Time Series Analysis for Financial Data I— Stationarity, Autocorrelation and White Noise

Download the iPython notebook here

While developing a trading strategy, most of the time you are going to be working with time series data. A time series is simply a series of data points indexed (or listed or graphed) in time order (Wikipedia).

The goal of quantitative researchers is to identify trends, seasonal variations and correlation in this financial time series data using statistical methods and ultimately generate trading signals. In order to improve the profitability of our trading models, we can deploy statistical techniques to identify consistent behavior in assets which can then be exploited to generate profits. To find this behavior we must explore how the properties of the asset prices themselves change in time.

Time Series Analysis helps us to achieve this. It provides us with a robust statistical framework for assessing the behaviour of time series, such as asset prices, in order to help us trade off of this behaviour.

This is the first of a series of posts which will cover basic concepts related to statistical modeling of time series and various time series forecasting techniques.

This work derives from the works of Michael Halls-Moore on Quantstart, Quantopian Lecture Series and some code borrowed from seanabu.com

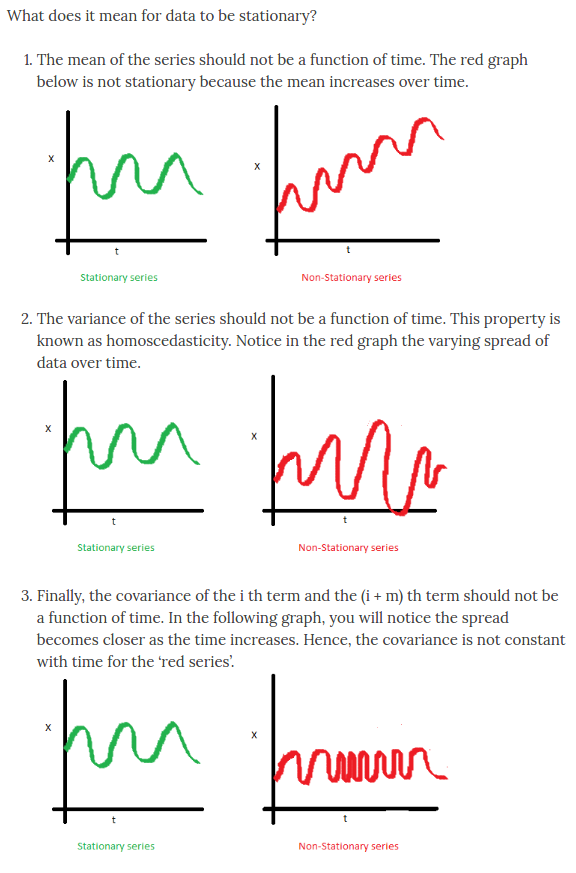

Stationarity, Autocorrelation and White Noise

In this post, we will setup some of the most important concepts in time series analysis that are repeatedly used in analyzing sophisticated series- Stationarity and Correlation. We recommend going through the math workbooks on Random Variable, Expected Value and Variance , Correlation and Confidence Intervals before this workbook.

In the next two posts, we will talk about two higher level models, AutoRegressive Models and Moving Average Models.