What To Watch For In Financial Markets In 2024

Bonds, cash, and no more inflation?

(Not intended to be investment advice, opinions are my own.)

A new year is almost upon us. So now is as good a time as any to take a look at our portfolios and the investment landscape to make sure that we’re positioned optimally for the long run.

Bonds and cash not trash

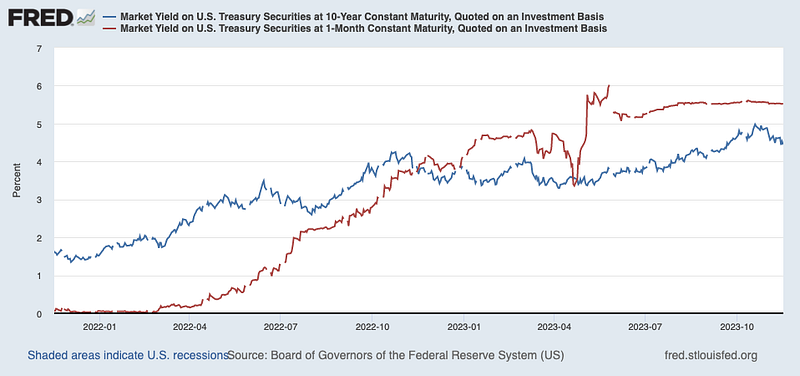

A few big things are different now versus a year ago. First bonds pay a lot more than they used to. So does cash. For the first time in a while, it looks like you can earn a positive real return investing in both Treasury bonds and money market funds as inflation seems to have leveled off (the most recent inflation print was 3.2%).

This adds an unfamiliar wrinkle to portfolio strategy. Bonds and cash are no longer trash. Perhaps they can once again offer both robust risk adjusted returns and diversification. Of the two bonds are more interesting as they’re a way to lock in today’s higher rates for years to come (cash yields will quickly dip if the Fed lowers rates).

In the short run, the diversification part remains to be seen. There’s still very much a “will they or won’t they” attitude towards the Fed where stocks and bonds seem to whip up and down with every change in expectations around whether the Fed will lower rates soon or not. The recent rally has been driven by increased hopes that the time of rising rates is firmly behind us and that we might even see a rate decrease or two. The dip that preceded this rally was caused by the opposite — fears of higher rates (plus shock at how quickly longer duration yields were rising) pushed down prices of both stocks and bonds.

No more inflation?

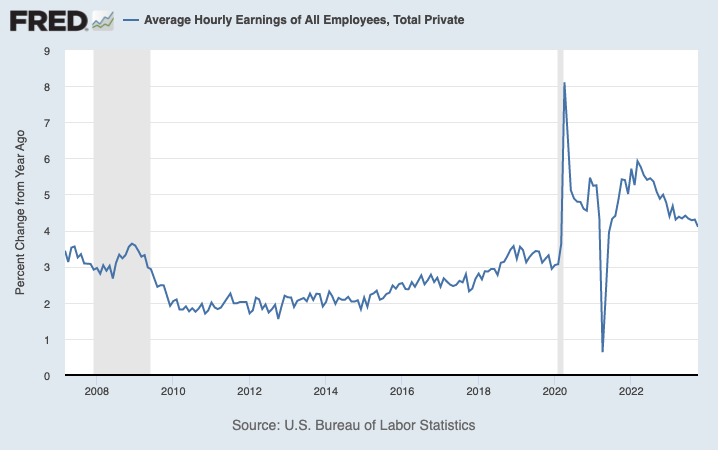

The inflation bogey man seems to have been slain. A big tell is that wage growth has slowed significantly from the post-pandemic high inflation days, dropping from 6% to 4%.

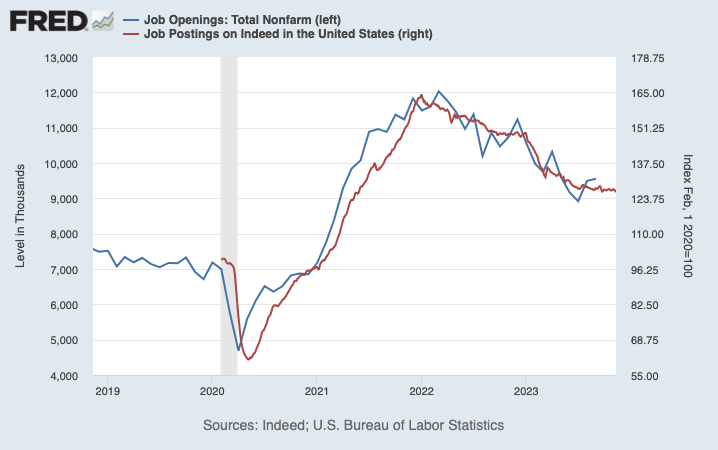

The demand for workers seems to be cooling somewhat as well with multiple indicators showing fewer job openings — this coupled with the layoffs at the start of 2023 mean there are fewer opportunities to job hop (and less leeway to negotiate for higher wages).

