The 7 Ways I Paid Ourselves Over $20,000 This Year

Consistency is key

When the thousand dollars that I invested into my wife’s Roth IRA cleared this week, I will have Paid Ourselves First in the amount of $20,500 this year. Plus another $7,000 to $8,000 or so.

Before I detail how, I feel obligated to issue the disclaimer that I realize the amount is higher than many folks can swing. Conversely, to many people I know and others I only know of through reading their stories or blog posts, it’s not very much.

One must recognize that we all have our own Shade of Green and that we are largely writing for those much in the same financial range as ourselves on this particular publication. There is likely some amount of readers who have already obtained multimillionaire status, but likely not a whole heck of a lot. Conversely, there are probably not too many whose income is in the lowest quartile and just barely making it month to month.

Personally, most of my own family’s Joneses are far wealthier than we are. Many of my friends and family are in the “low millionaire” range, and a large percentage of the developers, investors, and business owners who I work with as an economic development professional are what I consider “real” millionaires. Those who could stroke a seven-figure check if need be without feeling a tremendous amount of pain.

So this particular list of seven ways that I Paid Ourselves over $20,000 is a significant amount for a long-time, hard-working government employee in the field of economic development. That number represents roughly one-sixth of our household income (my wife works extremely part-time) and well over twenty percent of our take-home pay.

And do not for a New York minute think that we do not have many expenses. Our typical months run anywhere from a low of $8,000 to well over twice that amount, but I am including the investment numbers with that too.

With that out of the way, without further ado, here are the seven ways.

I funded my IRA the lazy way

Several years ago, I finally heeded the advice of one of my top three personal finance gurus, David Bach.

In The Automatic Millionaire, he not only advises paying yourself first but concedes that simply deciding to do so is not enough to guarantee success. There are behavioral issues that need to be addressed. As humans, we often have great intentions when it comes to budgeting, diets, and saving plans, but we are rarely able to stick with them for the long term. Every new year we make resolutions to lose weight and save more, but by the end of every February, we give up on our diet and start racking up credit card debt.

Bach advises taking the effort, thinking, and procrastination out of it and simply setting your investments on automatic. Every platform has that feature by now.

Hundreds or possibly thousands of other personal finance writers advise the same thing.

Putting that into practice a few years ago, I signed up for automatic investments into my IRA, transferring $500 into it twice per month for the first seven months of the year. I like to think of it as the Lazy Way to IRA.

Now that the IRS has raised the amount that you can invest in your IRA, I will have to initiate one extra payment, but I’m cool with that. It is just a few clicks on the keyboard so long as I have the funds in our checking account.

It may not be as exciting as discovering the next crypto that will “moon,” but do not forget to contribute to your IRA so long as you fall under the government’s income limit, as we do.

I paid my wife $7,500

I met my better half in the spring of 1990 when I was a 19-year-old college sophomore, and she had just turned twenty. Fast forward to today and we have been married for over twenty-six years and have a twenty-four-year-old son and a nineteen-year-old daughter.

I may write about marriage at some point, but suffice it to say that in ours, we assume what many would consider traditional roles. She spent many years as a stay-at-home mom, and I went off to work hard to provide financially, among other things.

She has yet to invest on her own, but I have invested to what now adds up to a low six-figure portfolio on her behalf.

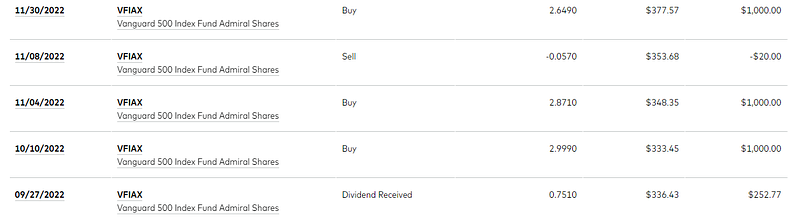

For the first nine months of the year, I dutifully mailed a $500 check to Vanguard for her Roth IRA. Vanguard recently forced old-school paper account holders like us to convert to digital, so I put our last non-digital account onto its website.

