HEALTHCARE IN AMERICA

This Is Private Health Insurance in America

These are our options, and yes, we’re “underinsured”

Hello, and welcome to my soapbox.

I’ve shared in previous posts about how we spent $11,000 on medical care last year. Often, I’m asked, “Well, can’t your husband select a better healthcare plan?” When we first got together, I asked him the same question.

After sitting down with him and reviewing our options, I realized a “better” healthcare plan was not an option, nor were the so-called “better” plans much better.

My husband works for a well-known global insurance consultant. Yet, the insurance options they offer their employees are expensive and unaffordable. Since they also publicly show what options are available on their website, I’ll share some screenshots.

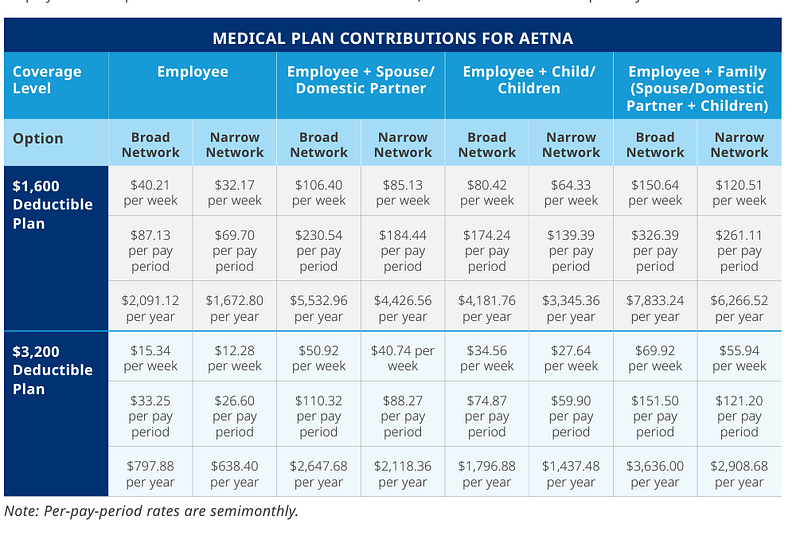

Our Options

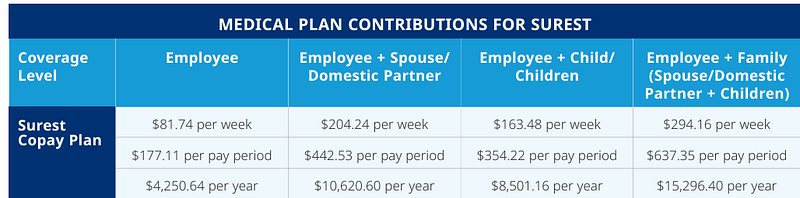

His company offers benefits through three companies: Aetna, Anthem, and Surest. The Aetna and Anthem benefits are identical, so I’ll share the Aetna ones (which are what we have).

These are the current 2024 plans. Back in 2021 when we had our son, there was also an $800 deductible plan. The company no longer offers that plan.

What We Pay

We pay for the $3,200 deductible plan and the narrow network for my husband, myself, and our son. It does not benefit us to get the broad network, since we have never had an issue finding an in-network provider. It costs $121.20 per pay period, and my husband gets paid twice a month. So, we pay $242.40 per month for this plan for our entire family.

This table does not reflect the out-of-pocket max or family deductibles. Our individual deductibles are $3,200, which means each one of us has to pay $3,200 before the plan will pay a penny. However, we also have $6,400 family deductible, so if two of us pay $3,200 (or my son and I each spend $1,600 in addition to my husband’s $3,200), then the deductible kicks in for the whole family.

Even once we reach our deductible, we still have to pay. Our plan only covers 70 percent of services until we reach $6,400 individually or $11,800 total.

This is what I learned last year: These services do not count toward the family deductible! My husband reached his deductible, and all services that went toward his “out-of-pocket max” after the deductible was met did not count toward our family deductible. This meant, that even though we’d spent well over $6,400 as a family, my son and I were still paying full price for medical services.

Why We Cannot Switch

- Not much cost savings

The biggest deciding factor for us not to switch is that we would spend an additional $3,357.84 per year whether we used the services or not. We would also still have a $6,400 out-of-pocket max. Let’s do a little math.

