Three Easy Steps to Take to Increase Your Credit Score

Stay on top of your credit score, build healthy spending habits, and utilize your credit card in the best way possible

Having a high credit score is pretty desirable and there’s a lot of benefits that come with it. Some of these benefits include; getting better chances at approvals for new low-interest-rate credit cards and loans, getting approved for higher credit limits, and getting better insurance rates.

Furthermore, you need a good credit score in order to get approved for most loans and mortgages. Thus, you can see why maintaining a high credit score is important.

A few months ago, I was in the market to buy a new car. I was confident that I had a good credit score which I could use to get approved for the 0% interest-rate financing promotions at Volkswagen at the time. But, once the finance manager submitted my application for the loan, I was rejected due to a low credit score. Therefore, I had to get a bank loan with a 4.97% interest rate.

This came as a surprise to me because I thought I had a high credit score as I paid off my credit card balance every month on time, and I had never missed a payment. But turns out, there’s more to credit scores than that, so, I decided to look into how I could improve my credit score and these three simple tips helped me increase my credit score significantly.

Disclaimer: I am by no means a financial expert or have any sort of expertise or experience in the field of finances. These are tips that I’ve found through research and have used to increase my own credit score. Make sure to do your own research and/or reach out to a financial expert for serious financial advice.

Having said that, let’s jump right into the first tip.

1. Sign Up for Credit Karma

First and foremost, start using Credit Karma to check your credit score and do it often. This is the first step in improving your credit score, as you first need to be aware of what your score is in order to improve it.

My parents and friends all use Credit Karma and they always suggested that I should use it too. But I didn’t like using Credit Karma because I thought the credit scores they showed weren’t accurate. And, although, Credit Karma scores aren’t completely accurate, they’re still a good representation of the average user’s credit score.

It’s crucial to be aware of your credit score at all times in order to avoid getting into similar situations as I did when I was getting my loan.

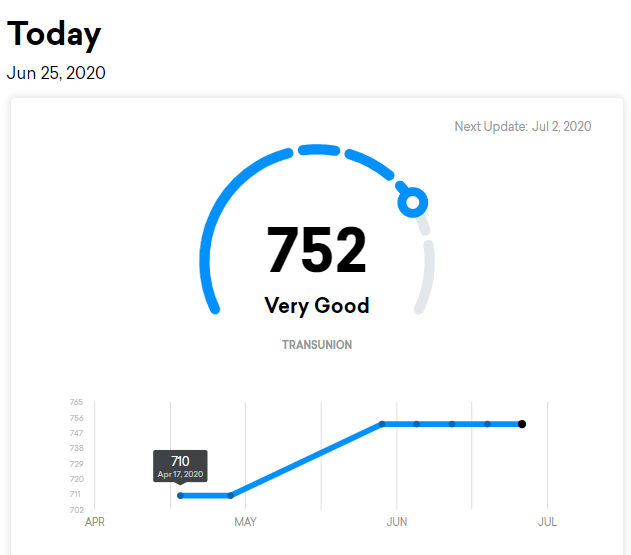

When I finally signed up with Credit Karma, I saw a credit score of 710 which isn’t a bad score, but I wanted to improve it. Over the next month, I watched my credit score closely as I was trying to increase it, and I saw it go from 710 to 752 by May 28th. This felt incredible and it showed me that I was taking the right steps to increase my credit score.

Credit Karma allows you to check your credit score often and stay aware of any changes, so I definitely recommend it to everybody with a credit card.

2. Always Pay Your Balance in Full

The most important thing when you start using credit cards is to make sure that you’re paying your balance in full in order to avoid going into credit card debt and having to pay high-interest rates on that debt.

Do not only make your minimum payment every month.

A common mistake I see people make is only making minimum payments on their credit cards each month. You’re not only not helping your credit score by doing that, but you’re also collecting huge amounts of credit card debt, which you will need to pay high amounts of interest on. If you have the money, always pay your balance in full.

This tip is mostly to help you pay less interest in the long run, rather than build credit. The truth is that there are lots of different algorithms used by credit bureaus when it gets to calculating credit scores, so it isn’t clear what factors affect your credit score the most, but it’s always better to be safe than sorry.

Credit scores are designed to predict the amount of risk a lender is taking when lending you money and the likelihood that you will make your loan payments on time. So, it must help if the credit bureaus see that you pay your balance in full every month. That proves your reliability and the fact that you’re more likely to make your loan payments in full and on time.

So, I always advise people to make their credit card payments in full each month.

