gross earnings, the real spending power and savings capacity of today’s higher-income professionals is being severely constricted. Creating passive income streams from productive assets is essential to circumvent this erosion of real wages.

The Wealth Creation Paradox: Income vs Assets

So how can higher earners escape this loop of inflating lifestyles and deflating real incomes? By truly understanding the fundamental difference between active income and wealth-producing assets.

As the data clearly shows, “for millionaires, their income is only 8.2% of their wealth — the other 91.8% comes from assets like investments and businesses.” Or as the classic book The Richest Man in Babylon elegantly explains:

“Think of every dollar you have as a working employee who has the ability to earn more employees for you…those are assets that compound in growth.”

Capital continuously deployed into income-generating assets like businesses, rental properties, stocks or other investments is the core engine of long-term wealth creation. Yet far too many higher earners neglect or avoid taking this critical step.

The problem is many high-income earners don’t focus on converting their income into assets, either because they don’t know about it or they just think they can do it later. But the rule of thumb is the longer you hold assets, the earlier you start, the faster your wealth grows thanks to compounding returns.

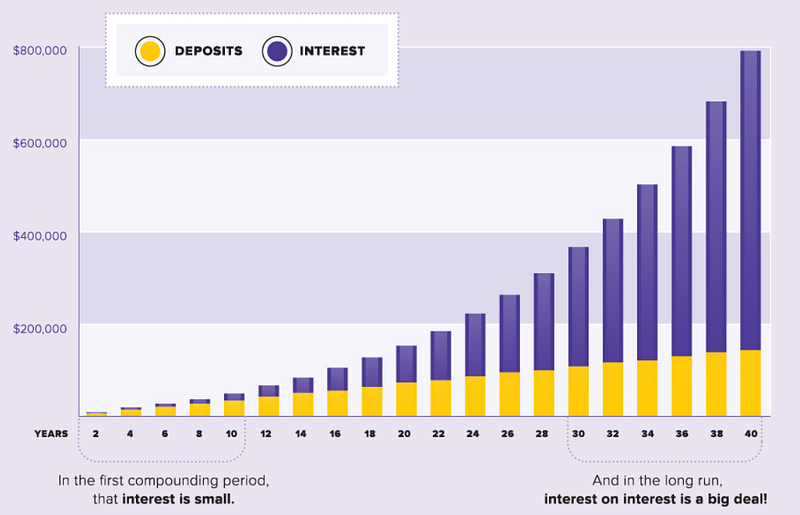

Indeed, compounding is perhaps the most powerful wealth-building force known. Yet its exponential growth trajectory is deceptively slow and unassuming at first, much like a seedling reaching for the light.

Look at this exponential growth curve below. Initially it might seem like nothing is happening at all, it looks pretty flat. But once you start converting your income into compounding assets, that’s when your wealth grows exponentially over years and decades.

The paradox is that those who most need to capitalize on compounding through assets are often those entirely neglecting it — the high-income earners relying solely on inflating salaries. Reversing this pattern through dedicated, consistent asset-building is crucial for achieving true wealth.

Keeping Up With Strangers: The Social Media Trap

Even for diligent higher earners purposefully building wealth, another formidable roadblock looms incessant societal pressure to spend conspicuously on goods and experiences. The primary driving force? An endless barrage of aspirational advertising and the rise of social media envy.

Billion-dollar companies constantly overwhelm us with ads suggesting we buy this or that, and people will recognize your success. The impact, particularly among millennials awash in these influences, is drastically altering spending habits away from prudence.

“90% of millennials say social media creates a tendency for them to compare their own wealth or lifestyle to that of their peers and influencers,” Vincent Chan showed — A startling “57% said they spent money they hadn’t planned to spend due to these aspirational comparisons.”

This phenomenon is known as “keeping up with the Joneses” — using one’s peers and social circle as the barometer to define the necessities for appearing successful, happy and affluent.

But today’s version is keeping up with the Kardashians and Joneses across the globe, thanks to social media’s pervasive reach. The lures of luxury labels, dream vacations, curated experiences, and ostentatious displays of wealth are unending.

The problem is it’s never going to stop — marketing and advertisements for products and experiences we don’t truly need are only going to keep increasing. People are going to keep spending trying to curate an enviable image, to impress strangers they don’t know and probably don’t care about.

Resisting these incessant external pressures to spend lavishly and channeling more income into wealth-producing assets is perhaps the greatest determinant of a high earner’s ability to achieve lasting financial prosperity.

The Wealth Accelerator: Optimizing Your Tax Burden

Finally, the internal factor separating many high-income earners from true wealth creation is their failure to implement legal tax reduction strategies. After all, it’s not what you earn that matters, but how much of it you keep after taxes.

The problem is many high-income earners don’t pay as much attention to systematically reducing their taxes as they should. But it could be the difference between paying $10,000 or even $100,000 more in taxes throughout their career.

From maximizing retirement account contributions to leveraging deductions to structuring investments and businesses in a tax-efficient manner, prudent tax planning represents a remarkable wealth accelerator and savings turbocharger. Yet all too often, these strategies go underutilized by higher earners focused solely on chasing the next salary increase.

The good news is reducing your taxes legally isn’t as complicated as many think. With some basic education, it’s very feasible to reduce your annual tax obligation substantially and keep more of your hard-earned income working for you.

Implemented consistently over decades, diligent tax planning and reduction can dramatically amplify wealth accumulation and provide breathing room in the budget to invest more, even for very high earners in the highest tax brackets.

It’s a Wealth Mindset, Not an Income Mindset

At the end of the day, avoiding the “broke high earner” trap comes down to a fundamental shift in mentality — from prioritizing high income to prioritizing wealth accumulation through assets and compounding growth.

It requires delaying gratification in the face of societal pressures and resisting the allure of lifestyle inflation. It demands optimizing drains on that income stream like taxes. And most of all, it necessitates taking an abundance mindset — leveraging higher earnings not for consumption, but for strategically building productive asset portfolios.

For those able to embrace this wealth consciousness, even a well-above-average income is merely the seed capital enabling long-term financial prosperity. Squander it on an extravagant lifestyle alone, and you’ve already lost the game before it’s truly begun. The choice for today’s high earners is clear: chase wealth, or chase your tail?

Thanks for reading! I hope this article gave you food for thought on the money trends affecting Gen Z and Millennials. Subscribe to me on Medium, Substack, or X to keep the conversation going.

Disclaimer: This article is for informational and educational purposes only. It should not be construed as professional financial advice. The author and publisher are not responsible or liable for any loss, damage, or issues that may arise from following the advice in this article. Please conduct your research and consult a certified financial advisor before making any major financial decisions. All information presented is general and not tailored to any specific individual’s situation. Past performance is no guarantee of future results.