Why $20,000 is Flying Out of Our Account This Month

I Would Not Have Believed You

Had you told me eighteen years ago, when I was a mere thirty-two years of age and had just recently become an economic development professional, that I would be paying/spending/investing over twenty thousand dollars in one single month in August of 2021 during a worldwide pandemic, I would not have believed you. In terms of the spending or the pandemic.

No, this is not some rags-to-riches story. Medium, YouTube, Twitter, and most other sites are rife with stories of those who struck it rich within the period of a few months or years. I am neither rich nor do I have a job that easily affords us to have months where twenty grand flies out of our checking account.

I was a local government employee eighteen years ago, as I am now, but we barely had two nickels to rub together back then. Our daughter had just been born, our son was five years old, and my wife was a stay-at-home mom.

We are not wealthy yet but are blessed to possess the funds to absorb months like this a few times per year primarily due to my years of grinding away, setting aside funds for such costs, and being at least a bit frugal for a good number of years.

Also, I readily admit that the number of twenty thousand may sound impressive to most middle-of-the-pack middle-class families like my own (not upper-middle-class by all accounts), but I know numerous people for whom that amount would not be anything out of the ordinary. Perhaps even a very low-spending month.

But I did feel compelled to share this to help ease the Pain of Paying that I am feeling right about now as it seems that all my bills are coming due simultaneously.

But another totally different viewpoint, say that of my younger brother, is that the world is a place of abundance and that I am highly privileged to pay those kinds of things.

Without further ado, when I share seven of the myriad ways that I am spending or paying such a high amount this month, you may find it quite reasonable.

Our Daughter’s School

Well-worthy of an upcoming story on its own, our daughter rapidly went from Ivy League material to not so much during the pandemic. Because I will divulge my name in the coming years, I do not wish to share too many details, but the gist of it is that she started community college this week.

After enduring thirty thousand points of pain for four years with our son, who will soon be embarking on his graduate school career, which I will detail soon, the community college tuition is of tremendous value.

Not only will she continue living with my wife and me for the next year or two, saving thousands of dollars, but her first-semester tuition was less than the monthly bill for our son’s undergrad and now less than his graduate program.

Furthermore, the school charged us exactly what they said it would, unlike our son’s current graduate school and unlike the price creep that his undergraduate institution does year after year.

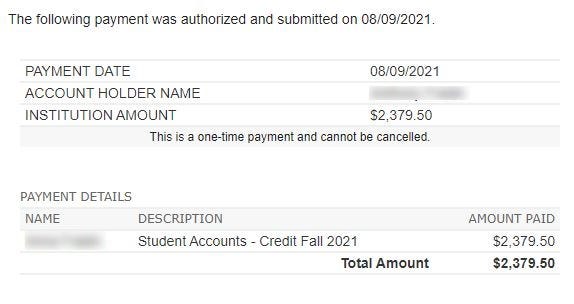

The $2,379 that I charged to my credit card a few weeks ago is an extremely fair deal in my book and an expense that I am pleased to pay. Do not tell anyone, but I now have over $130,000 stashed in her college accounts and am not even using any of those funds for this. Next year, I will likely begin claiming the tax credit to offset some of the tax burdens that we are likely to owe next spring.

I intend to pay the entire balance of my credit card off next month, as always, despite this and many other charges adding up to well over $5,000.

I will likely go to the bookstore with her, as well, since she can hardly claim to be me with my credit card in hand, so it is a fair assumption that her four classes will result in several hundred dollars worth of books. I’ve been to this rodeo before.

Over $7,000 in Automotive Expenses

As per my verbal agreement with our daughter, I told her that I would buy her a car if she stayed at home for at least a year and attended community college.

This past Saturday morning as I was trying to relax a bit around 9 AM and sip some coffee with my wife, she called me on it.

I’ll skip the long story, but between the three of us (not counting my son), my wife, daughter, and I usually had to be at various places at the same time, thus my wife and daughter were sharing the privilege of driving me to and from work several times per week for the past three or four weeks.

When she reminded me that it would be impossible for her to continue driving me to work every Monday and Friday (I typically work from home on Wednesdays) due to having an 8 AM class, I felt that the time was right.