Pay off as much of your debt as you can every month if you’re already in a lot of debt

I understand that it might be hard to pay off all of your debt when you’re already in a lot of credit card debt and you don’t have enough money to pay your balance in full. However, in that case, paying even a little more than your minimum payment every month is great. That will help you get out of debt faster while having paid less interest on your debt in the long run.

One piece of advice that I have for making sure you always have enough money to pay your credit card balance in full is to only spend money from your credit card that you already have in your chequing/savings accounts that you can use to pay back the balance with.

Credit cards are amazing to use in order to collect points and build credit with, but make sure you don’t use your credit card to make purchases that you can’t afford.

3. Keep Your Credit Utilization Ratio Around 25–30%

Your credit utilization ratio is calculated by dividing the amount of revolving credit you’re currently using (what you owe) by the total amount of revolving credit that you have (your credit limit).

For example, if you have a credit limit of $1000, and you have a balance of $483 on your card, your utilization ratio is 48.3%.

You want to always keep your utilization ratio at around 25-30%. So, if you have a $1000 credit limit, you want to keep a balance of $250 to $300 on your card. What this means is that if you spend $800 from your credit card, you pay back $550 to get your balance to $250 which would be a 25% utilization ratio.

This is something I pay close attention to every month. Due to the way credit cards are designed, you can always keep a balance on them (without going into debt or getting charged for interest on the balance).

You get a statement every month with a balance that you need to pay by a certain date. The amount you will need to pay is the amount of money you’ve spent within your last billing cycle which is usually a period of 28-31 days, depending on your credit card provider. Therefore, the amount you see on your statement might not always match your actual balance.

Let’s imagine your statement balance is $768 (out of your $1000 credit limit); this is the amount that you need to pay in full by the date you see on your statement. But you’ve also spent another $52 after the last day on your billing cycle. That puts your credit balance at $820. So, after you pay the $768 that you needed to pay back for this month, you have a $52 balance on your card, which puts your utilization ratio at 5.2%.

To increase your credit score you should keep your utilization ratio between 25-30% all the time. This means that whenever you use your credit card, you make a payment to make sure that you don’t go over your 30% utilization ratio. This way you always have a balance on your credit card while having paid your statement balance in full and keeping your utilization ratio around 30%.

Using too much of your credit limit is not good for your credit score; by keeping your utilization ratio at around 25-30%, you make sure that you’re improving your credit score and/or maintaining your good score.

You should also keep in mind that if you have multiple credit cards or lines of credit, your credit limit is the total amount of available credit from all of them. So, your utilization ratio will be calculated based on the total balance on all your credit cards and lines of credit divided by the total credit available.

4. Bonus Tip: Get More Credit Cards and Keep Them for a Long Time

This is more of a tip for maintaining a high credit score after you’ve improved your credit score and you’ve built healthy spending habits.

After all, getting more credit cards is a great way of increasing your total available credit and building credit in return. But if you don’t have healthy spending habits and you’re already in credit card debt, getting more credit cards can be scary and it could lead you to spend more money from your credit cards and get into more debt.

So, if you already have a good credit score and good spending habits and you want to increase your credit score, that’s when you should get more credit cards in order to help you build a stronger credit history.

Creditors like to see a long and rich credit history from you. And having multiple credit cards that you’ve used over a long period of time is a great way to build that long and rich credit history.

One important thing you should keep in mind is that creditors like to see that you’ve had your credit cards for a long period of time, so don’t apply for a new credit card all the time; rather, get a couple of new credit cards altogether and keep them for a long time. You also get credit checked when you apply for a new credit card which decreases your credit score for a small period of time, so you don’t want to be applying for new credit cards often.

Make sure to also keep in mind the fees that come with some credit cards and stay away from those with high yearly/monthly fees. Think about the benefits that come with the credit card you’re getting and how much you’ll be using the card to determine whether the fees make sense or not.

Conclusion

To build good credit and increase your credit score, you need to stay on top of your credit score by checking it often, always pay your balance in full and on time, keep a utilization ratio of 25–30% across your credit cards, and use multiple credit cards to build a strong credit history.

I used these tips to increase my own credit score and I will continue to use them in order to increase my credit score even more and maintain that high score.

Having said that, I’ve never missed any credit card or loan payments; I’ve always paid my balance in full and I’ve never paid any interest on any credit cards. So, it wasn’t hard for me to make the changes that I did. But, no matter what credit score you have right now, or how much interest you’re paying on your credit cards, making these changes will definitely help you increase your own credit score in the long run.

Focus on paying off your credit card debt and staying out of consumer debt, developing healthy spending habits, and following a clear path to increasing your credit score.

Thank you so much for reading this article. Feel free to share any other tips that you use to build a high credit score.