Digital Payments

UPI — India’s Way of Secure Digital Payments

It isn’t a Hyperbole that the World smells Innovation in India’s UPI.

Firstly, What’s UPI?

UPI abbreviates to Unified Payments Interface. It is a platform that could link to many bank accounts and enables fast money transfer using IMPS (Immediate Payment Service). However, it needs an app to work. It’s way faster than the previous NEFT (National Electronic Funds Transfer). As it’s online, it’s available 24x7, 365 days.

It’s Origin:

It was launched in 2016 as an initiative by NPCI (National Payments Corporation of India) with support by the RBI (Reserve Bank of India) and the IBA (Indian Banks Association).

Until then, people used to use Mobile Wallets like PayTM, Oxigen, Mobikwik, and Freecharge to recharge, and pay bills. People had to recharge their wallets every now and then to ensure there’s sufficient money inside. It was a tedious task. With the UPI platform, people could recharge and pay bills directly from their bank accounts. The sender need not remember the Receiver’s Bank Account number, IFSC Code, Bank name etc…

How to register for UPI?

To register one’s bank account for UPI, all he needs is:

- A Smart phone with a UPI App installed.

- A Bank account.

- An active SIM card with mobile number registered with the bank.

When you install the app, it prompts you to add a bank account. Choose your bank in the list. Then, an SMS will be sent with some encrypted information to confirm if the Bank account is linked to your Phone number. Then, you’re ready! You can also link multiple bank accounts to one app.

One doesn’t need to apply for KYC, because having a Bank account, he’s already verified as a bonafide citizen.

Ways of Sending money through UPI:

- By Tapping the Receiver’s name in the contact list or by typing his Mobile number. (Both the Users need to have the same UPI App)

- By Scanning his Unique QR Code.

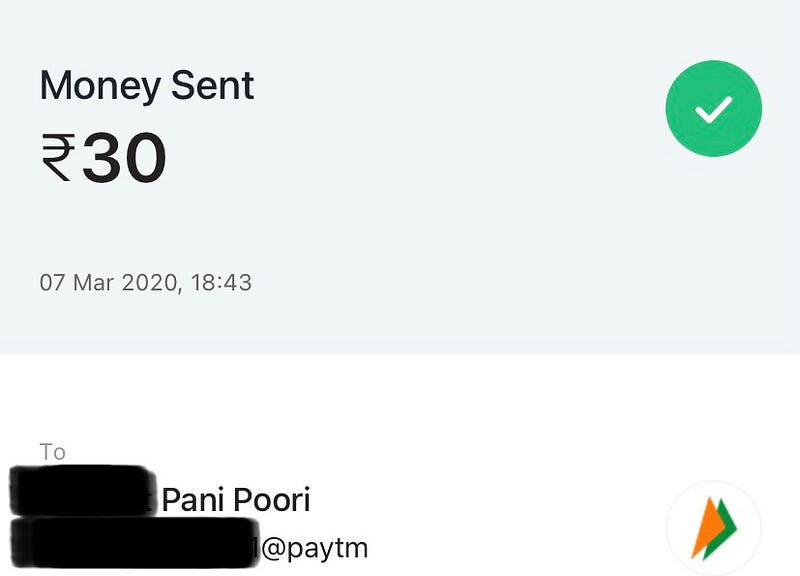

- By entering his Unique VPA (Virtual Payment Address).

(It takes the form of phonenumber@upihandle. For example, if your Mobile number is 9876543210 and you use PayTM, your VPA would be 9876543210@paytm. Presently, we get the facility to replace the phone number with our favourite unique name)

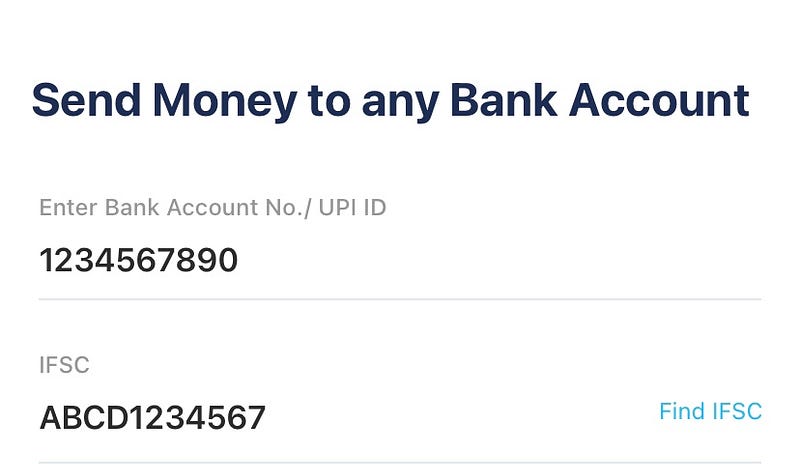

- By Entering his Bank details (Account number and IFSC Code).

