Investment Advice

When to Invest in RRSPs to Boost Your Future Savings

A guide to the key benefits of investing in an RRSP

A common question I hear among young professionals is when is the right time to start contributing to a Registered Retirement Savings Plan (RRSP).

The best time to invest in an RRSP isn’t an equation that fits everyone — it’s more about matching your circumstances.

The key is to understand your financial situation along with your retirement goals to help start your RRSP journey. From assessing your current financial situation to anticipating future income to determining your retirement goals, everything plays a role in determining the best time to make an RRSP contribution.

Let’s go through the specifics to find out when it is the best fit for your RRSP investment strategy.

Early Career Initiation

Starting your RRSP contributions early comes with a clear advantage due to impressive compound interest. This financial magic happens when your investments generate income, which in turn generates more income. Starting early, even with a small contribution, gives your money more time to grow.

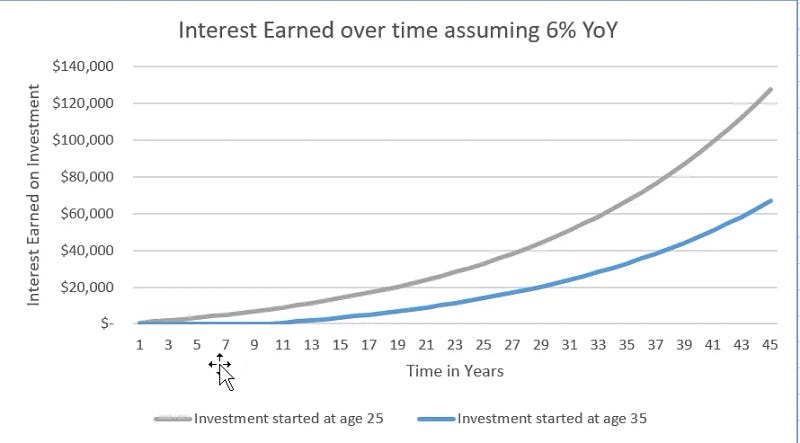

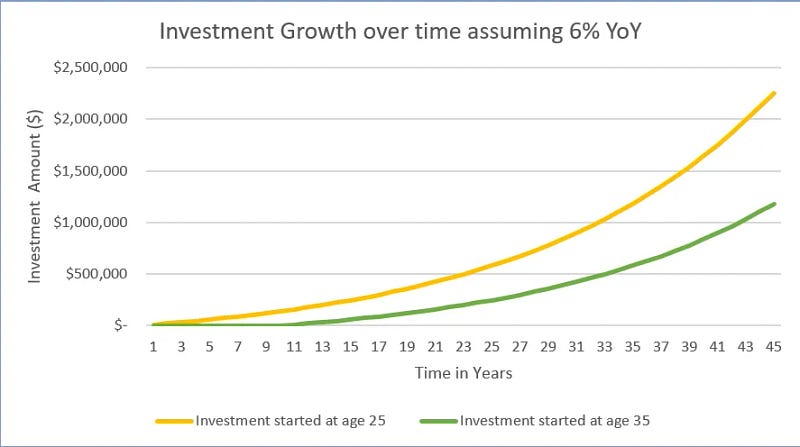

For example, consider a person who invests $10,000 per year from age 25 and another person who invests the same amount per year from age 35. Despite contributing the same total amount, a person who starts at 25 can accumulate more because of their long-term investment.

This example illustrates the huge benefits of starting RRSP contributions early, showing how time can be your strongest ally in building a great retirement fund.

Starting at ages 25 and 35, a $10,000 annual deposit earns $127,626 and $66,861 in interest annually, respectively. If someone retires at age 65, the total investment value will reach $2.25 million and $1.18 million, respectively. This illustration illustrates how delaying investment can significantly reduce potential income.

Immediate Tax Benefits

When you contribute to an RRSP, you open the door to potential tax benefits. Contributions to an RRSP are considered a deduction from your taxable income. This deduction reduces the taxable portion of your income, which ultimately reduces your overall tax liability.

For high-income earners, this tax deferral can result in significant savings. Investing in an RRSP not only secures your future by increasing your retirement savings but also provides an immediate beneficial impact by potentially reducing your expenses today. It’s like a double win — building your financial security for tomorrow and potentially reducing your taxes today.

Debt Management Consideration

It may be wise to take a closer look at high-interest loans before committing to an RRSP investment. High-interest debt can grow quickly and can mask returns on investments.

Paying off these loans can be a smart move, as it frees up your finances and sets a more solid foundation for RRSP contributions. By cutting high-interest debt first, you are essentially eliminating financial burdens that can hinder your progress toward retirement savings.

This approach not only creates a stable financial environment but also sets you up to contribute meaningfully and easily to your RRSP in the future, setting the stage for a secure and prosperous retirement.

Tax Bracket Optimization

Matching your RRSP contributions to years of high earnings can be a smart move to maximize tax benefits.

Do you forecast income growth, which I believe would be?

Consider deferring the contribution until you are in a higher tax bracket.

Why?

Because if you contribute during these high-income years, the tax deductions are substantial.

By strategically timing your RRSP with multi-year increases, you can make the most of the tax advantages.

This way, you optimize the deductions, which can reduce your taxable income in the years you earn more.

It’s a strategic approach that not only helps you build your retirement savings but also makes the most of the tax benefits offered by RRSPs.

Age and Retirement Proximity

Increasing your RRSP contributions becomes increasingly important as you approach retirement. Investing heavily in RRSPs, especially during those peak pre-retirement income years, can significantly increase your retirement savings.

The goal of this focused effort is to have a more comfortable life after retirement. By channeling more into your RRSP during these crucial years, you’re essentially turbocharging your retirement funds, ensuring there’s a bigger nest egg to count on when you say goodbye to the workforce.

This strategic increase in RRSP contributions during retirement is a last-minute boost to your financial security, allowing you to enjoy a more fulfilling and stress-free phase of retirement.

While there’s no definitive answer to the “right time” to invest in an RRSP, the early years of your career often present a lucrative window due to the long-term benefits of accumulated interest; therefore, the best time to invest in an RRSP depends on your financial situation and aspirations.

Your current financial situation, existing debt, future income expectations, and retirement goals should all be weighed before moving into an RRSP contribution.

Paying attention to your financial health, assessing where you stand on the cost and income metrics, and considering your retirement dreams are important steps in the decision-making process when investing in an RRSP.

I suggest you consult with a financial advisor who can provide you with relevant insights tailored to your circumstances.

Financial advisors can provide detailed guidance on when and how much to invest in an RRSP that matches your specific financial goals.

Recommended Reads

More From The Canadian Way