The Money You Save by Paying Extra in ONLY Years 1–3 of Student Loan Repayments

How big a difference does it make paying $50/month extra for 3 years at (1) the beginning, (2) middle, or (3) end of student loan repayment? It’s huge….

More articles

• What’s the Smart Play If You Borrowed $40,000 at 10% in Student Loans and Just Graduated College? • Chat Threads — Student Loan Borrowers Taken for a Ride as Supreme Court Sides with Lenders • Life Expectancy vs. Healthcare Costs in the U.S., Japan, Germany, etc. — whatever you’re expecting, you’re going to be surprised. • U.S. Housing Price Predictions for 2023–2024 • Are Chinese People Smarter About Mortgages than Americans? • The Social Contract Broke in the U.S. Years Later Than in Japan • 2 Reasons Populations Are Collapsing in Developed Countries • How the Al Dente App Eliminates the MacBook Battery Life Problem

There are 3 things that account for most of the interest that people pay on their student loans:

- Total amount of money you borrow;

- Interest rate for your loans; and

- Length of time you take to pay back the loans.

Depending on the interest rate on your student loans, it’s very likely that you will end up paying more in interest than the amount of money you originally borrowed!

Once you have borrowed the money — and especially after you have spent it — you don’t have much control over #’s 1 and 2.

But you do have a surprising amount of control over #3.

Here’s how that works.

Pay extra amounts each month on your student loans beyond the standard monthly payment.

I already discussed this in detail in the previous article, “You Just Graduated College and Borrowed $40,000 at 10%. What’s the Smart Play?”

But there are a couple pro tips that really turbo-charge the impact of your earlier payments.

Here’s the Pro Tip — Whatever you’re going to pay extra on your loans, pay it AS EARLY AS POSSIBLE.

The earlier in the repayment term you pay extra:

- the more interest you’ll save; and

- the more you will decrease the time it takes to fully pay off your loans.

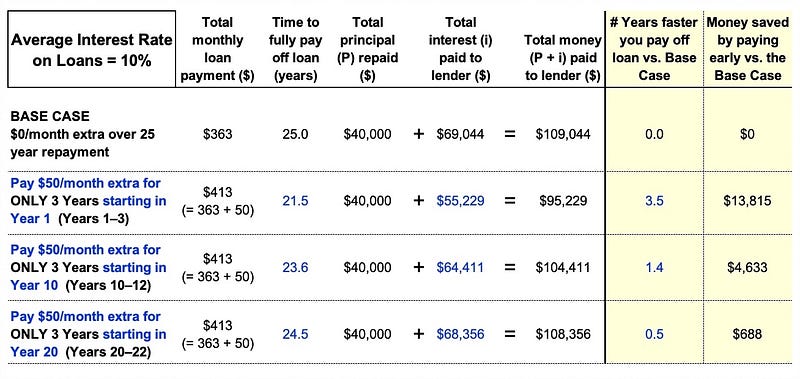

Here is our base case for today: $40,000 in loans at 10% over a 25-year repayment period.

We start by looking at the impact of paying an extra $50/month for ONLY the first 3 years.

- Then we will compare that with (1) paying the extra $50/month for only 3 years but (2) starting in Year 10 instead of starting in Year 1.

- Finally we’ll move those 3 years of extra $50/month payments out so that they start in Year 20 of the 25-year repayment term.

