The 8 Kinds of Debt You Must Navigate as a Young Adult

Debt is unavoidable, so you need to manage it the right way

Paying off debt is the top financial priority of anyone living in debt.

Long-term goals like investing and retirement planning are so far into the future that they feel abstract. You won’t feel the benefits (consequences) of investing (not investing) for decades down the road.

But debt?

Anyone who has lived with debt knows the crushing feeling of that debt every single day. This makes getting out of debt the financial goal that people are most motivated to achieve.

Debt is also unavoidable — especially for young people who have to grapple with the historic costs of education and housing.

Rather than subjecting you to a 10,000-word post, I’ve broken the topic of debt into three parts, which we will cover in the coming weeks in the Dollars & Decades series:

- In this first part, I explain why debt is not evil and how to navigate the eight most common forms of debt.

- In part two, I’ll review the importance of your credit score, how debt impacts your credit score, and how to repair it.

- In part three, I break down the most effective strategies to pay off debt and give you a spreadsheet that will tell you exactly how to pay off your debt ASAP.

Debt is not evil. It’s a tool to use with caution

Many people think that debt is evil. When you think of the millions of people who have declared bankruptcy and have spent the majority of their lives living in debt, you can understand why people believe that debt is evil.

Debt is simply a financial tool that allows you to buy something if you don’t have enough money available to make the purchase using cash.

Debt is no more “evil” or “bad” than a physical tool like a hammer. It is the misuse of this financial tool that causes pain and suffering to so many people.

If you use debt in the right way, it has the potential to increase your wealth and improve your life.

If you use debt in the wrong way, it will take you down the path to financial misery.

Let me be clear on what I mean when I say, “If you use debt the right or wrong way.” Four factors will determine if you are using debt properly:

1. The type of debt you are using.

2. The purpose for which you are using that debt.

3. How much debt you take on.

4. The interest rate and repayment terms of that debt.

The 8 kinds of debt you need to know about

This ranking is my opinion, starting with the worst kind of debt and ending with the least bad.

1. Payday loans

Remember when I said debt is not “evil”? I need to amend that statement because there is one type of debt that might actually be evil, and that is payday loans.

What are payday loans? Payday loans are bridge loans to provide cash for people who have run out of money and need to pay bills before their next paycheck.

That sounds pretty harmless. In fact, it sounds like it provides real value to the borrower. You might be wondering why payday loans are bad? The issue with payday loans is that they have the potential to hook borrowers into dependency and keep them coming back every month.

Think of it this way: if you can’t afford to pay your bills this month, there is a decent chance you won’t be able to pay your bills next month. This is especially true when you just added a new loan that needs to be paid off on top of your regular expenses.

Here are two stunning statistics about payday loans:

1. 80% of payday loan borrowers are repeat customers.

2. According to a report from the Centre for responsible investing, the typical Average Percent Rate (APR) on a payday loan ranges from 391% to 443%.

Payday loans can trap you in a vicious cycle of dependency on ultra-high interest debt. For that reason, payday loans are the worst type of debt and must be avoided.

2. Credit cards

In contrast to payday loans, credit cards are not “bad.” They are, however, the most mismanaged and abused type of debt in the world today. The average American owes $5,700 on their credit card. If that does not sound like a lot of money, consider the fact that the average APR for credit cards was over 16% in May 2020. It’s not uncommon for credit card rates to be as high as 20% or even 30%.

You can’t find an investment that can guarantee you a 16%-30% annual rate of return. It does not exist. If you carry a credit card balance, credit card companies are making more money off you than Warren Buffett or any investment manager could ever make in the stock market.

How to manage credit cards

Managing credit cards is simple. There is one golden rule to successfully managing credit cards: always pay off your outstanding balance immediately after making a purchase. If you do that, you will avoid all the pitfalls of credit cards and begin building up your credit score.

This means you only use your credit card to buy something that you could have purchased using cash. To make this easier, most credit card companies offer a grace period where no interest is charged. Typically, this grace period is three weeks. If you pay your credit card balance within the grace period, you won’t be charged interest.

Credit card cash advances

It’s important to know that this three-week grace period for credit cards does not apply to cash advances made on your card. A credit card cash advance is when you use your credit card at an ATM to withdraw cash.

There are three crucial facts you need to know about using your credit card to get a cash advance:

1. Interest begins accruing immediately. There is no grace period; you start racking up interest the second the ATM spits the money out.