$6,266.52 + $6,400 = $12,666.52

Meanwhile, with our current plan (assuming we reach out out-of-pocket max):

$2,908.68 + $11,800 = $14,708.68

While we would “save” $2,042.10 each year, the biggest problem is that’s only true if we come that close to our out-of-pocket max. So, we would have to spend $9,757.90 as a family to justify this switch.

2023 and 2021 (the year my son was born) are the only years we’ve reached our out-of-pocket max. Usually, we’re nowhere near it.

2. It’ll add extra financial burden to our family

The second problem is that if we switched to the $1,600 deductible plan, an additional $139.51 would have to come out of my husband’s paycheck each pay period (or $279.02 per month). This will make it harder to pay all of our bills and make ends meet since we are barely breaking even with all the expenses that have come up in the last year (in addition to medical bills).

Medical bills can be put on payment plans, and they usually don’t send your bill to collections until after six months of nonpayment. A premium needs to be paid every single pay period, so that’s an immediate hit in the money available to spend on other bills.

3. The high-deductible plan comes with a Health Savings Account (HSA)

Another benefit is that the higher deductible plan comes with a Health Savings Account (HSA). The best part about this HSA is it carries over from year to year, so we can use money put into from last year this year. My husband’s company also contributes a small amount to this savings account.

HSAs are pre-taxed money put into a special account that can be used to pay for doctor’s visits, medications, and even some over-the-counter products. We had over $5,000 in our HSA last summer when my husband went into the hospital, which is what he used to pay for the visit.

By using untaxed dollars in an HSA to pay for deductibles, copayments, coinsurance, and some other expenses, you may be able to lower your out-of-pocket health care costs. — Healthcare.gov

The Other Plan

There’s one other plan I have not addressed, which is supposed to be the “best” insurance plan my husband’s company offers.

Wowza! I don’t even have to do math to figure out that we cannot afford this plan, because the premiums alone cost over $15,296.40 per year. This is a whopping $3,496.40 more than our out-of-pocket max! Who in America can afford this plan?! Plus, you still have a copay with every visit, so you’re going to end up paying way more than you would with either of the other plans.

Medical bills can be delayed. Premiums cannot.

Our Health Insurance Reality

This is where we are right now. We could save some money by switching to the $1,600 plan, but the savings are minimal and only beneficial if we know for certain we’re going to spend around $10,000 in medical care for the year.

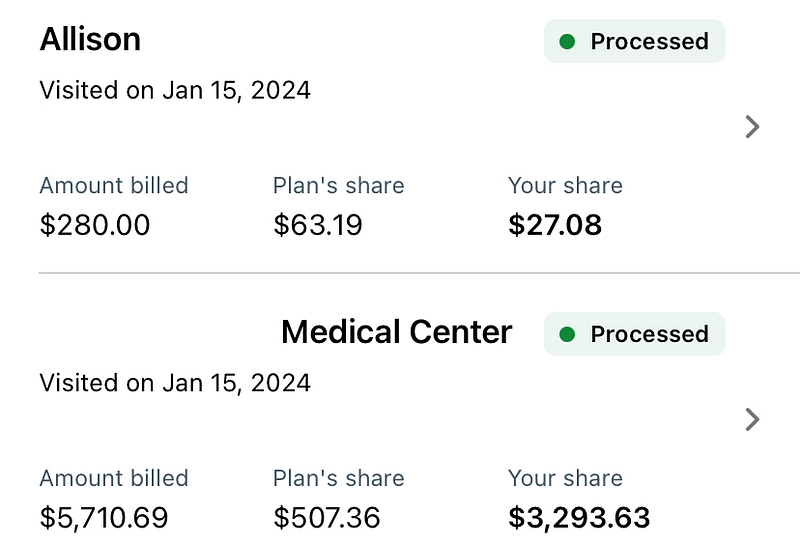

So, this is what an ER visit looks like when my husband wakes up at four in the morning and can’t breathe.

We’re still nowhere close to $9,757.90, but it’s only January.

Moving Forward

I pray every day that I can find a job that offers better benefits than my husband’s. As shocked as everyone seems when I tell them what we pay out of pocket for insurance, I feel like this can’t be the norm.

No family should have to pay over $10,000 a year for health insurance.

Also, in case you’re wondering, my husband doesn’t make a ton of money. He doesn’t even make six figures.

Health insurance in America is a broken system, and I wish it could be fixed.

If you enjoyed this article, please consider subscribing to me.