The 2 Worst Bear Markets Of All Time

The 2020 crash might only be the warmup act of a deeper bear market

Twice before in history, worldwide markets have experienced a sharp, deep, unexpected sell-off (like we experience in 2020), a rally, and finally a much deeper, multi-year bear market and economic depression.

The world appears to be on the precipice again.

Governments and central banks are trying to spend their way out of the current recession without triggering runaway inflation. Based on recent stock market action, it appears investors don’t believe the balancing act is going well.

Today, we will explore the financial shocks that preceded the two worst bear markets of all time and what the 2020 stock market crash might be predicting for 2021 and beyond. In this article;

- The two worst bear markets of all time

- Today’s conflicting economic indicators

- The problem with Modern Monetary Theory

- Final thoughts

The two worst bear markets of all time

The Great Depression

There is still uncertainty about what triggered the 1929 stock market crash but do know about financial conditions leading up to the crash.

Germany lost WWI. Germany owed a lot of money to the US, France, and the UK. Germany couldn’t pay what it owed because Germany had also been bombed back to the stone age. America had an idea — invest in and rebuild Germany so Germany could pay back all the money it owed to everyone.

Between 1924 and 1929, the US economy exploded. In fact, there was such an economic boom from the rebuilding of Europe, we now refer to the era as the ‘Roaring 20s’. I’m oversimplifying the story, so if you’d like to learn more about the Roaring 20s, please read my previous article on the subject.

Europe eventually did rebuild. By the end of the 1920s, Europe really didn’t need to rely on American machinery, building supplies, and agricultural products. By the end of the 1920s, Europe had recovered enough to provide most of these things by themselves.

Throughout the mid to late 1920s boom, Americans had flocked to the cities in search of better jobs. By 1929, Europe started buying a lot fewer American products. A slow down in purchasing, combined with bumper crops in America and Europe suddenly created a massive oversupply problem. Wheat prices dropped suddenly. The stock market followed by September of 1929.

What many people forget, is that although the 1929 stock market crash was sharp, deep, and very sudden (like the crash in 2020), there was a very significant rebound before the stock market finally reversed and continued falling until the summer of 1932. I’m oversimplifying the story, so if you’d like to learn more about the stock market crash of 1929 and the subsequent bull trap that formed, please read my previous article on the subject.

Monetarist economists believe the Great Depression ended up being a much worse recession than it needed to be because the Federal Reserve failed to take a big enough corrective action early in the recession.

‘Friedman and Schwartz argue that people wanted to hold more money than the Federal Reserve was supplying. As a result, people hoarded money by consuming less. This caused a contraction in employment and production since prices were not flexible enough to immediately fall. The Fed’s failure was in not realizing what was happening and not taking corrective action.’— Wikipedia

Keynesian economists think the Great Depression might have been sparked by businesses anticipating a long-term downturn in consumption. In response, businesses would naturally invest less in future production, causing the recession to worsen. Keynes thought governments should have spent more money, which in theory should have kept unemployment rates significantly lower, thereby lessening the depth of the Great Depression.

‘Keynes argued that if the national government spent more money to help the economy to recover the money normally spent by consumers and business firms, then unemployment rates would fall. The solution was for the Federal Reserve System to “create new money for the national government to borrow and spend” and to cut taxes rather than raising them, in order for consumers to spend more, and other beneficial factors.’ — Wikipedia

Unfortunately, the Federal Reserve did not react quickly in 1930–31 and the government opted to raise taxes in an attempt to offset government income shortfalls.

The lesson learned from the Great Depression was that central banks need to loosen money supply and national governments should borrow and spend to make up for the loss of consumer and business spending and investment.

