The Real Reason People Are Bad With Money

And 5 ways to overcome it…

“They say ignorance is bliss… they’re wrong”

-Franz Kafka

If you’re part of the roughly half of Americans who can’t come up with $2,000 in 30 days for an emergency, this article is for you. If you’re not sure how to get started with tackling debt or your finances in general, this article is for you.

Even if you already think you’re a finance ninja, this article is for you because you’ll see how there are layers to this big idea that applies to everyone. The fact is, we all have room for improvement when it comes to personal finance.

In the end, I’ll offer 5 concrete solutions to overcome the problem. What is that problem?

THE OSTRICH EFFECT

The real reason people are bad with money is because of the ostrich effect.

According to TheDecisionLab:

“The ostrich effect describes how people often avoid negative information, including feedback that could help them monitor their goal progress. Instead of dealing with the situation, we bury our heads in the sand, like ostriches. This avoidance can often make things worse, incurring costs that we might not have had to pay if we had faced things head-on.”

Originally, it was coined based on attempts by investors to avoid negative financial information due to fear of negative performance. Studies show that investors check their portfolios far more often when the market is up than when the market is down.

This is a psychological response to what we know to be bad news. It’s human nature to avoid information that can be upsetting.

BLIND SUCCESS

Funny enough, I think keeping your head in the sand altogether is a good strategy when it comes to investing. I always recommend investing in index funds that track either the S&P500 or the total stock market and investing a set amount at a set time interval no matter what. This is called dollar-cost averaging.

Then ignore the market completely. Set it and forget it. Stay the course. In the long run, the market always goes up.

I’ve developed an aversion to receiving all information, especially information about a down market because those losses are temporary.

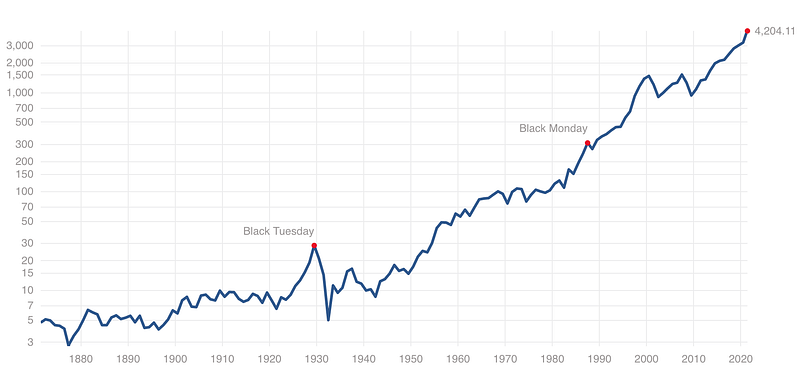

People often forget you don’t lock in losses unless you sell investments when they’re down. Understanding historical performance, which is as easy as looking at this chart, is all you need to know to feel confident going forward.

When the market took a downturn in 2009 when the housing market crashed, smart long-term investors knew to avoid the news and fear-inducing headlines.

If you’re investing for the long-term, it’s best to not get caught up in the weeds of day-to-day volatility. Burying your head in the sand can be good in this one specific situation.

But that’s not the point of today’s article.

PSYCHOLOGICAL DISCOMFORT

The definition of the ostrich effect has widened and is commonly used in reference to people that avoid exposing themself to negative information in fear of it causing psychological discomfort.

In truth, many people hide information or ignore problems because the truth can hurt. It is human nature to run away from threats or fear the unknown.

This happens often in real life in many ways. For example:

- Avoiding the doctor or dentist

- Developing anxiety about an upcoming performance review

- Avoiding the scale even when you’re on a weight loss program

- Not knowing the annual interest rates on your credit cards like half of Americans

Don’t mistake these for laziness. It’s in our DNA to avoid difficult situations and bad news. We despise loss and losing. Instead, we protect our ego by staying firm in our happy-go-lucky beliefs.

Wile E Coyote is the poster child for avoiding the truth. Whenever he finds himself outwitted by that darn roadrunner, he’ll often admit defeat by doing something like covering his eyes when he’s staring at a train barreling down on him with dynamite on the tracks.

We laugh and sympathize because we relate. But his situations, like many of life’s bad situations, are avoidable.

Ignorance is bliss. But it’s still ignorance.

The reason most people are bad with money is that they don’t understand their financial situation because they avoid it. They don’t log into their accounts. They don’t track spending or net worth. They don’t set goals.