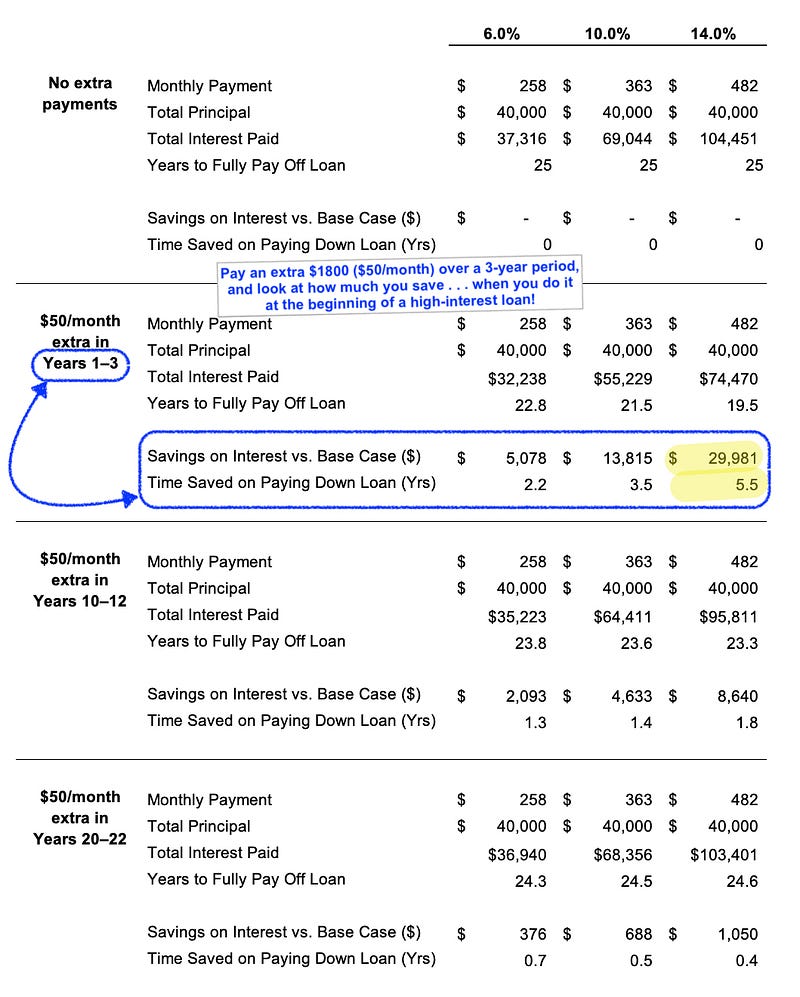

(At the end of the article, I will also show what the numbers look like for student loan interest rates at 6% and then at 14%.

Paying $50/month extra in Years 1–3; then Years 10–12; and finally Years 20–22

Four things jump out at me from this table:

- The $13,815 you save in interest by starting your 3 years of $50/month extra payments at the beginning of your repayment process is about 3X the amount you save if you wait to start those 3 years until Year 10.

- The $1800 you pay in the first 3 years (36 months x $50/month) ends up leaving you with an extra $13,815 in your bank account at the end of your loan repayment. “Pay $1,800 and get back $13,815”…and that is a guaranteed, zero-risk ROI (return on investment.) That beats what you can do on average in the stock market by a country mile when you factor in both typical ROI and typical stock market risks!

- By paying $50 extra per month for just the first 3 years, you also finish paying off your loan in 21.5 years — 3.5 years faster than the base case.

- Waiting until Year 20 to make those 3 years of extra payments gives no real benefit in terms of saving on interest or in terms of paying off the loan faster.

Bottom line, if you’re only going to make a limited number of extra payments, do them as early as possible in the repayment process.

Ok, how much of a difference does the interest rate on your student loans make in all of this?

Short answer: a lot.

Here’s what jumps out at me from the above table:

- Higher interest rates should make a difference on the amount of money saved if you pay extra on your loan at the beginning of the payback period . . . and that is what happens. At 14%, you save almost $30,000 by paying an extra $50/month over the first 3 years. But at 10%, the savings is only $13,800, and at 6%, the savings is only $5,100.

- Making extra payments late in the repayment term makes very little difference, regardless of the interest rate.