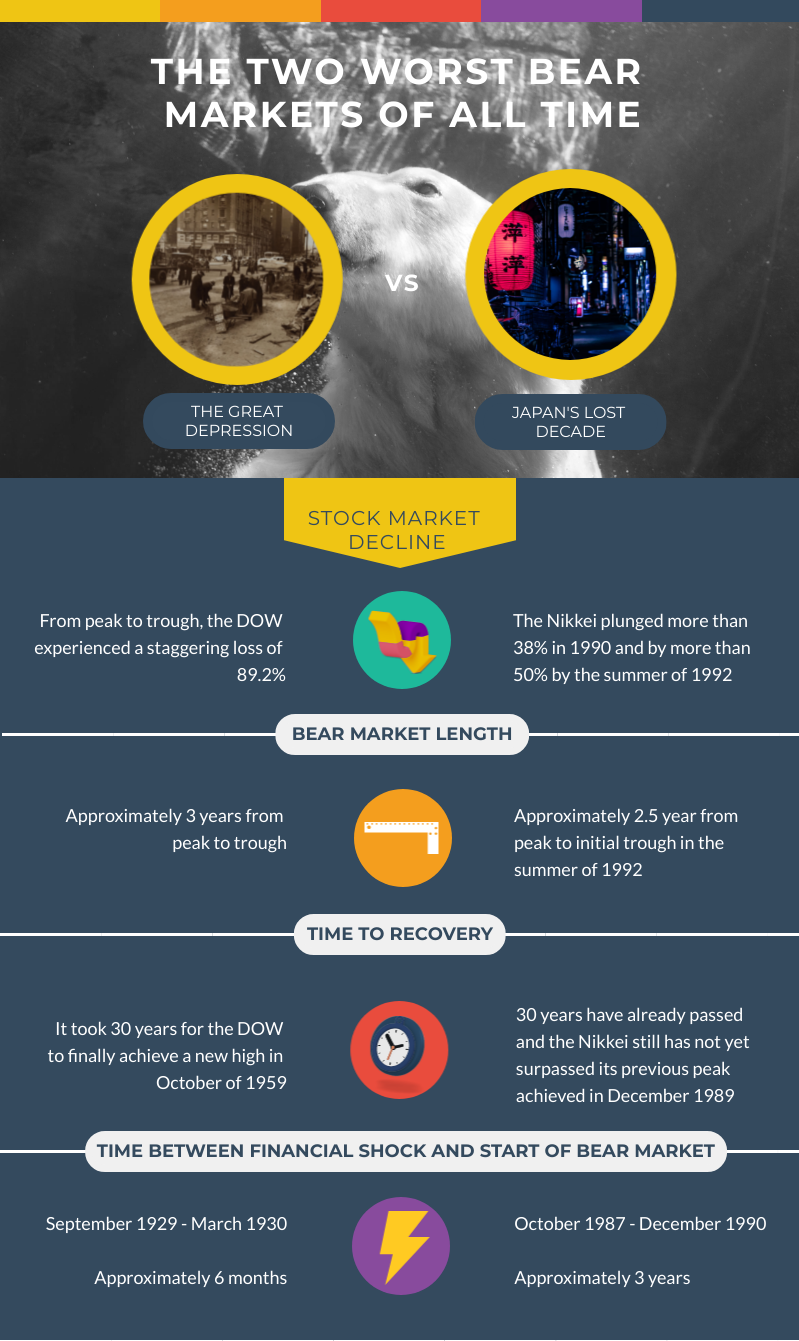

It took 30 years for the DOW to recover from the Great Recession and finally achieve a new record high, in October of 1959.

Fast forward 60 years …

Japan’s ‘Lost Decade’

Japan suffered a short and relatively shallow recession in 1985–1986. Using lessons learned from the Great Depression, the Bank of Japan (BOJ) lowered interest rates and adopted a much looser monetary policy stance. By 1987, Japan was coming out of the recession. The BOJ expressed concern over asset inflation and signaled the possibility of a monetary tightening policy in the summer of 1987.

October 1987, Japan experienced ‘Blue Tuesday’. (In North America, the same event is known as Black Monday). Again, there’s no consensus on what caused this short, sharp, stock market crash. However, the event convinced the Bank of Japan to keep monetary policy very loose and interest rates very low until December of 1989.

A combination of virtually unlimited credit expansion and uncontrolled money supply resulted in rapidly increasing asset prices and excessive economic activity. Land prices went through the roof and stock prices exploded. I’m oversimplifying the story, so if you’d like to learn more about Japan’s Bubble Economy and the subsequent bear market, please read my previous article on the subject.

The BOJ finally started to tighten monetary policy by hiking the official discount rate from 2.5% to 4.25% by late December 1989. The rate hike did little to slow property and stock market speculation.

The BOJ continued to tighten monetary policy in early 1990 by pushing the official discount rate from 4.25% to 6.00%. This time, investors took notice. By the end of 1990, the Nikkei had fallen 35%. Thirty years have already passed and the Nikkei still has not yet surpassed its previous peak achieved in December 1989.

The lesson learned from Japan’s Bubble Economy was that central banks need to loosen the money supply and national governments should borrow and spend to make up for the loss of consumer and business spending and investment.

However, interest rates should be increased before excess speculation takes hold. If too large a bubble is allowed to form and inflation starts taking off, putting the brakes on monetary policy or sudden interest rate hikes can also cause a real estate and stock market crash of epic proportions.

Today’s conflicting economic indicators

The jobs report came out last Friday. It wasn’t good. It suggests hiring is slowing down. Some argue the weak jobs numbers reported last week suggests the economy is cooling down already and more stimulus is required. However, we are also seeing signs major employers like McDonald’s, are being forced to increase salaries — a potential leading indicator of a wage-price spiral.

Stock markets responded to all the news with high-growth technology stocks selling off this week and commodities continuing to rally strongly — an indicator suggesting investors believe inflation pressures are mounting.

