Wage Garnishment, Student Loans, Social Security, and Collection Agencies Tricks

The reason why I wrote this article is that many do not know their rights.

For example, one person I met was out of work for two years. When he got a job, he put his first paycheck into his bank, and they took it all.

According to federal laws, this was 100% illegal, but the Collection Agencies know that most people do not know this or know how to fight it. Plus, how are you going to fight if you have no money?

Wage Garnishment:

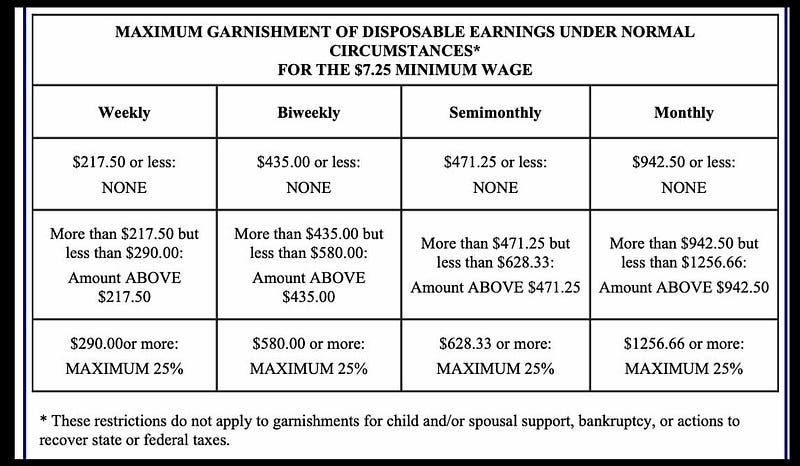

It is illegal for the collection agencies to take more than 25% of your paycheck or 100% of the money in your bank account. However, if the garnishment is for child support, alimony, or taxes, they can take up to 50%.

If you make less than $217.50 per week, no garnishment is permitted other than for taxes, child support, and alimony.

Please see The Debt Collection Improvement Act and The Higher Education Act. Federal laws 31 CFR 212.8., 31 C.F.R. Part 212, and 42 U.S.C. 407(a).

These laws say that they must leave you with enough money to pay your living expenses.

These collection agencies also know that the company you work for probably does not know the law, and this is why they tell the company you work for that they will garnish your wages but do not tell you.

It is not enough for them to only tell the company they must tell you before the garnishment begins, or it is an illegal garnishment.

These collection agencies also know that most banks do not consult with their legal department and just do what the collection agencies ask. These are just the branch of the bank and not the bank’s corporate office.

If your wages are being garnished, and you did not receive a NOTICE in the mail before they started to garnish your wages, then it is an illegal garnishment.

If it is an illegal garnishment, then the Department of Labor will require them to give you all the money they took and may stop future garnishments.

For illegal garnishment, contact the US Department of Labor.

U.S. Department of Labor

Frances Perkins Building

200 Constitution Avenue, NW

Washington, DC 20210

1–866–4- USWAGE (1–866–487–9243).

TTY: 1–866–487–9243

https://www.dol.gov/agencies/whd/wage-garnishment

https://www.dol.gov/agencies/whd/fact-sheets/30-cppa

Garnishing Your Social Security:

Your Social Security cannot be garnished to pay your debts. However, your Social Security can be garnished to pay taxes or child support.

However, there is a loophole that will allow them to garnished your Social Security to pay any debt, including your student loans.

The Loophole:

If you put all of your income into one bank account, including your Social Security, then they can take whatever they want out of that bank account.

However, if you keep your Social Security in a separate account, where no other money is ever deposited into this account except for your Social Security, then they cannot touch your Social Security.

For example, you have one checking account where you have your Social Security directly deposited, and then you find a dollar on the street. You put that dollar into your checking account, and now they can garnish any of the money you put into that checking account.

Thus, you need to have one bank account that is only for your Social Security.

However, you have to have money to open a bank account, and there is no way to prove that the money you used to open the bank account is only from social security.

The solution to stop them from garnishing your Social Security is not to put your Social Security into a bank account. You can ask Social Security to provide you with a debit card.

After you have a bank account that is only for your Social Security, you need to write the bank, the credit card company and tell them that this account is only for your Social Security. As it relates to the following laws, they cannot garnish your Social Security.

Federal laws 31 CFR 212.8., 31 C.F.R. Part 212, and 42 U.S.C. 407(a)

People have done many of these methods, and the garnishments have CONTINUED, and the collections agencies keep calling. All may be illegal, but they know you have no money, so you cannot take them to court. However, if enough people complain, then the U.S. Department of Labor may put a stop to it all.

Garnishment and Student Loans:

For Student Loans, the best way to stop the garnishment is nothing. There is nothing you can do to stop them from garnishing your wages to pay your Student Loans, except change jobs or switch your bank account to another bank.

In the past, you could go into an Income Contingent Repayment Plan (ICRP), and this would stop the garnishment and make you current on your Student Loans.

Now, today, you have to make enough payments to make you current on your Student Loans, and then they will allow you to go into an Income Contingent Repayment Plan (ICRP).

If you do not know what an Income Contingent Repayment Plan (ICRP) is or the benefits, then please see my article called How to Get Rid (Legally) of your Student Loans if you are Poor, on Social Security, or are Retired.

Collection Agencies Tricks:

If you want to stop the creditors from calling, then all you have to do is send them a Certified letter with a Delivery Receipt stating the following words.

A Certified letter with a Delivery Receipt only costs a few extra dollars.

I am executing my rights under the federal law 15 U.S.C. 1692c for you to stop all communications with me, except for the reason set forth under this law. In addition, this letter is NOT an acknowledgment that I owe any debt.

The part that says this letter is NOT an acknowledgment that I owe any debt is very important. Once you state or imply that you owe the debt, the clock is reset to day 1.

For example, you owe a credit card debt, and you have not paid it for 9 years, then in one more year, it will come off your credit report. However, once you state or imply that you owe that debt means that the debt will not come off your credit report for another 10 years.

Just because you sent them this letter does not mean that they will follow the law and stop harassing you. However, with the Delivery Receipt, you got some proof that you did send them the letter. This will be helpful when you report them to the US Department of Labor for harassment.

Another trick that they use is to sue you in court and send you a Summons to show up in court. Once you show up in court, then they can ask where you bank and where you work. Once they have this information, they can take the money directly out of your bank account and garnish your wages.

A lot of people have figured this out and now do not show up for court.

For civil cases such as this, it is not illegal not to show up to court if you received a Summons. For criminal cases, it is illegal not to show up to court if you received a Summons.

If you do not show up to court means that you will automatically lose. This will also reset the clock back to day 1.

These collections agencies are now conducting court by phone. These agencies really want to know where you are working and where your bank is so that they can take money directly out of your bank account and garnish your wages.

If you know you will lose, then when the court calls, do not be home or do not answer the phone.

Previously published in a video here at fyidy.com