Thoughts On Savings After A Reader Hits Back On Paying Off A Mortgage

Never Retire Checklist: #14

Today’s installment is as much about how psychology impacts our financial decisions as it is about saving money. So let’s intro it with this before detailing how I view and execute savings.

I received pushback from a subscriber the other day in response to this —

If you had $500,000 left on your mortgage at a payment of $2,300/month, $2,000 in other expenses, $550,000 in savings and work that generates $5,000/month, what would you do?

- I would pay off my mortgage.

- Save $2,300 each month, resulting in a $3,000/month surplus.

- If my work was easy on the body and mind and required only around 20–25 hours a week, I would use $2,000 of that $3,000 surplus to replenish my savings each month. While it would take about 20 years to get back to $550,000, it only takes five years to get to $125,000. Not too shabby.

- $125,000 would cover my $2,000 in monthly expenses for more than five years.

That’s how much having no or a super low housing payment means to me.

We had an exchange where he made the sound mathematical argument against what I would do —

I completely, 100% see where Jeff is coming from. I love that Jeff took the time to respond. In fact — in full disclosure — I sent Jeff an email inviting him to write a guest post for the newsletter in response to today’s post. I want different perspectives, even if they poke holes in mine.

I don’t mind being challenged, because the financial choices I make come from me developing an understanding of who I am and how I function best, not how others are and what they do. (More on this throughout and at the end of today’s post).

The only issue I have with Jeff’s response(s) is that he seems unable to see where I am coming from. To suspend his convictions to acknowledge and accept that I’m a different person with different fears, motivations, goals, experiences and, subsequently, concrete responses. It all depends on your perspective and psychological makeup.

How do you feel in one personal financial situation versus another?

Because I feel one way and do certain things in response doesn’t mean you will or should do likewise.

We all have our rationale as we do what works for us, even if it sounds illogical and objectively wrong to others.

To reiterate and expand on my points on why I’d take a lump sum of savings and pay off (or aggressively pay down) a mortgage if I had one —

Low overhead IS savings. In making his argument for keeping the mortgage, Jeff mentioned concerns that would drive him to keep the loan payments. His rationale is if something happens and he can’t handle the payment, he has the cash — in savings — to make the payment, absent other ongoing cash flow from work or another source.

You can’t argue with that. It’s sound logic. Makes sense. For Jeff. Maybe for you.

I look at it another way, which is one reason why I never took the plunge into home ownership and will only do so once my partner and I have enough cash saved to pay cash — or close to it — for a property we can afford in a city neighborhood we love.

Regardless of how much money I have saved, nothing freaks me out more than overhead. So the lower my overhead, the better. The less money I am obligated to put out each month, the less stress I experience and the better I feel generally. I don’t view savings as a safety net to cover a mortgage obligation I’m not comfortable taking on in the first place.

I have situated my work in a way that I’m as close to 100% confident as I can be that it will continue to generate ample monthly cash flow now and for the duration. I use this to cover my expenses, spend on wants and contribute to savings via my pots of money.

I’d rather be obligated to $2,000 in monthly expenses than $4,000, no matter how much money I have saved.

I’m not ashamed to admit this is an emotional response. However, nearly every time I have removed — or ignored — my emotion as part of a financial equation, I have made a mistake that ended up costing me more money than had I followed my instinct, driven by my psychology. (I’m planning a post to elaborate on and illustrate this idea for April).

My parents took a similar view. And it worked out well for them.

My Dad’s #1 goal, after buying his second home around age 55, was to not leave my mother with a mortgage payment if he passed away. And to not have to deal with one himself as he got older. For the record, my Dad worked — full-time — well into his 70s. He only quit because, in his words that make me chuckle, sooner or later, you have to retire.

Today, at age 87, my Dad has long accomplished his goal. He paid off his 30-year mortgage in less than 20 years. My parents have two cars, but no payments. They have very few fixed expenses to speak of. My Mom, who is 12 years younger than my Dad, literally has nothing to worry about if my Dad passes. And, of course, the inverse holds true. The money that used to service the mortgage goes to savings (and has been for years now) and a majority of the cash flow coming in each month at my parent’s house gets spent or saved.

I’m also willing to admit that my situation colors my views on what I’d do in a, for me, hypothetical situation.

I don’t have $550,000 saved. I don’t have a $500,000 mortgage. I don’t want to have a mortgage payment. I maintain as low a rent payment as possible. My personal finance focuses on the lowest cost of living possible. My next housing move will — barring some unforeseen circumstance — result in a lower housing payment than I have today or it won’t happen. My parents experience has certainly influenced all of the above.

It’s all about perspective. Some of us do things backwards. I’ll leverage my low cost of living (thanks to not owning a home now) into savings. When my partner and I have ample cash saved to do so, we’ll spend it on a property in a place where we our housing expense will be close to zero and healthcare expenses are less of an issue.

How and especially where I see my future also colors my perspective in this conversation. Planning for old age in America is different from planning for it in Spain or Italy.

