The FAST Tax: Strategic, Fair, and Revolutionary

While not my ideal solution, this one is simple yet progressive (eight brackets) in a way that most tax policy proposals aren’t

Every election cycle, the same debates pop up ad nauseum about how we should reform the U.S. tax system. How do we make it more efficient? Which loopholes should we close in order to bring in more federal revenue? Shouldn’t we make our tax system simpler, overall?

The problem with that last one: just because we make a change that seems “simpler” doesn’t mean it’s automatically the most beneficial option.

I see flaws in most of the popular tax remedies discussed by political pundits and the mainstream media.

Flat Taxes: these proposals, pushed by many conservatives and some libertarians, would be where all earners get taxed at the same percentage-rate, regardless of income level. One commonly-floated example would be a standard 15% tax rate for everybody, which would be disproportionately unfair and burdensome to the working class overall.

The FAIR Tax: an alternate proposal, favored by other conservatives and libertarians, eliminates all income tax and replaces it with a universal 23% sales tax on most goods and services. This plan places self-employed people and small business owners at a distinct disadvantage by inflating their prices in tandem with those of their larger competitors.

Progressive Taxation: these models divide workers into various income brackets, with higher-grossing Americans falling into higher tiers that are taxed at higher percentage rates. Liberals and progressives would presumably structure it to place tax burdens on people within higher income brackets at higher percentages than those from our current tax system.

The current U.S. tax system has seven tax brackets: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. However, this structure allows for different exemptions that enable many high-earning individuals and corporations to manipulate the rules so their overall tax burden is decreased. Working-class and middle-class people have less power and fewer resources to try to game the system in that manner. Furthermore, capital gains, dividends, alternative minimums, and estates/gifts are subject to lower taxation thresholds altogether.

My own vision for an ideal American tax structure has always been to increase the number of tax brackets even further. I honestly wouldn’t see a problem with having fifty or sixty separate tax brackets. Yes, CPAs might complain that it would create more work for them…but my objective isn’t really to make life “easier” for CPAs.

I would design such brackets along a sliding scale. Tax rates separating each bracket from adjacent brackets (on either side) would be no greater 1% apart (and, ideally, more like 0.5% separating each bracket). As far as how to tax capital gains, AMTs, or one’s estate or inheritance — I haven’t yet outlined a structure for that. Whatever sample templates I might synthesize in the future would be designed to balance fairness with increased revenue generation.

But keep in mind, since economics isn’t my area of expertise, my vision (so far) is something I’ve conceptualized only in broad strokes.

Winston Negron, President of the Democratic Hispanic Caucus in Florida’s Lee County, has developed his own permanent tax reform proposal, designed to keep politicians’ hands off the tax code.

The FAST (Fair Automatic Simple Tax)

The FAST tax idea is Negron’s solution for paying off the national debt while closing loopholes and eliminating all deductions (which are used by the uberwealthy to avoid paying their fair share of taxes) while LOWERING RATES for all taxpayers. In this VIDEO from 2019, he outlines how it would work:

Necessary implementation steps:

- Assess the previous tax year’s national debt and the number of taxpayers per income level

- Set a base Permanent Rate for those with gross earnings of $15,000 to $49,999

- Establish differences between economic classes, per bracket

- Determine a DRR (percentage) projecting the number of years required to pay off the national debt

It lowers tax rates for all (including corporations), gradually pays off the national debt, and everybody contributes their fair share.

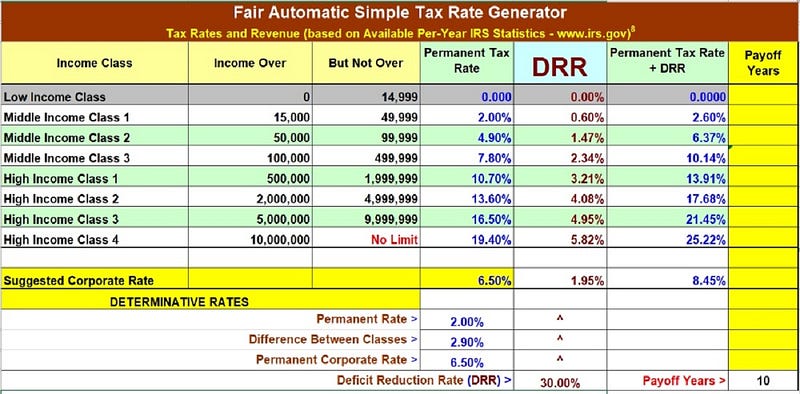

FAST’s taxation structure can be broken down as follows:

- A recommended Permanent Rate, with eight separate tax brackets ranging from 2% to 19.4%

- A Debt Reduction Rate (DRR), added to one’s Permanent Rate

- The DRR would only be in effect when there’s a national debt; it would automatically disappear once our national debt is paid off

- All loopholes, deductions, and special credits would be eliminated altogether

- Americans earning under $15,000 per year would have zero tax liability

- If you earn under $50,000 per year, your annual tax rate is 2% of your income (and so on, as your earnings increase)

If Congress determines that the inheritance tax (“death tax”) is not legally deemed taxable income, it would be ignored under this model. The same sort of waiver could be applied to small farms who’d benefit from tax-exempt generational transfers of farmland and agricultural property, if included in the 2023 Farm Bill.