I transferred an even thousand dollars into her account in the final three months of this year, bringing the amount that I “paid her” in the form of investing into the most ubiquitous and one of the oldest mutual funds out there to $7,500.

My one investment that rose this year

While the rest of the investments that I have made on my family’s behalf fell hard this year, one of my investments rose.

Rather than just park funds into some boring savings account, CD, or money market fund, I began putting some funds into what is quickly becoming one of my favorite investments.

Having been gun-shy to become an actual landlord for many years, I decided to get “back” into investing in real estate through this crowdfunding platform.

There are many things that I like about Fundrise but am not generally happy about. I agree with many of the stories written by Jared A. Brock, who constantly decries the direction that real estate is heading whereby landlords and corporate landlords, in particular, are gaining far too much economic might, snapping up single-family homes faster and for higher prices than many aspiring homeowners could. A significant number of homes in my own neighborhood have been purchased by these institutional investors and converted into rentals over the past several years.

This trend does not bode well for my own children, both of whom have expressed serious doubts about ever becoming homeowners themselves, although I personally believe that both of them eventually will.

Whatever the case may be, Fundrise is right up there with the other corporations buying up and funding entire subdivisions and housing developments that will either begin as rental communities or will become them.

So if you also believe that this trend will continue and want to become part of the asset-owning class, this particular investment may be right for you.

The other thing that I like about Fundrise is that it urges you to set a goal. My personal goal is to have $25,000 invested into it by the spring of 2026 when my plan is to begin drawing funds down by about $5,000 per year to support my wife’s and my travel. Most likely to visit our children.

I know all too well the old adage about the best-laid plans…

But Fundrise advises investors to hold their funds for at least five years, so five years after I began investing in it is when I plan to begin divesting.

As I frequently say and write — If, If, and If. If I can remain gainfully employed and not be in dire need of these funds, If the real estate market does not completely collapse and the projects that Fundrise buys into do not fail, and if my wife and I can both remain in decent health, then I very much look forward to writing stories about using these rising funds in the not-too-distant future.

I do not want to become one of those guys who grinds away for decades, finally achieves millionaire status, and then keels over just in time to leave a decent inheritance. I invested $6,000 into it this year, bringing my grand total to $18,000 over the past two years. It’s currently worth $21k and some change.

I invest in Blue Chips

Alphabet aka Google. Microsoft. Apple. Amazon. Tesla. Berkshire Hathaway. Walmart. JPMorgan Chase. Visa. Home Depot. Pfizer.

You get it.

When I first set up my wife’s Roth IRA, I figured that I would start it off with the most generic stock index fund that Vanguard offers, the S&P 500 index. Because I was such a smart guy and astute stock and fund picker (yeah right!), I figured that eventually, I would move some or all of it into a more high-flying basket of investments. Perhaps something tech-heavy or into emerging markets.

Well, I never got around to moving it into something else and have no plans to.

As the U.S. stock market goes, so goes my wife’s IRA.

When I moved some funds around in my own IRA about a dozen years ago, one of the two funds that I settled on for myself is so blue chip that is in its name. I have contributed evenly to two mutual funds with T. Rowe Price although the one that I am referring to, the Blue Chip Growth fund, has vastly outperformed the far safer and less risky fund that the other half has been plowed into.

Whatever the case may be, whenever you spend money on one of the five hundred-plus companies held between the S&P 500 or Blue Chip Growth fund, you are contributing to mutual funds that my wife and I combine for about six figures invested.

I invest when the market is up

The longest bull market in history came to an end about two years ago.

All the while, younger and newer investors understandably felt that any funds that they invested in basically anything would continue to grow.

It makes you feel pretty smart.