2. Cash advance interest rates are higher than standard credit card rates. The average interest rate on cash advances is around 24%.

3. You pay an additional administration fee. To rub salt in the wound, credit card companies

often charge an administration fee in addition to the interest you pay on cash advances. These fees might be a flat rate like $5 or $10, or it could be a percentage of the amount of the cash advance you are making.

How to read a credit card statement

If you have never reviewed your monthly credit card statement, you should because it contains a lot of useful information.

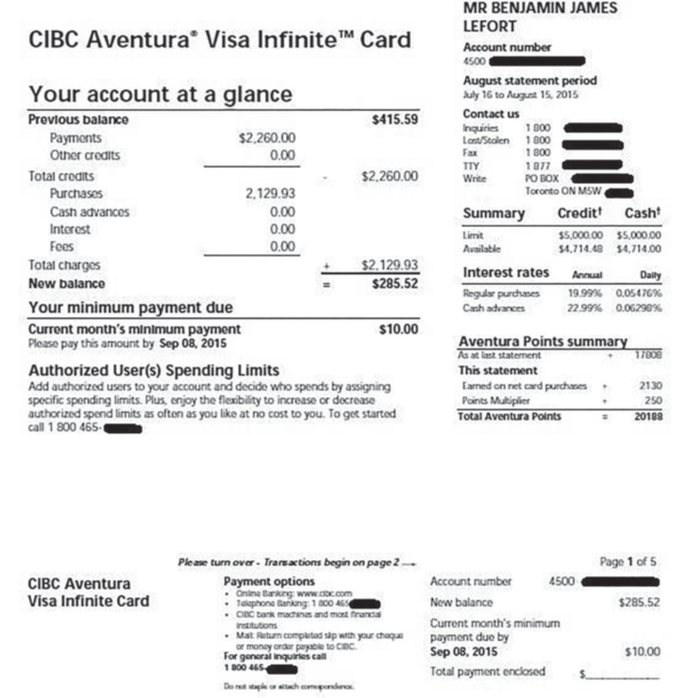

Let’s review a sample credit card statement from an old credit card I had several years ago. Every month, your credit card company should send you a statement that looks something like this:

Your monthly statement contains a lot of information and can feel intimidating. It’s not as complicated as it looks, and specifically, we will be looking for the following information on a credit card statement:

- Name of the financial institution that issued you the credit card. If you have multiple credit cards with the same bank, you could sort them by the type of card. For example, the card in the sample image above is called an “Aventura Visa Infinite” card.

- You’re also going to need to know the current balance on the card.

- The interest rate you pay on any outstanding balance.

- The minimum payment required.

- The due date of that minimum payment.

- Consequences of missing that minimum payment due date.

If we zoom in a little closer, we can easily find that information.

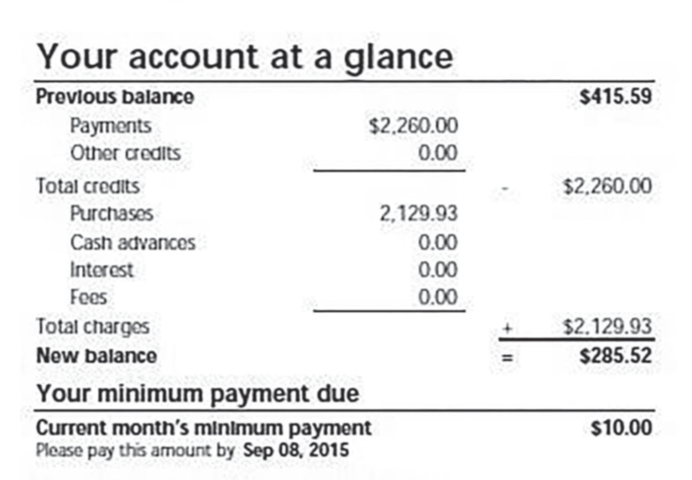

The first thing you’ll likely notice is what’s usually called a “summary of account activity” or, as my bank called it, “your account at a glance”.

Let’s go through this line by line to understand what we are reading.

- Previous balance: Balance on the credit card last month.

- Payments: Total amount of payments you have made since the last statement

- Other credits: Total of any other transactions that reduce your credit card balance, for example, returning an item and having it refunded on your card.