While it’s highly unfortunate that it’s rank and file workers that were once again sacrificed (via layoffs and negative real wage growth) to stop inflation, it does seem like the Fed has engineered a soft landing, especially relative to other major economies. Whether through foresight or sheer dumb luck, the U.S. economy is looking particularly strong versus those of China, Japan, and the Euro Area.

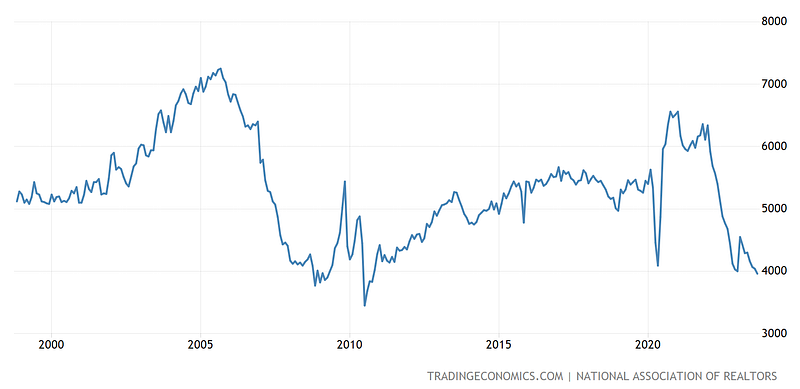

More room to fall in real estate?

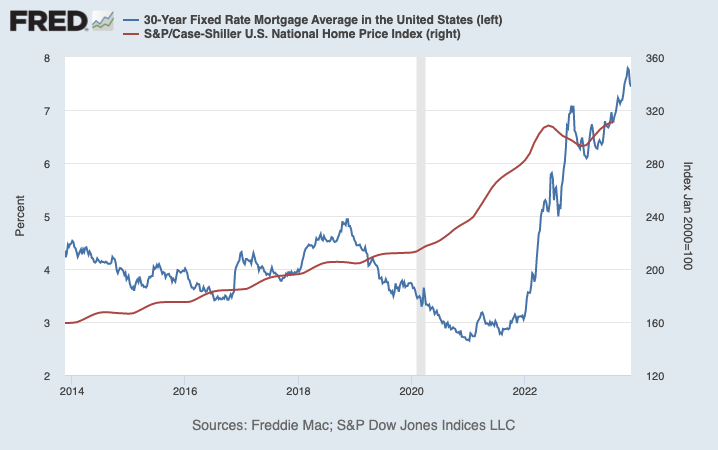

Real estate prices have remained stubbornly high in the face of record rises in mortgage rates. A big reason why is that more than a decade of super low rates have allowed borrowers to lock in cheap mortgage rates — thus, while they might not be able to afford that new bigger house, they’re also in no rush to sell as they can easily afford their current home payments.

This means that while home prices might look stable on the surface, deeper down there’s been a plunge in activity as would-be sellers refuse to sell (because they refuse to swap their current low rate mortgages for higher rate ones) and would-be buyers can’t afford to buy (because market rates are so high).

That implies two things:

- If something like a sudden increase in unemployment were to force more supply (i.e. sellers coming to the market), at current mortgage rates and prices, there would be a large supply-demand mismatch — meaning prices would need to come down significantly to attract more demand.

- If rates were to come down, all that pent up demand (i.e. buyers that would love to buy if only mortgage rates were lower) would rush back into the market, possibly causing another surge in prices.

The Fed is surely aware of this and I would hope realizes the importance of not inflating another housing bubble as that would undo much of what they’ve just done to contain inflation. At the same time, the flip side implies the possibility of a negative feedback loop between jobs, home prices, and possibly even bank balance sheets where a spike in job losses could kick off forced sales and more job losses.

So soft landing for now — but we must tread with caution.