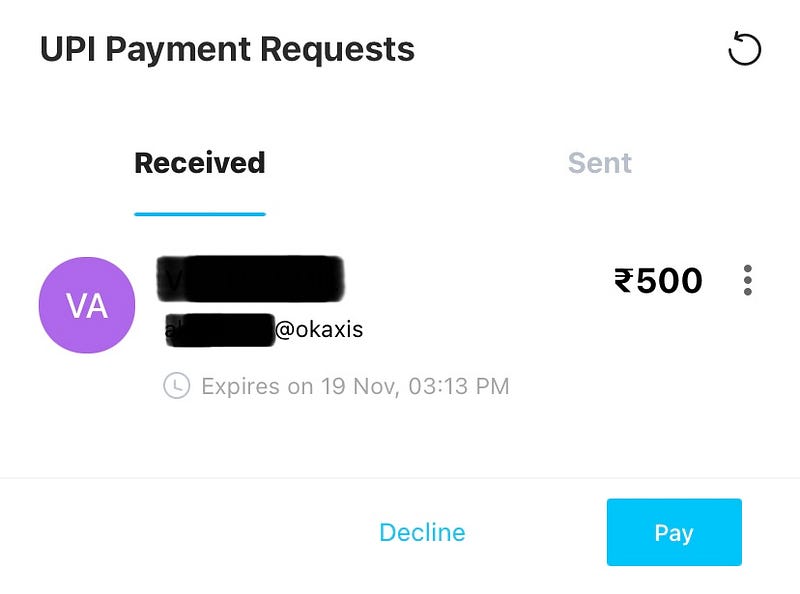

- Accepting payment request from Receiver. (Some Users use this feature to ensure there are no sender frauds. This way, the sender has no other go than sending the required money to the receiver)

What can you do with UPI:

- Pay for online websites with ease.

- Pay at the nearest stores.

- Pay rents, utility bills and recharge instantly.

- The recent additions include paying credit card bills, cylinder booking, challan payment, Metro rail QR tickets etc…

- UPI 2.0 brings many features including Auto-pay and Bill-split with friends.

Popular UPI Apps:

When UPI platform was introduced, NPCI made its own BHIM as its official app for payments. Its a small app that just makes transactions and nothing much. However, with the permission for private players to provide UPI facility, those gained a lot of popularity with their own Cashbacks and offers. And BHIM went almost to zero.

The popular UPI Apps include:

- PayTM

- Google Pay (previously Tez)

- PhonePe

- Mobikwik

- BHIM (Bharat Interface for Money)

- Amazon Pay

- WhatsApp Pay

These apps partner with banks to provide UPI facility. That could be observed in the UPI handle (*****@upihandle). For example, GPay partnered with Axis Bank, HDFC Bank, ICICI Bank, and SBI. That is why you could observe handles like okaxis, okicici etc… This doesn’t mean you need to have an account in their partner banks. They’re just PSPs (Payment Service Providers).

Is it secure?

UPI transactions are secured with a highly encrypted format that’s not very easy to tamper. As the use of UPI is increasing exponentially, there’s an increasing responsibility on the people behind it. The app and transactions are two-factor authenticated by the UPI App’s in-built lock feature and with your own UPI pin. Both could be changed by the user anytime.

The strong point of UPI is that the money never leaves your bank account before the transaction is complete. There’s no intermediate step in the transaction where a third-party gets access to our money. In short, UPI payments are direct bank to bank transactions. If the transaction wasn’t successful and your money was deducted, you can be sure you’ll receive your money back within 3 working days, without the need to contact the customer care.

