Thinking of Paying Off Debt…You Might Learn One or Two Things From My Reality

A man in debt is so far a slave.

In May, I was in talks with the bank about clearing my credit card debts. In an email, they offered a debt consolidation loan. After reading the fine print and working out the numbers, it turned out their offer was more marketing than dealing with my reality.

So I had to look for alternatives. I got in touch with a debt consolidation company. This wasn’t a first and their offer wasn’t the best either.

For a fee of 700 dollars, they would get the banks to write off my credit card interests, but I would pay the amount owed in full. My credit score would also tank.

I didn’t think this was a good deal because I had once spoken with another company that offered to write off a percentage of the amount owed besides the credit card interest. That offer had long left the table.

I left like I was between a rock and a hard place. The onus was on me to pay off the debts as quickly as possible and freeze the use of the cards.

For the card with the lowest limit, I cleared off the debt and froze the card. I thought of selling off some of my assets to clear the other outstanding bills. Instead, I used up my savings. With that, I reduced one credit card debt to 60%.

Then another email came from my primary bank. They were offering me a balance transfer to their card. Let’s call my primary bank card A and my secondary bank card B.

Card A interest rate is almost 18% and Card B's interest rate is almost 20%. The transferred balance’s interest would be 5%. I accepted the offer and moved some money from Card B to Card A. Now the balance on Card B sat at 60%.

The next move was I canceled all payments on all my credit cards and moved them to my debit card. It is counterproductive to make so much effort while accruing more debt. Besides, it is irritating that someone is making money from you with interest rates just because you have outstanding balances.

Before, I practiced minimalism. Now, I have taken it to a whole new level. In my current makeshift budget, my main expenses are rent, transport, phone bills, feeding, and credit card debts.

Shopping for anything else is now secondary. Good enough, I have other essentials that’ll carry me now and hubby for a while.

Food shopping has taken a new dimension. Apparently, processed food costs more than unprocessed food. So I spend the food budget on the latter. The upside is I get to maintain my health even better.

Gone are the days when we go shopping just for fun. We now shop intentionally. As for the fridge, no food item gets wasted.

I get paid in cheques. I do not cash these cheques until an expense is due. That way, I control spending.

I tuck away my credit cards in my drawer at home. They have no business in my purse. I think they are for real emergencies or guaranteed investments.

For my friends who invite me for outings like birthdays and anniversaries, I look around the home for things I can repurpose as gifts. If I do not find good options, I go on minimalist shopping. Fancy has gone out the window.

Now the balance transfer option is open till August 30th, 2023. So a primary goal now is to pay off substantial debt on Card A to create room for more transfers from Card B before the August deadline. There is a clear difference between paying off debt with an interest of 5% and an interest of 20%. The offer of 5% interest is for 3 years and so, they cut out my work for me.

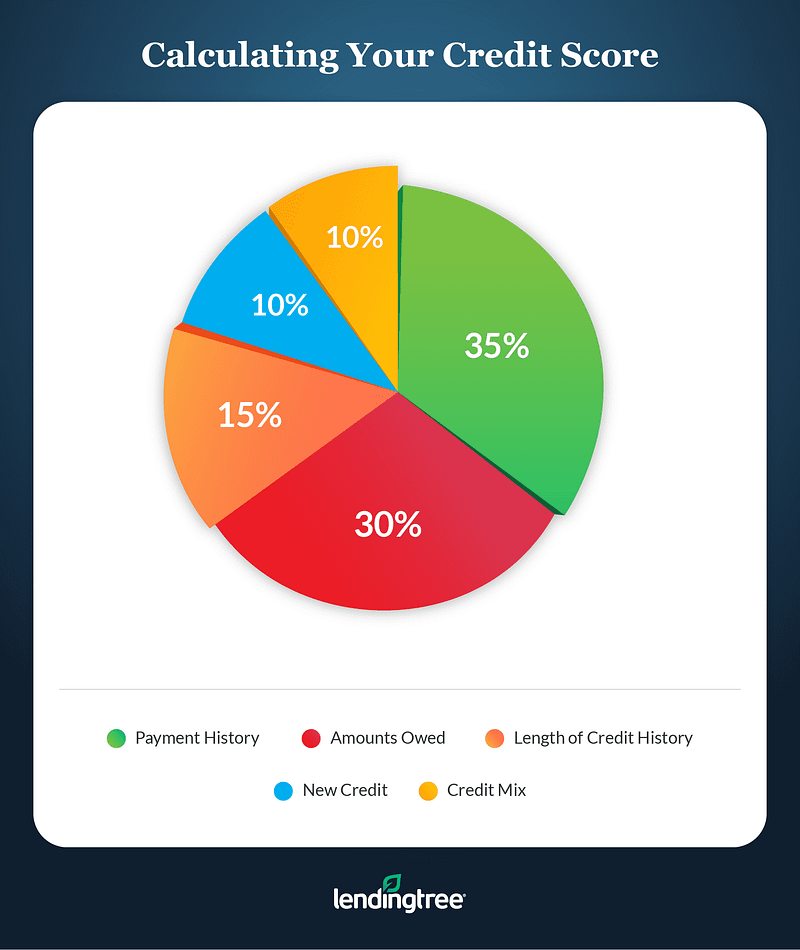

One downside: My credit score took a hit. It would keep looking unsexy as long as the balance transfer happens from Card B to Card A. The transfers make the utilization ratio [fraction of amount owed] for Card A very high, which has a huge impact on credit scores.

As an add-on, I have an accountability buddy who checks in on my progress now and then.

When this is all over, I’ll be smiling like the lady in my head photo and the next time the banks make a good offer, I’ll probably do extra scrutiny or run like the lady in the photo below.

Thanks, Jason Edmunds.