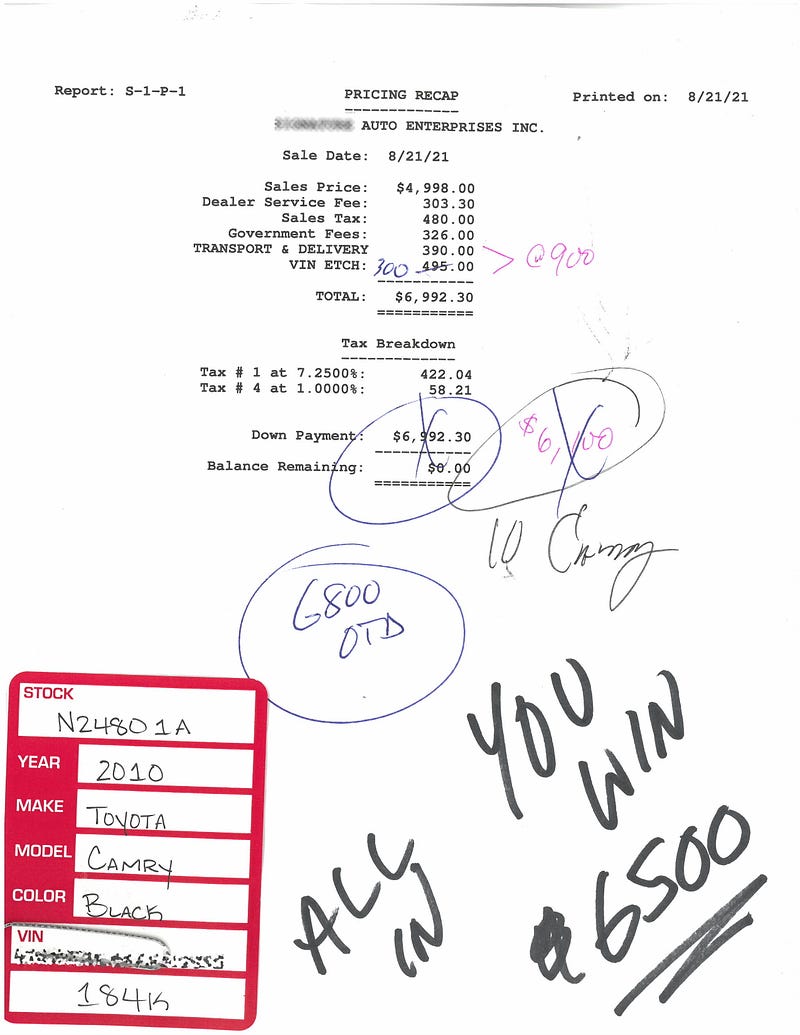

Below is the pricing recap that I will leave you to figure out, but the bottom line is that I paid $6,300, one thousand on my credit card (the maximum they would allow me to charge without a 3% fee) and stroked a check for the remaining $5,300, putting me ahead of a couple that was interested in the same vehicle, but had to seek financing.

Perhaps one time when my cash reserves helped out a bit.

Of course, besides the $6,300 that I shelled out on the 21st, I went ahead and ordered a new key fob made from Ace Hardware, at a cost of $200-plus, and my wife thought it wise to pay for the first six months of insurance, which came out to another $350-plus. Both costs were charged to my credit card.

While thinking about this, I nearly forgot about our automatic $436 monthly payment to purchase my wife’s 2019 Subaru Outback off of the lease.

If you care to add incidentals like the gas for our cars and whatnot, I have likely spent about $7,500 on vehicles this month.

My daughter loves the car even though it has more miles on it already than any car that anyone in our family has ever owned — 184,000. But I will state here for the world to read that if we get at least two years out of it without spending thousands more on repairs, I will be okay with that.

Our Son’s School

My son and I are quite bitter about the University of Denver.

Another long story on its own, they sold us a bill of goods.

Someone from the school quoted him one price, but when his registration was done and the tuition coming due, the price was different.

Care to guess if it costs more or less than what they quoted?

That is a joke, of course.

Never in the history of the college industrial complex has the bill come out to be less than what the student/customer thought. If it even comes within a few hundred, consider that a blessing.

Even after paying nearly a hundred and twenty grand for our son’s undergraduate degree, I still have a few bucks in his college account.