People hide from reality. They bury their heads in the sand. Then they wonder how their debt reached 5-figures. They fail to understand that ignoring the problem is robbing their future selves. Plus, they’re missing out on the benefit of time in the market.

Time can be your best friend or your worst enemy. Compound interest is great when you’re invested and your money is growing exponentially. But time is a jerk when compound interest is working against you — like credit card interest.

I ignored my finances until January 1st, 2018. In the back of my mind, I knew it was bad but decided to deal with it later. I did, but it took years of commitment to dig myself out of a hole and make up for decades of lost time.

I’m proof you technically can deal with it later. But I missed out on years and years of investment growth I’ll never get back.

EXCUSES

Getting organized is hard. Knowing your net worth or credit score can sound terrifying. Learning about investing? I’d rather get a root canal.

It doesn’t help that talking about money has become incredibly taboo. Most of us feel like we have nobody to talk to about money. We don’t know who to trust. We feel alone and embarrassed. Plus, they didn’t teach this stuff in school!

But these are excuses. I eventually found that out the hard way. You don’t have to.

This ostrich effect is holding people back, putting people in debt, and it gets far worse when ignored. It also affects people that are decent with money but could be even better. We all have blind spots. We all have room for improvement.

Most people aren’t preparing for their future. The data doesn’t lie. 63% of people are living paycheck to paycheck in the United States. Some studies indicate this number is higher.

It’s not all doom and gloom. The alternative is simple. Don’t deal with it later. Get started today.

WHERE TO START

First of all, get financially prepared for emergencies! Setting aside $1,000 that you will only touch when an emergency comes up is a massive step and will help you sleep at night. Because:

“Everybody has a plan until they get punched in the mouth.”

-Mike Tyson

If you’ve made mistakes or have regret, let them go. Take it one day and one action item at a time. There is nothing more relieving than knowing that you took that first positive step in the right direction.

Next, invest more towards retirement. Time is your best friend when it comes to investing. A 10% return for 20 years generates more money than a 20% return for 10 years. Plus, not contributing towards a company match is throwing away free money.

YOU DON’T KNOW WHAT YOU DON’T KNOW

The ostrich effect means people continue to not know what they don’t know. This is called the Dunnig-Kruger effect, where people lack enough basic financial knowledge to even realize that they’re making mistakes. People’s lack of understanding about key concepts like compound interest and inflation can lead to thinking you’re making good financial decisions when you’re making things worse.

Further ignoring finances can lead to succumbing to lifestyle creep where your spending increases as your incomes rises. Some might call that a good problem to have but no, it’s a problem. As you earn more, you should absolutely save and invest more — not get better at spending.

A recent study showed 18% of people earning 6-figures are still living paycheck to paycheck. By spending money as they get it, they’re stealing from their future selves.

People also develop bad money habits that stick, like impulse buying. As an example, they congratulate themselves for saving $20 on a pair of $100 jeans instead of admitting they splurged away $80. With the ostrich effect, people would rather feel good about saving than looking closely at their spending.

HOW TO OVERCOME THE OSTRICH EFFECT

Ignoring personal finance is bad, obviously. But what’s good? Here are 5 non-obvious strategies to help you overcome head in the sand syndrome.

Tip #1: Development mindfulness.

Being aware of the problem is step one. Ask yourself some challenging personal questions like “What am I really afraid of?” or my favorite: “If I were giving my friend advice about the same situation, what advice would I give them?”

For the first question, you might surprise yourself with what you come up with. It could be fear of the unknown. Fear of failure. Fear of feeling helpless. Fear of damaging your ego. Oftentimes, what we’re fighting with externally or internally isn’t the actual problem. There’s something else beneath the surface causing the issue.

And you would never tell a friend to ignore their financial situation so why would you do it yourself? The friend perspective offers instant personal perspective.

Tip #2: Get exposed.

The exposure effect is real and it means that things become more likable as we expose ourselves to them more often. Taking 5 minutes a day to look your financial fears in the face or confront a blind spot is an excellent starting point. You might find the situation isn’t as bad as you thought. You might also find a few quick wins that help you build momentum.

Then, gamify it. See how many days in a row you can spend 5 minutes working on your finances as a goal. Celebrate in a fiscally responsible way when you break a record.

Getting exposed means replacing imagination with real-life data consistently.

It’s like being convinced there’s a monster under your bed as a kid. The first time you looked it was extreme relief. The 10th time you looked was the last time you believed in monsters. And by you I mean me…

Force yourself to look. It’s the best way to conquer fear.

Tip #3: Develop a long-term mindset.

When trying to improve your financial life or even trying to scale your investments, know that you will experience setbacks. That’s okay when you have a long-term mindset.