UPI apps are more secure when both the sender and receiver use the same UPI app. This removes the need of sharing confidential details like VPA or Bank Account number and IFSC Code. However, in the contemporary period of multiple active UPI apps, it isn’t possible often. Still, there’s no need to worry about it.

Frauds? Unfortunately Yes.

There were many cases of UPI frauds since the beginning. To my knowledge, three of the most common are:

- Vishing: Vishing is simply scamsters imitating bank representatives, asking questions ‘on behalf of the bank’. These individuals offer fake loots and offers. They act as if they’re helping us and politely ask our personal details and sometimes our PINs and OTPs too. Once we say, our money is at risk.

- Phishing: Here, the fraudsters send bogus emails where there’s some eye-catching offer mentioned with a link. Once the innocent guy clicks on the link, some notorious virus creeps into his device which targets the UPI apps and gets a note of his PIN, OTPs and all other sensitive information. The information is immediately passed on to the Hacker, who could vanish all the money with a click. Remember, paytm.com isn’t the same as pay.tm.com or xyz.com/paytm, for example.

- Request Money fraud: The innocent people here are mostly children and senior citizens, who don’t know that for receiving money, one doesn’t need to scan a QR code or enter the UPI pin. The hackers tell them to scan some QR code and enter their UPI pin to receive a jackpot. But it’s not mentioned that the receiver would be the hacker himself. Remember, you could receive money even while you’re sleeping. It’s only to send money, you need to do something.

Charges for using UPI:

Initially, a nominal fee of ₹0.5 is charged per transaction. But later, it’s removed to encourage the Digital India movement.

Limits per *** of UPI:

- Money per Transaction: 1 Lakh (However, it could be modified by the Bank).

- Money per Day: 1 Lakh.

- Transactions per Day: 20 (in most of the cases).

Rare downsides of UPI:

- Payment Delay: It’s a trouble when you’re paying to a shopkeeper, which happens when the bank servers are down or busy. However, as already mentioned, you can be sure your money is safe.

- Mobile hang problem: BHIM is the lowest RAM consuming UPI App. Unlikely, private players pack a lot of features and memory which sometimes hang your mobile while paying.

- One time Transfer Limit: For a UPI transaction the limit is generally ₹1 Lakh. But if the bank caps it to, for example ₹20k, you need to send multiple times to send a huge amount, which is time consuming.

- Doesn’t work on slow internet: If your internet is slow, it’s better you pay your friend later instead of paying at the moment. Because, UPI apps demand good internet connection. If it isn’t there, your money may get stuck.

Appendix (Interesting):

1. This is how my friends used to cheat UPI Merchants in my college:

My friends hang out to some shop once and pay the required money by UPI honestly. But from the next time, they don’t pay but rather show the previous payment screenshot. The shopkeeper would be busy to check the date and time of the payment and he says, “Ok Anna, go”.

2. When the Merchants realised it, they made a solution:

This PayTM SoundBox is now being widely used across the country. This enables the Merchant to listen for instant audio payment confirmation and the amount received. This avoids the irritation when he needs to confirm the payment when there’s a huge crowd. It’s offered in many languages too.

So if there’s no audio confirmation, there’s no payment, and that’s sure.

3. 30% Payment cap on Third-party UPI payment apps:

NPCI has announced recently that there would be 30% cap on UPI transactions by Third-party apps like Google Pay, and PhonePe, which hold 80% of the total market share. This would reduce the risk of monopoly. However, PayTM and Jio Pay wouldn’t be included in these because of their payment banking licenses.

The limit of 30% will be calculated on the basis of total volume of transactions processed during the preceding three months on a rolling basis. This would cause a rise to the number of failed transactions. This will be with effect from January 1st, 2021.

4. Launch of WhatsApp Pay:

The two-year long wait of WhatsApp pay now ends. NPCI gives green signal for WhatsApp pay. So far, it was in beta version in India and was restricted to 1 Million users. But now, it’s increased to 20 Million users. The 30% cap applies to WhatsApp too.

PS: There are 400 Million active WhatsApp users in India.

5. Interesting Abbreviations:

- PayTM—’Pay Through Mobile’. One more reason in naming it so might be because PayTM looks like Pay™.

- BHIM—Was named after Bhim Rao Ambedkar.

- KYC—Know Your Customer. It confirms whether the Customer is a True Citizen of the Country or not.