Canada and the UK have already tapped the brakes on monetary stimulus, while New Zealand and Australia are seriously considering the same. Yet the Federal Reserve has made it clear they intend to get unemployment down to near-record lows before trying to taper monetary stimulus. Jerome Powell insists the inflation the world is currently experiencing in everything from car rentals to computer chips will be temporary – or ‘transitory’ in the words of Mr. Powell.

But will inflationary pressures remain transitory?

For example, if the price of computer chips is temporarily increased, then chip output should naturally increase, eventually meeting demand. Subsequently, computer chip prices should normalize, right?

Not necessarily.

Warren Buffett thinks the economy is already, ‘red hot’. Warren pointed out at the 2021 Berkshire Hathaway annual shareholders meeting that higher input costs are already causing ‘very substantial inflation’ and those rising costs are being accepted by consumers.

One thing all consumers know – once higher input costs are successfully passed on to consumers, manufacturers don’t lower prices unless consumers stop buying.

Modern Monetary Theory

Compounding the debate over when to tighten monetary policy is the relatively new concept of Modern Monetary Theory (MMT).

While many of us think of government spending and taxation a little like how we handle our own mortgages and checking accounts at home, proponents of MMT say we are wrong to think of it this way. At the risk of over-simplification, MMT suggests government debt is simply money put into the economy by the government that hasn’t been taxed back … yet.

Traditional economic theory suggests too much debt inevitably leads to inflation as a country’s currency gets devalued by excess money printing. MMT supporters argue this idea is outdated. They point to Japan’s staggering debt level as an example of sustainable government debt and deficit spending. The key to making MMT work is simply ensuring inflation remains low and interest rates remain near zero. At least, in theory, this could be accomplished by raising tax rates to cool the economy rather than increasing interest rates.

America’s apparent ever-increasing reliance on MMT is causing a shift away from traditional economic indicators economists have used in the past to predict inflation. This means that if MMT is wrong, inflation could get far ahead of the Federal Reserve before there is any action to counter it. Like the Bank of Japan in 1990, The Federal Reserve might be forced to raise interest rates faster than they would like, potentially triggering another stock, cryptocurrency, and real estate market crash.

“Meanwhile — as part of a profound shift in economic thinking that’s gathered pace in the past year — a whole range of other indicators once relied on to flag trouble ahead are falling out of favor. Abandoning or downplaying all of these yardsticks means officials are less likely to take the kind of pre-emptive action that’s choked off expansions in the past.” — Ben Holland at Bloomberg

If, on the other hand, MMT turns out to be right — great, I guess problem solved. However, whether you are a believer in MMT or not, I would like to point out one Achilles heel that even most MMT supporters agree with;

According to MMT, the only limit the government has when it comes to spending is the availability of real resources, like workers, construction supplies, etc. When government spending is too great with respect to the resources available, inflation can surge if decision-makers are not careful. — Investopedia

Sounds great to me. In other words, MMT suggests inflation will be transitory as long as governments can;

- figure out a way to relieve supply chain bottlenecks caused by the ongoing pandemic,

- get people to go back to low-paying jobs (thereby avoiding a significant wage-price spiral),

- and reverse the sudden commodities spike in everything from cattle to copper,

- while simultaneously spending trillions of dollars on infrastructure and job creation projects.

Does that sound simple to you?

Final thoughts

Let’s review –

The Biden administration and the Federal Reserve are counting on MMT to allow monetary policy to remain loose and infrastructure spending high in order to pull the economy out of the worst recession since the Great Depression.

The problem is, agriculture products, raw resources, labor, and construction supplies, are all rising rapidly in price.

If the premise that inflationary pressures are transitory is wrong, we could be in for a whole new round of hurt.

Technology stocks have corrected a lot but mega-cap tech valuations remain sky-high. I’m not advocating investors sell all their technology stocks and load up on commodities. Far from it. Technology stocks will continue to remain an important investment sector over the long term and history shows us time and time again, commodities tend to sell off in a prolonged bear market as rapidly as stocks do.

Investors should be on high alert.

The selloff in MEME and technology stocks suggests the worst of the ‘everything bubble’ might be past us but most stocks continue to look very overvalued. If central banks slowly take their foot off the gas, hopefully, prices can deflate in an orderly manner.

However, if the Federal Reserve and the Biden administration insist on juicing the US economy, the chances of seeing a return to runaway stock prices and potentially, runaway inflation could rise quickly.

In my humble opinion, the biggest risk of all is a situation where inflation suddenly takes off and central banks are forced to slam on the monetary policy brakes (as Japan did decades ago).

If this happens, it will be absolutely devastating for the stock market and the economy as investors lose faith in the system and cash out whatever stocks they have left. Worst of all, investors could become so disillusioned with the stock market (in the same way investors did in the US in the 1930s and Japan in the 1990s) that they remain out of the stock market, perhaps for many years.

Stay calm, stay vigilant, diversify, rebalance.