Unlocking the American Dream: Achieving Homeownership Through FHA

Is achieving homeownerships become difficult in America?

Well! everyone knows the answer to that question. But before I start talking about my journey of owning a home in 2023. I would say that I am not a financial expert, however I strongly believe in building assets. Therefore, I decided to buy a house, a small family home that I can afford without being house poor.

Every home buyer’s problem?

My rented accommodation was great, it was a big house with 4 bedrooms and 2 bathrooms, but I always had the feeling that I am just helping someone else building their asset with my money. Furthermore, I wasn’t saving enough because cost of renting a big house, household expenses, insurance and car loans were draining my paycheck. I felt that it will take a lot of time before I save 20% for the down payment. And with ever increase home prices, that 20% will translate into a higher number and I will not have enough to make down payment. Basically, I wanted to end this vicious circle.

What is the solution?

As usual, I started with looking at the properties on Zillow and Redfin. Soon, I had a list of homes I thought I could afford, which were in nice neighborhood, had good schools in the vicinity and were not far from where I work (less than 10 miles from my work location).

Per month I was paying $3,500 plus utilities for my rented home. So that was my benchmark, and I wanted to convert that $3,500 rent into mortgage. With the caveat that I do not have sufficient funds to make 20% down payment to buy a house.

How to secure a loan?

Again, I followed the drill, went to the big financial institutions (don’t want to name any). There response wasn’t very encouraging, considering I neither had sufficient funds for down payment, nor an impressive credit score. Though, they introduced me to the concept of FHA. Initially, it sounded expensive because I had to pay for FHA mortgage insurance which in turn will increase my monthly mortgage.

However, there is a silver lining to this, interest rate with FHA is slightest lesser than the prevailing rates of conventional loan. Though, the biggest benefit is that only 3.5% down payment is needed. For me FHA worked, I was able to secure a loan, own a house and my mortgage is slightly (may be not slightly) more that my monthly rent.

A quick comparison…

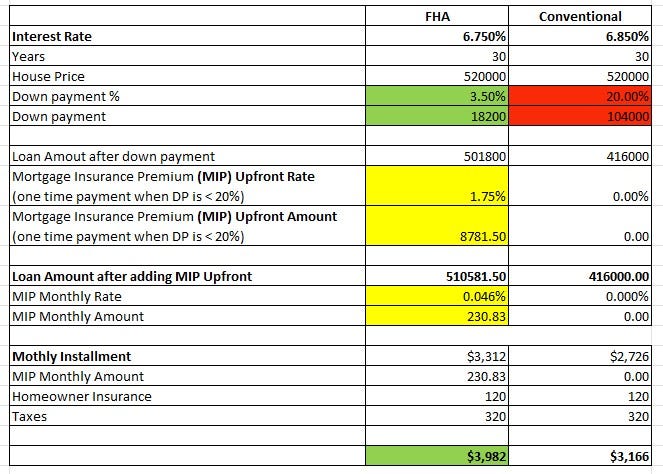

I believe numbers speak louder than words. So here is a quick comparison in numbers between FHA and Convention loan (with 20% down payment) for the house.

Numbers highlighted in RED were the biggest roadblock between me and my dream of owning a house. Furthermore, credit score wasn’t great, another factor I decided to go with FHA loan.

Best part is highlighted in GREEN, just $18,200 in down payment, instead of $104,000.

YELLOW is to remind me the additional cost I paid (upfront), and paying every month to turn my dream into a reality.

Another important fact is, if you put 3.5% down for a $500K home, your PMI is around $230 per month or $8280 for 3 years. However, if you keep renting until you save 20% to put down while paying $3500 per month, you will end up paying $126,000 in 3 years.

PS: I haven’t delved into the details, the nitty gritty of how everything came along, if you have questions then put them in comment section. The objective of this article is to share the personal experience of home ownership.