This discussion is as much about savings — and how you prefer to save — as anything else. Because savings can mean more than one thing, depending on your perspective.

Savings isn’t just cash in the bank. Savings is also how much you save (as in, don’t spend!) each month thanks to your low cost of living. You can’t have a low cost of living with an out-sized mortgage/housing payment.

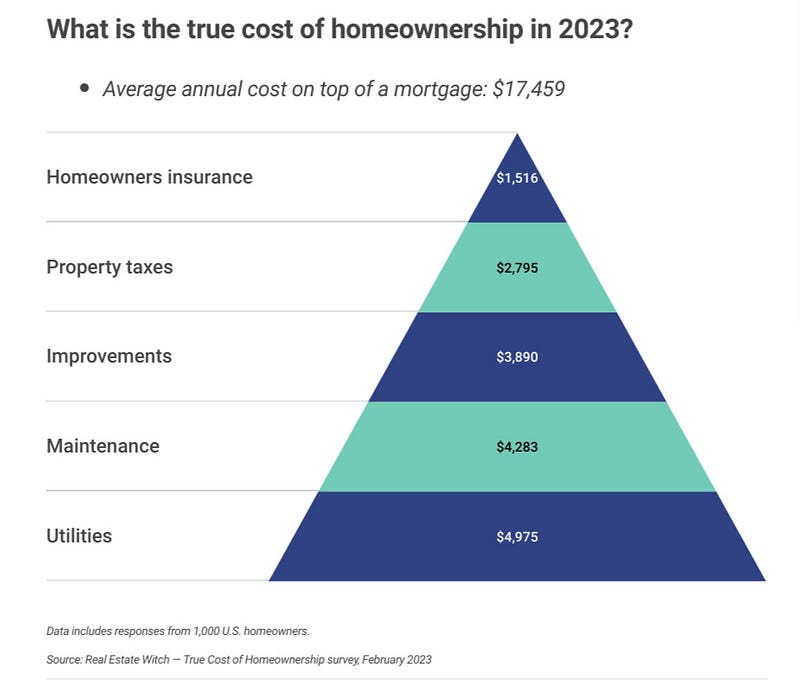

The typical homeowner in 2023 pays close to $18,000 a year in expenses on top of their mortgage.

If you’re dropping a couple to a few grand on a mortgage only to be on the hook for another, on average, $1,400-$1,500 a month, the mathematical logic behind keeping a mortgage alongside a lump sum of cash goes out the window. Or comes razor thin close to going out the window.

In my world — and it might not be as financially big as yours — a mortgage payment plus the attendant expenses of home ownership would render saving a dream. Absent taking on way more work than I want to do, there simply would not be anything left over to save.

Not having these monthly expenses IS my savings plan. And it’s a low pressure savings plan.

If the gap between what you have to spend and what you earn each month is small, you’re under pressure to save. One unplanned expense or errant impulse purchase and you can’t save. A small monthly surplus — thanks to high overhead — also curtails your ability to spend freely, but within reason.

It’s important to note I’m talking about people like me, who make decent or better money, but are still of modest means.

I like to give myself the room to spend each month before I save. I can only do this — on my income and desired amount of work — if I maintain the lowest overhead possible.

Here’s my savings plan —

- I match income to expenses. Each month I have an idea of what each of my income streams will generate. I earmark all or part of each stream to my large expenses.

- I cover small, everyday and discretionary expenses with my checking account cash cushion. So I do my spending before I do pretty much any savings, except for —

- I make modest, weekly deposits into my pots of money.

- I match saving to spending.

- Every time I use my debit card, my bank transfers $1 to a savings account.

- When I think twice and pass on making a discretionary purchase, I transfer what I would have spent to one or more pots of money.

- When I make a purchase — typically travel — I aim to save all or a percentage of that purchase. So, make a $250 Airbnb payment, save $125. Book a $50 train ticket, save $50.

- At the end of the month, after paying my fixed expenses, doing a small bit of automated savings and matching saving to spending, I see if I have a surplus. If I do, I ensure my checking account cash cushion is sufficient headed into the next month. From there, I save the rest into my pots of money.

Here again, this — a focus on minimal large monthly expenses, spending before you do most of your savings, matching savings to spending — might not work for you. I know it’s unconventional. I know it’s driven by my odd approach to personal finance.

However, that odd approach is the result of years of learning about myself in relation to how I feel about money, how I spend money and the conditions under which I save the most money. It comes after years of trial and quite a bit of error. This is the only way you can devise personal financial plans that work for you. You have to find out what works for you — blocking out conventional approaches in the process — and devise a comprehensive strategy that takes into account and is best suited to your personality and psychology, quirks and inconsistencies and all.

Today’s article, a version of which appeared in my newsletter, continues a month-long series on Medium. Receive a notification each time I publish a Medium article by going here.

Medium readers can receive 50% off a one-year subscription to my Never Retire newsletter.