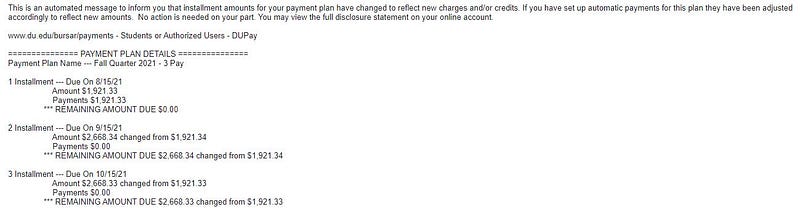

When the quote for his first year of graduate tuition was in the $17,000 range, after a generous $22,000 academic scholarship, I readily agreed to pay it and thought that we might even have a few dollars left after the year. All other living costs are on him.

But when the bill came due after he completed his registration, you can see that the first out of three quarters will cost over $7,200 for tuition alone. It does not take a math genius to figure that his tuition, even after a scholarship, will be about $22,000 — exactly half of the “book price” and $4,000 more than the estimate from early this year when he was accepted.

Not only am I pissed about this, but my son is, too.

But it is what it is. Next week we will be flying out there together to move him into his new apartment with three other roommates, including one who is years past graduation and has a “job” selling marijuana. Another one is a law student, so hopefully, at least he will be a tad bit legit.

Whatever the case may be, I transferred just under $2,000 from our checking account to DU this week, with many higher payments to come. The typical payment that I make to them for the next eight months will each be higher than our daughter’s semester.

Denver is far

None of the four of us had ever set foot in the State of Colorado until a few months ago when my son and I spent a few days there for him to meet with the school and for us to find an apartment.

Having lived in the Chicago area my entire life, and his too, we must fly and lodge somewhere when we head to Denver. Our son just did get his license, but he is not much of a driver yet. And I have never been the kind of guy who wants to drive a thousand miles including half of it through the desert and mountains.

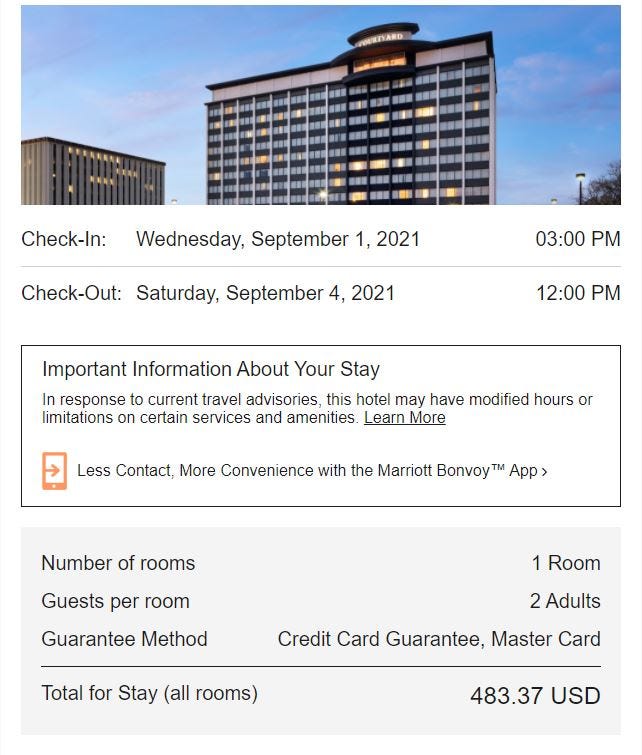

Even though we got a great deal flying to Denver from Chicago next week, only about $150 for both of us, I am also flying back. After having had a horrendous stay at the Holiday Inn Express in downtown Denver in late May, I stepped up our lodging a bit.

Flying to and from Denver, lodging at the Marriott in Cherry Creek, transportation and food while there and all the other costs associated with moving him in will likely add another $1,200 to $1,500 to my credit card this month.

My wife also bought our son a nice new luggage set, since ours has seen better days and he will be traveling more. Oh well, another $250 or so on my credit card from Amazon.

But his luggage is nice.

Our wannabe jet setter

Our family’s income is far too low for our daughter’s taste.

I do not mean to sound snarky, but all of her friends come from families that purchased Pools and RVs and spent the bulk of the past two years on vacation since both of their parents, or at least the fathers, worked from wherever they were at the time. Two of them purchased second homes — both in Tennessee for whatever that’s worth.