- Total credits: Payments + Other credits.

- Purchases: Total cost of all the things you purchased with your credit card since the last statement.

- Cash advances: Total of any cash you have borrowed from your credit card since the last statement.

- Interest: Any interest you have been charged from carrying a balance on your credit card.

- Fees: Any other fees charged to your account.

- Total charges Purchases + Cash advances + Interest + Fees.

- New balance: This is how much you currently owe on your credit card and is equal to your Previous balance + total charges — total credits.

It’s crucial that you carefully read your credit card account statement every month. It has vital information that you will need to manage your credit card.

Credit card reward points

If you follow the golden rule of managing a credit card, you will put yourself in a position to take advantage of one of the major perks of owning a credit card: reward points.

There are many different types of credit card reward programs, but the two most common are travel and cashback rewards.

1. Travel reward programs allow you to collect points for each purchase you make using that card. These points can typically be redeemed for flights, hotels, and vacation packages.

2. Cashback reward programs provide a cash rebate for each purchase you make with that card. These rebates are typically around 1%-2% of the value of purchases made on the card. Many rebate programs provide different cashback rates for various purchases. For example, some cards give a higher percentage of cashback at grocery stores and gas stations.

In addition to points and cashback, credit card reward programs also provide additional perks to the cardholder. For example, my travel reward card gives me free insurance coverage on rental cars.

A word of caution about credit card reward programs: these reward programs incentivize you to spend money. The more money you spend, the more points you get.

You should never spend money simply to collect credit card points.

That might sound obvious, but you would be amazed how many people justify purchases they don’t need to make because “I get points.” Credit card companies are not stupid. They know that people respond to incentives. Use the reward programs, but don’t let them use you.

Another word of caution on credit cards that offer a reward program: don’t get fooled into paying a high annual fee for the privilege of collecting points.

Often, credit cards that have a reward program offer two different versions of the same credit card.

1. A version of the card with a less generous reward system with a small or even no annual fee.

2. A version of the card with a more generous rewards system with a higher annual fee.

Let me repeat it: credit card companies are not stupid. They know that many people will take the card with a high annual fee for the sole purpose of collecting more points.

Depending on how much money you spend per year, it is possible that the more generous rewards program could justify the higher annual fee. Still, for most people, it’s best to stay away for a straightforward reason. The high-fee credit card incentivizes you to spend more money.

Think about two versions of a cash-back rewards card:

Card 1: Offers 1% cash back and has no annual fee.

Card 2: Offers 2% cash back and has a $120 annual fee.

You would need to spend $12,000 per year or $1,000 per month just to break even on card 2. This provides an incentive to spend at least $1,000 per month to justify the choice to go with the high-fee credit card. You may not even be aware that this is happening, but somewhere in your subconscious is a voice telling you to get the points.

When in doubt, choose the credit card with no annual fee.

While credit cards themselves are not evil, mismanaging a credit card can have devastating consequences on your finances. As long as you always pay off your balance immediately and opt for a card with a low or no annual fee, a credit card can be a valuable financial tool.

3. Personal loans and lines of credit

Unsecured personal loans and lines of credit are other forms of debt that people often abuse.

The term “unsecured” refers to the fact that there is no collateral attached to these loans. A mortgage is a “secured” loan, meaning the loan is secured against your home. If you don’t pay your mortgage, the bank can take your home.

This is not the case for unsecured loans and lines of credit, which is why they have a higher interest rate than a mortgage or other secured loans. The bank takes on more risk with an unsecured loan or line of credit, so they charge a higher interest rate to compensate themselves for taking that risk.

You might be wondering what the difference between a loan and a line of credit is.

A personal loan is a lump sum of cash. It is useful for financing a large, one-time purchase like a car. It can also be used as a way to consolidate higher-interest debt like credit cards. Payments on a loan typically begin as soon as you receive the money.

A personal line of credit is a financial instrument where you are granted the right but not the obligation to borrow money up to a maximum amount. For example, if you are approved for a $10,000 line of credit, you can choose to borrow between $0 and $10,000. You only pay interest on the outstanding balance of your line of credit.

Personal loans and lines of credit can be useful if you need to consolidate higher interest rate debt like credit cards and payday loans into a single monthly payment with a lower interest rate.

On the other hand, if you use personal loans or lines of credit to fuel consumption, like buying a new TV or going on a vacation you can’t afford, they can get you into financial hot water.