An interesting follow-on question

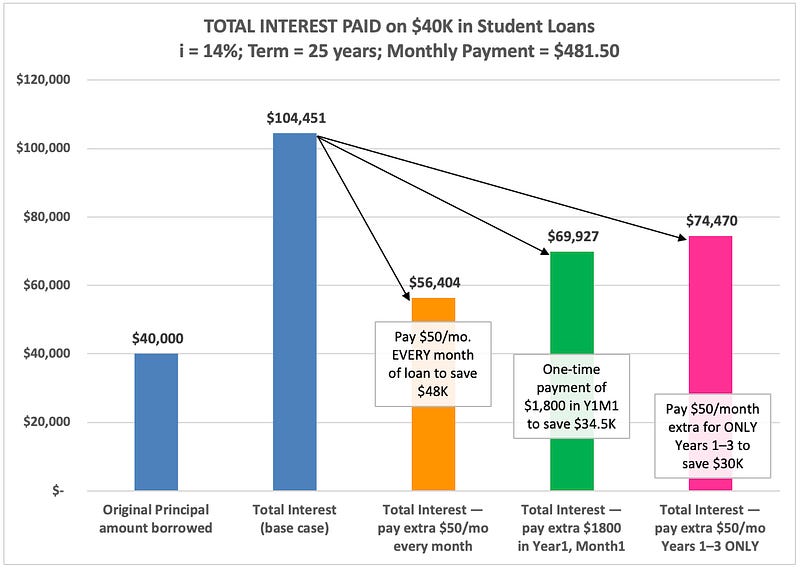

In the case of the 14% interest rate student loan, what’s the difference between (1) paying an extra $1800 in the FIRST MONTH of the repayment period and (2) spreading that $1800 out over the first 36 months?

Would it make much of a difference?

Yes, it turns out that it would make a real difference. Take a look at the chart above.

- In the base case with no extra payments, you pay $104,500 in interest.

- If you pay an extra $50 every month, you’ll pay only $56,400 vs. the original $104,500.

- If you pay the $50 per month for ONLY the first 36 months (Years 1–3), then you save $30K. Saving $30K is great when it only cost you a total of $1,800 spread out in $50 payments over the first 3 years.

- But what if you pay that $1,800 in a single lump-sum payment in Month 1 of Year 1? Then you save $34,500 in interest over the life of the loan. This is noticeably better than if you pay the $1,800 in monthly $50 payments over the first 36 months.

The general rule is, the earlier you pay down your high-interest, long-term loan, the more you save. And the savings can be huge.

One Last Thing

I will talk about this more in a future article, but what has really put financial shackles around the ankles of most Americans under the age of 60 are the massive, fixed, inexorably increasing, and non-negotiable costs in American life like housing, healthcare, education, and childcare.

From the perspective of the totality of those financial burdens, cutting back on what you spend on coffee each week or deciding not to go out with friends once or twice a month isn't going to fix your overall problem there.

However, if you have high-interest loans that you are paying back over a long period of time (20+ years) — including but not limited to student loans — small amounts of extra money paid toward those loans right at the beginning of the payback term WILL make a big difference for you.

Are student loans something that you’re especially concerned about? Please share your comments, questions, and feedback below!

More articles

• What’s the Smart Play If You Borrowed $40,000 at 10% in Student Loans and Just Graduated College? • Chat Threads — Student Loan Borrowers Taken for a Ride as Supreme Court Sides with Lenders • Life Expectancy vs. Healthcare Costs in the U.S., Japan, Germany, etc. — whatever you’re expecting, you’re going to be surprised. • U.S. Housing Price Predictions for 2023–2024 • Are Chinese People Smarter About Mortgages than Americans? • The Social Contract Broke in the U.S. Years Later Than in Japan • 2 Reasons Populations Are Collapsing in Developed Countries • How the Al Dente App Eliminates the MacBook Battery Life Problem

Want unlimited access to all Medium articles? Become a member!

If you appreciate my writing, please share it on social media.

Again, thank you for reading, subscribing, clapping, and sharing — I appreciate your time and attention!