If this plan was followed, based on the national debt accumulated — plus the number of taxpayers and their gross incomes up through 2021 (based on a 35% DRR) — it would take approximately 10–15 years to pay off our national debt under this model (at which point, the DRR goes away).

It is worth noting that the FAST Tax was created during the Great Recession of 2011, based on the economic reality of the time. However, in today’s economy, the number of billionaires and other taxpayers has increased manyfold. Therefore, except for the ever-growing national debt, proportionally, all things economic remain equal.

Obviously, the longer we wait (and the more additional debt accrues), the longer the future payoff time frame would become.

The FAST tax brackets

The FAST Tax features eight brackets. Let’s dub them as L1, M1, M2, M3, H1, H2, H3, and H4 (these are designations that I, rather than the FAST plan’s creator, have assigned to these Permanent Tax brackets).

L1: those earning under $15,000 pay 0% in income taxes

M1: those earning under $50,000 are taxed at 2% of their income

M2: those earning under $100,000 are taxed at just under 5% of their income

M3: those earning under $500,000 are taxed at just under 8% of their income

H1: those earning under $2 million are taxed at just under 11% of their income

H2: those earning under $5 million are taxed at slightly above 13% of their income

H3: those earning under $10 million are taxed at slightly above 16% of their income

H4: everyone else who earns more than $10 million will be taxed at just under 20% of their income

Then, the DRR, paired with the Permanent Rate, becomes the actual Tax Rate Due. It would be 0% for L1, 0.6% for M1, 1.47% for M2, 2.34% for M3, 3.21% for H1, 4.08% for H2, 4.95%, for H3, and 5.82% for H4.

Someone in the M2 bracket would have a total annual tax liability of 6.37% (a Permanent Rate of 4.90% plus a DRR of 1.47%)

By contrast, someone in the H3 bracket would have a total annual tax liability of 21.45% (a Permanent Rate of 16.5% plus a DRR of 4.95%)

This means that the maximum tax liability for any individual or married couple would be 25.22%, if they fell into the H4 bracket ($10 million annual income and over).

FAST’s suggested tax rate for all corporations would be 8.45% annually (6.5% Permanent plus 1.95% DRR).

Obviously, Congress could adjust these rates in future years. Any bracket could be lowered or raised, in terms of tax liability, when needed. However, congresspersons would clearly be well-aware of the potential ramifications from voters if any such tax increases or decreases were changed without prudent justification.

The benefits of FAST

A point made in Negron’s video is that the revenue raised would strengthen the U.S. when challenging other powerhouse nations, such as China and Russia, on the international stage. He doesn’t mean “challenge” as in proposed military warfare, but rather, “challenge” as in remaining economically-competitive against global power players.

And, ultimately, competition necessitates healthier trade partnerships amongst all countries. But, it also generates American revenue for us to reinvest in more “Made-in-America” products, factories, and shipping centers. We’d still buy from and sell to other countries — but we’re not boxing ourselves into a corner where they can hold us hostage so easily.

This could potentially appeal to some “America First” or fiscally-conservative voters. It would certainly appeal to many centrist and moderate voters.

America might not necessarily be able to remain *THE* dominant superpower indefinitely; but a more all-around beneficial tax plan (such as this one) would prevent us from being overly-dependent or perpetually at the mercy of nations that emerge as rival superpowers in the coming decades.

While my own vision of 50-60 separate tax brackets would still be my personal ideal, I’m taking Winston Negron’s advice, here: don’t let perfect become the enemy of good. “Purity tests” will get us nowhere.

The FAST Tax avoids the pitfalls of other plans. It generates far more revenue than the Flat Tax would. It avoids the regressive taxation imposed upon the working-class that would result from the (so-called) FAIR Tax. And it offers more balance, equity, and fairness than so many of the Progressive Tax proposals that we see presented to us.

Of course, many special interests will resist the FAST Tax. It would greatly reduce their ability to skirt the rules or gratuitously enrich themselves at the expense of consumers. For that reason, there will likely be much resistance to it from many members of Congress.

But that shouldn’t stop us from offering it up as a legislative option. If activists deflated their own ideas from the get-go based on how “likely” it would be that Congress will ever adopt any form of those ideas, then there would be no reason to promote imposing term limits (while hypothetically also cracking down on the lobbyist sectors). Or abolishing Selective Service. Or abolishing the Electoral College. Or making strides with immigration reform. Or crafting some feasible iteration of slavery reparations. Or implementing some degree of religious liberty protections. Or purging dark money from our electoral systems.

Or pretty much anything else in the political realm.

Notwithstanding anything said above: Negron believes that, if a group of new, “untainted,” knowledgeable advocates for the FAST Tax were elected and able to provide the Speaker of the House — and other adherents of fair, rational tax reform — with Negron’s plan, and explain its benefits to taxpayers, his plan might have a good chance to be adopted.

In the same way the FAST Tax’s creator would tell us not to let perfect become the enemy of good…

We shouldn’t fall into the trap of letting “likely” become the enemy of “possible.”