4. Car loans

Cars are most people’s second-largest expense in life and are one of the areas many people spend way too much on.

I am also no fan of car loans because they trick people into buying a more expensive car than they need. Just because someone will lend you $40,000 to buy a car does not mean you can afford or need to buy a $40,000 car.

Sadly, this is exactly how many people make their decision on what car to buy. They buy the most expensive car for which someone will lend them the money to buy. Borrowing money and paying interest to buy something that will one day be worthless is not a smart financial move.

That is why The average monthly car loan payment for a new car is $725. Take a moment and compare that number to the amount you save for retirement each month.

Rather than going further into debt to buy a “cool” car, why not buy the crappiest (and safest) car you find and redirect the savings toward our financial goals?

5. Loans from family and friends

Not all debt comes from credit card companies or banks. Oftentimes, people borrow money from their friends and family. It’s difficult to rank these types of loans because they have the highest variance in outcomes.

Borrowing money from close friends and family can work out great if you repay the loan in the agreed-upon timeframe. This could be a lifesaver if you need cash but can’t get a loan from a bank.

However, there are a lot of risks involved in borrowing money from people you know, and it goes beyond financial risk. You risk losing your relationship with that person.

There are some things in life more valuable than money, and relationships with the right people are one of those things. Never borrow money from friends or family unless you are willing to potentially sacrifice your relationship with that person.

6. Student loans

We are now officially out of “consumer loans,” which is when you take on debt to buy “stuff,” and now moving into “investment loans.”

Student debt is a tricky issue. On the one hand, it has never been more expensive to get a college education. That is why 54% of college graduates have student debt, and the average student loan is $37,338.

On the other hand, college graduates have the lowest levels of unemployment and earn more money than people who did not graduate from college.

Here are some stats from the Social Security Administration about the impact of education on lifetime earning potential.

- Men with bachelor’s degrees earn $900,000 more lifetime earnings than male high school graduates.

- Women with bachelor’s degrees earn $630,000 more than female high school graduates.

- The numbers are even more lopsided for those who complete graduate school.

- Men with graduate degrees earn $1.5 million more lifetime earnings than male high school graduates.

- Women with graduate degrees earn $1.1 million more lifetime earnings than female high school graduates.

Education is an investment in yourself.

I took on $50,000 in debt to complete my master’s degree, and it was one of the best decisions I ever made. It increased my income substantially and allowed me to easily get out of debt and quickly begin building wealth.

Whether or not student loans end up being good debt or bad debt depends entirely on you. If you don’t overextend yourself and leverage your education into a high-paying career, it can be a great decision.

If you flunk out of school or never pursue a career related to the education you received, then student loans are a waste of money and a financial burden that stays with you much of your early adult life.

Anytime you invest in yourself, the outcome will be entirely dependent upon what you do.

7. Mortgages

In many circumstances, owning a home can be an excellent financial decision. A mortgage allows you to buy an asset worth hundreds of thousands of dollars without having the money upfront.

As a form of debt, mortgages are as good as you will get.

The interest rate for mortgages is lower than any other type of debt you will find.

You have longer to repay the debt (up to 30 years) than any other type of debt you will find.

That being said, don’t go overboard and buy a bigger house than you need. A bigger house means a bigger mortgage, which means higher monthly payments. If you have a four-bedroom house but only use one bedroom, you are paying interest on three rooms you don’t use.

A bigger house also means higher property taxes, utilities, and maintenance costs. In the same way that a car loan can trick someone into thinking they can afford a nicer car, a mortgage tricks many people into thinking they can afford a bigger house.

Buying a home and taking on a mortgage is one of the most important financial decisions you are likely to make. You need to be smart about it. Buy the least amount of house you are comfortable living in and minimize the size of your mortgage.

8. Loans to buy income-producing assets

The best kind of loan is one that is used to buy investments that will increase in value and pay you income along the way.

Examples of income-producing assets:

- Real estate.

- Stocks.

- Businesses.

Borrowing money to invest is called leverage. Leverage can increase your investment returns and your net worth. Still, it also increases your level of risk and, if misused (or if you simply have bad luck), can have disastrous financial consequences.

One should be especially cautious when borrowing money to invest in the stock market, which is highly volatile and highly liquid — A very dangerous combination, especially when debt is involved.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any significant financial decisions.