Older and supposedly wiser investors, such as myself, know that what goes up must come down at some point. The markets cannot continue rising forever.

I realized this both during the years while the markets continued rising and even during individual weeks and days when the bull run was in full swing.

I began the practice of diligently paying ourselves first, no matter what, during the bull run when $500 invested in March might turn into $550 or $600 by the end of the year. It felt good to see our family’s portfolio rise by $50,000 or more in any given year. We even collected over $16,000 in passive income last December alone, which felt pretty good, and I enjoyed sharing it as a story.

But markets do not always rise, do they?

I also invest when the market is down

This year has been a case study in continuing your investing strategy even when you feel as if you are losing money.

Remember an old adage that also happens to be true: you have not lost any money unless you sold something for a loss.

So what is one to do during a year when your portfolio falls month after month while you are doggedly pursuing a wealthier life?

Continue investing, of course.

I will not pretend that it feels good or that even I have one hundred percent confidence that the markets will return to their all-time highs any time in the near future.

But even in a year when my overall portfolio is down by over $50,000, even with the $20,000+ that I have invested, I am going to keep on Paying Ourselves First for as long as I can.

I do believe that the markets will rise once again and that those who either cashed out at a loss or stopped investing during this maybe could be perhaps it is perhaps it isn’t Recession will most likely regret it.

There will be new investors every day, including right now as you read this, and I do not think that they should feel any differently about the long-term prospects of the stock market than someone who began investing one hundred years ago today.

It may take two years or it may take ten, but eventually, I will write a story about the Dow and Nasdaq returning to their all-time highs and I will try to remember to link to this story when that time comes

I pay my kids

I frequently share that I have read more personal finance books, advice, blog posts, and stories than any person ever should. From the top gurus to writers with fewer followers than I have, I have read pretty much anything and everything that I could lay my hands and eyes on.

One such book that I enjoyed is Die With Zero: Getting All You Can from Your Money and Your Life by Bill Perkins.

One point that he makes and that I have been meaning to write about for quite a few years but have not yet due to being a master procrastinator is the concept of the peak utility of money.

Perkins writes that putting your kids first means you give to them much earlier and you make a deliberate plan to make sure that what you have for your children reaches them when it will make the most impact. A real plan for dying with zero includes the kids if you have them. That way, you’ve already separated out their money (which becomes untouchable by you) from your money, which is what you must spend down to zero.

“If the peak utility of money (the time when it can bring optimal usefulness or enjoyment) occurs at age 30, then at age 30, every dollar buys you one dollar’s worth of enjoyment. By age 50, the utility of money has declined considerably: Either you would get a lot less enjoyment out of that same dollar or you would need more money (say, $1.50) to obtain the same amount of enjoyment as you got out of $1 back when you were a healthy, vibrant 30-year-old. For the same reason, as your adult children age, every dollar you give them goes less far, and at some point, that money becomes almost useless to them.”

What the above means is that I recognize that handing a hundred dollars to our daughter or handing a $250 check to our son is far more meaningful to them than paying utility bills, our mortgage, or car payment is to me.

Not that I do not recognize the need for me to pay our family’s bills while also paying ourselves first via our IRAs and Fundrise.

But handing our daughter five twenties before she heads to downtown Chicago for the night or a $250 check to our son, who is living on his own in a town over 400 miles away from us in Athens and trying to “adult” makes all of us happier.

I do not know the exact amount that I have given to our children in addition to paying some of their bills. If I was put on the stand in court and had to estimate, I would say somewhere in the $7,000 to $8,000 range, which amounts to an average of about $600 to $700 per month combined.

It is not anything that will pay us dividends in retirement or pay down debt, but it may just be the payments to ourselves that are the most appreciated.

All Making of a Millionaire readers can now enroll in our free personal finance 101 courses available here.

This article is for informational purposes only. It should not be considered Financial or Legal Advice. Not all information will be accurate. Consult a financial professional before making any major financial decisions.