Turning a bad financial situation around is going to take time. Completing goals takes time. Building wealth or starting a business takes time. The same is true when losing weight. It’s consistent action with a long-term approach that dictates a successful result. And as hard and challenging as things can feel in the moment, I like to picture myself in the future looking back on the journey with extreme satisfaction.

This is also a good time to establish why you’re doing something. Why do you want to improve your financial situation? What would it mean to succeed? Don’t be in a hurry. That will get overwhelming, fast.

Tip #4: Help yourself or ask for help.

Admit that you don’t know what you don’t know and get started by getting educated. This could actually be your first action. Start learning. It’s a beautifully simple first step.

That’s what I did in my year of getting good with money in 2018. I found a finance podcast I loved — The Stacking Benjamins Show. I listened to it every day. Eventually, I had a few ah-hah moments that propelled me into action. I wasn’t expecting that but learning encouraged me to overcome my fear.

The second thing I did was get a library card and put a dozen finance books on hold. There are many free resources available but it has to come from a genuine place of curiosity. And here is a quick tip about reading: don’t read because completion is the goal. Read to learn. Read chapters out of order. Take notes in the margins.

Either way, get curious and get knowledgeable. I’d be remiss if I didn’t mention my two books. My first, The Money Resolution, is perfect for beginners. My second, Money You Can Hack It is full of creative ways to grow your wealth.

Tip #5: Automate.

A really nice and easy way to get started is to automate your bill payments so you won’t miss a payment and get hit with a fee.

You can also automate your savings. Increase your work retirement contribution by 1% or commit to setting aside $100 into savings as soon as you get started. It’s like hiring a personal trainer — you commit financially so that you know you’ll show up to the (finance) gym.

I’ve also found ways to automatically make time for learning throughout my day. When I take the dog for a walk, exercise, or clean the kitchen, I use that time to listen to an educational podcast or audiobook.

What’s great about automation is that it’s a beautiful foundation to build on. Most of my financial wins happen automatically. I wrote books and started a finance YouTube channel because I kept wanting to work on my finances but there was only so much I could do daily once I automated almost everything.

Bonus: Talk to somebody.

I do this with my fiancé during what we call “Money Parties” once a month. You can ask family or even a close friend for help or advice. You can seek out a professional. You can even contact work. You might be surprised about how willing HR is to point you in the right direction.

Either way, open up about your situation and talk to somebody.

This was a struggle…

If I can be honest, I struggled to write and finish this article. I spent days researching. I started over 3 different times because I had the opposite issues: too much information and analysis paralysis.

At one point I buried my head in the sand and put it out of sight and out of mind for a few days. Ultimately I committed and overcame my personal doubts and fears. This article still isn’t perfect but ego is the enemy and done is better than perfect.

Push forward with positivity and confidence. Take it one day at a time. That helped me finally pull through to finish this. Remember, it’s okay to be vulnerable and admit to struggling or needing help.

We all have blind spots — fears that hold us back or gaps in education. We all have things that keep us up at night. I call these mental monsters. I challenge you to continue to think about the money things you don’t know or the parts of your financial life you ignore. I challenge you to overcome the ostrich effect.

Takeaways

Focus on doing what you’ve been avoiding. Learn about challenging financial topics you’ve been avoiding. Focus on bringing light to your financial fears and self-improvement.

Getting stronger in an area of strength is good. But if you can turn your weakness into a strength, you will be great. Possibly, unstoppable.

If it’s all dark and dim because you avoid all things money like many, get started. Make the commitment. The first step is the hardest. But remember, only an object in motion can gain momentum. If you stick with it you’ll discover success comes gradually, then suddenly.

We all hate loss and losing, but ignoring a problem or financial issues is the only guaranteed way to lose. The only thing you have to fear is fear itself.

If nothing else, remember this: Ignorance isn’t bliss. It’s ignorance. Curiosity is king and knowledge is power. Every day you’re moving forwards or backward financially.

Get your head out of the sand and move forward today.

I hope this helped motivate you to get started, or encouraged you to keep going. Hopefully, this provided some clarity for your next steps.

If you want to know more about gaining financial clarity, read this article next.

What’s a finance topic you’d like to learn more about? What’s a blind spot you think you have? Don’t hesitate to share!

Watch the video version of this article on YouTube here.

Frankie Calkins (M. Ed) is a Digital Marketing Manager by day. On nights and weekends, he’s an author, YouTuber, and finance course creator. He lives in Seattle, WA. Contact: [email protected]