What Is The Best Health Insurance Plan If You Are Self-Employed?

Are you a business owner or self-employed person? Or looking to start your own business?

Freelancer? Private clinician? Boutique lawyer owner? Digital content creator?

Have a lot of questions about insurance for business owners?

I got you. A-Z, full concierge health insurance expert here at your service!

Can’t read the full article? Join Medium as a member here to read all my articles on this platform.

My mission has always been to help the middle man/woman or 1099 community navigate their way around health insurance. I specialize in helping small business owners and self-employed people with this, and I clearly speak to many of them about health insurance options, all day every day.

Many self-employed business people who want affordable and quality healthcare fall into the black hole abyss of overpriced, underwhelming and downright confusing coverage options. Or if they haven’t already fallen into that trap, they’re afraid to do so and oftentimes end up forgoing health insurance altogether.

And I’m here to help with all that!

I’ve gathered the questions I frequently get asked and have compiled an easy guide for you to answer all your self-employed health insurance needs.

What factors to consider for a health insurance plan?

When you take the plunge from a 9-to-5 job with benefits to full-time freelancing, you might not know where to turn.

Especially with health insurance benefits.

Do you even know what you need for your self-employed health insurance?

Here are some factors to consider:

- Premium Amount — can I comfortably afford this every month?

- Deductible — Do I typically spend this much on medical expenses annually? Can I meet my deductible in the event of an emergency?

- Network — Do the doctors I like to go to accept this plan? Is the nearest emergency room IN NETWORK?

Not sure about other terms in the healthcare marketplace? Read this list to help you navigate better!

What health insurance options do you have?

The options are largely divided into public and private market plans. Understanding first which market to shop in is key because tons of carriers participate in each market!

Once you've started on your journey of self-employment, you know there’s a big range in income.

You’re different when you start and you’re different when you’re in mid-career, or even when you take your hands-off, hire people, and let them do all your work.

You have different needs at every stage of your business.

Many variables make health insurance so daunting and difficult. Not only is it your individual perspective at the stage of your business, but insurance is also governed by state laws. Different factors go into the insurance options in your state. There are so many things to read up on!

I’m a 2–15 licensed professional. I’ve taken all the tests and I understand the ins and outs of it.

How can I help with this? My role is to evaluate where you are in your business and advise the best-fit health insurance options for yourself or your employees. It all starts with a simple conversation to assess your situation and risk; then I get to work and do my magic and research and find you a plan that simply works!

For example, Healthcare.gov is a state marketplace where everyone can log on and get a list of plans to shop from.

There’s a stage of business where this is appropriate. There are some pros to this but there are also some cons.

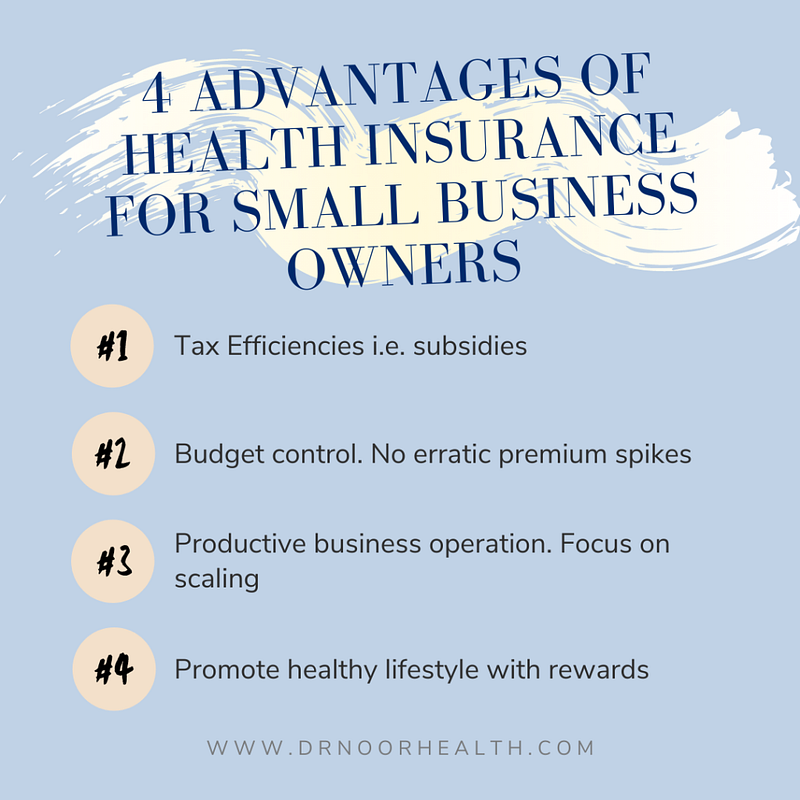

If you’re just starting your business, and your income or revenue hasn’t started rolling, the marketplace is a good place to start. You can get a subsidized plan tied to your income (not to your health!).

Read all the details about picking the right insurance for your small business here.

When you do well in your business, you will no longer qualify for subsidies and your premium is going to skyrocket!

This is when the private market plans come to play and it’ll work much better for you. This one will be tied to your health, not your income!

Listen to more details about this here:

Should you look for a doctor or a healthcare plan first?

It depends on your deal breakers!

If you have a specific doctor you want to see, see what insurance they accept, and ask for a list of estimated out-of-pocket costs.

This can help you decide:

(1) whether they accept a plan you’d want

(2) what it would cost you out of network, should you pick a plan that’s not covered.

My advice is to always stay in-network! It’s never worth it to go out of network on a self-employed health insurance plan. If you love a provider, try to find a plan that they are in-network with to maximize your network discounts and plan benefits.

If you don’t have a specific doctor you want to see, are relatively healthy and care more about cost-saving, then picking the plan first may be best.

Most insurance marketplaces have a search option where you can research doctors and specialists. If that feels overwhelming, let me help.

Can you write off health insurance as an expense?

Yes! If you’re a freelancer paying out of pocket, you can do this.

Hit up your CPA come tax time and ask about the Self-Employed Health Insurance Deduction. If you qualify (i.e. have no other insurance options + have business income), you can deduct 100%. This only applies to federal, state, and local income taxes — not to self-employment taxes.

What about your health insurance for your spouse or your team?

No law directly requires employers to provide health care coverage to their employees. Under the ACA, employers with 50 or more full-time employees (or the equivalent in part-time employees) must provide health insurance to 95% of their full-time employees or pay a penalty to the IRS.

Unfortunately, there isn’t a benefit for micro-businesses to get health insurance. You don’t get a discount just because you’re a business. However, offering health insurance is definitely a benefit to some employees.

Many employers offer fantastic coverage for their employees but rates tend to have an unexpected spike when adding spouses and dependents.

This might be an opportunity to consider creative solutions like split family policies to help reduce the bottom line premiums amounts.

Assess health coverage needs and policy options on the open market as well as employer sponsored options and make a decision that makes sense. It’s alright to change health insurance plans at any time also.

Don’t let health insurance become an afterthought. If you aren’t sure where to look for self-employed health insurance, let a professional help you. Book a 15-minute health insurance consultation with me today.

➡️ Schedule a 15-minute call with me so we can start talking about what you need, at your current stage of freelancing.

➡️ SUBSCRIBE to my YouTube channel for fresh tips on understanding the health insurance industry so you can make the most informed decision.

➡️ ️️www.drnoorhealth.com