Her FOMO is setting in as her three best friends all left home for school the past few weeks. The good news is that two of them are within driving distance and should be home every so often — one is attending Bradley University in Peoria, Illinois and another is now attending the University of Wisconsin at Milwaukee.

But her BFF since she was just a little four-year-old now attends San Diego State.

So would you believe that this week, our eighteen-year-old daughter purchased airplane tickets, paid for an Airbnb, and her friend bought tickets for them to go to the Chase Atlantic concert in San Diego on October 12th? The round-trip airfare via American was a great deal at about $250 and two nights staying in someone’s home is around $200.

Both the airline tickets and the AirBnB are on my credit card, as I insisted, but she will ultimately pay me back in some way, shape, or form.

As I told her today upon giving her my credit card number, I know where she lives!

Our Regular Life Costs Around $7,000 per month

I do not want to bore anyone, but besides initiating tuition payments, paying for a new car, an additional key for it, and insurance, airfare, and lodging for Denver and San Diego, we still have our normal expenses.

We eat out a lot. My wife spends a lot on groceries. We still have a mortgage to pay, and August is when our homeowner’s insurance is due every year, so that was another $500 or so on my credit card for the six-month installment.

To make matters even worse, the very same day that I spent three hours purchasing a car and then taking it to Ace Hardware to get another key cut, the mail for the day included my wife’s credit card bill ($1,000), her Kohl’s bill ($70) and a $2,666 bill for the second installment of our property taxes.

I did not mention that late last month, my wife and daughter went for a much-needed two day “girls getaway” in northern Illinois, which helped lead to her $1,000 credit card bill, and earlier this month, I took my daughter for a much-needed two-day jaunt to the Starved Rock area, which helped contribute about $800 or so out of the $20,000 in spending this month.

It’s enough to make a grown man weep!

The very best $48 that I spent was this past Sunday when after mowing our large lot for nearly two hours, I treated my sore body to an hour-long foot massage. I go to what my daughter would call a sus business, but I assure you that it is on the up-and-up. A sixty-minute basic massage goes for $30, and I typically tip between $18 and $20.

…And I Am Still Paying a Most Important Bill

Despite feeling somewhat overwhelmed by our family’s high expenditures this month, the moral that you can take from this is that I continued to pay our most important bill of all — to us.

Consider me the “Pay Yourself First” guy and I strive to do just that come Hell or high water, both of which seem to be plaguing our country at present.

After fully funding my IRA the easy way this year, I have now shifted towards contributing $250 every week to my budding Fundrise account.

Having come across an interesting article about how forty percent of families in our low six-figure income bracket are still living paycheck-to-paycheck and reading a story by Rocco Pendola today chastising those who do, I continued resolving to not fall back into that trap.

Sure, our checking account balance is rapidly plummeting from around $27,000 down to around $12,000 from early August through early September, which causes me some measure of anxiety. It does not take a math whiz to determine that level of spending more than you make is not sustainable.

But that has occurred before and has lowered our account to much lower than twelve thousand. Also, included in that big spending and paying month for us is $500 contributed to my wife’s IRA and another $1,000 into my Fundrise account.

When all is said and done, I can feel okay about this high spending month. I resolved long ago to pay for our children’s education, so that is what I will do. I do it gladly, too, but feel better about it when I share with others. It is no easy feat to do on one salary alone, along with our myriad other expenses.

I do not wish to become one of the six-figure earners living to paycheck. Rather, my goal is to increase my income by several things that I already do, like selling my long-ago written eBook about my experiences as a probation officer in Cook County, which nets me only a few hundred bucks per year.

Likewise, I only net a few hundred bucks per year with all of these long stories that I post to Medium, as well as some very short ones that I write for Two Minute Madness.

The investments that I have made for my family’s and my own behalf now gather over ten thousand dollars most years in dividends and capital gains, including my favorite twelve thousand this past December alone.

So to wrap this all up, I urge you to pay yourself first too, whether it is only twenty dollars on your next payday or twenty thousand dollars when you sell an NFT or make thousands off of your writing or products.

It will give you some peace of mind, like I am striving for, during those months like I am having when all of your bills and expenses come due all at once.