The 4 Pillars of Succesful Investing — in 8 Minutes or Less

Advice for the reasonable investor

Investing a percentage of your paycheck every month towards an S&P 500 ETF or another portfolio of diversified stocks has always been key to building long-term wealth and passive income. For the past few years, we’ve seen some unprecedented developments take place in the stock market, and with them has come a lot of uncertainty.

On one hand, tech stocks have driven most of the growth in the past 2 years thanks to the AI wave, and this trend is expected to continue. Indexes like the S&P 500 have become extremely tech-overweight, and stocks like Nvidia are trading at XXX times their earnings. This is a typical case of overvaluation and it should have shown some signs of slowing down, but it simply hasn’t.

On the other hand, we have some of the most uncertain geopolitical and economic context in decades, with wars both in the Middle East and eastern europe. Elsewhere, inflation is still very present, and in countries like the US the end of the student loan forgiveness program is expected to shave off $100 billion of consumer spending in the coming years, greatly diminishing companies' profits. These factors have led some experts to believe a recession may be coming.

With that in mind, I thought it would be useful to write up a little reminder on the 4 pillars of successful investing. These pillars are true in any situation:

- No matter the investment timeline you’re looking at

- No matter the economic context you’re investing in

- No matter the strategy you’re going with

- No matter what market you’re targeting

“Nobody knows if the stock is going up, down or round in f*cking circles”

— Matthew McConaughey in The Wolf of Wall Street

Nobody can predict the future for sure. But by having a strong set of core principles when approaching an investment strategy, one can optimize his/her chances of maximizing profits and minimizing losses, all the while being able to sleep at night without fear of losing everything.

Each pillar is written to be as easy to understand and straightforward as possible. This is not a deep-dive article, just a reminder you can save to your favorite “finance list”, and get back to whenever you need it.

Pillar #1 — Diversification

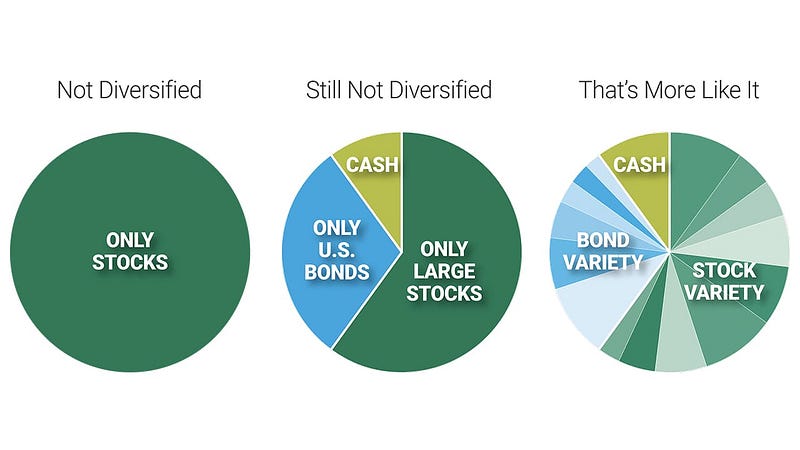

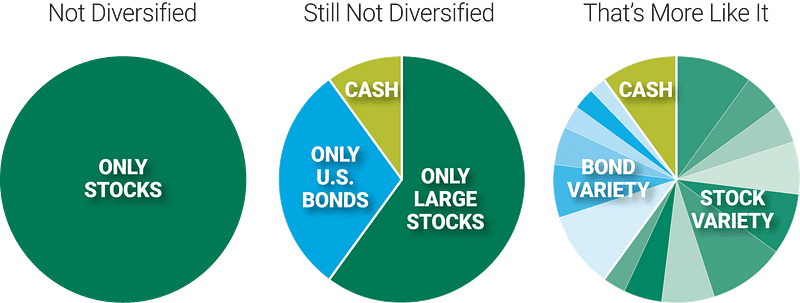

Diversification at its core is very simple to understand: don’t put all your eggs in the same basket because if the basket drops you’ll lose everything. If you put your eggs in 3 different baskets and one falls, you’ve only lost 66% of your eggs.

When investing in the stock market, diversification is the practice of spreading your investments around so that your exposure to any one stock is limited. This practice is designed to help reduce the volatility of your portfolio over time (Fidelity).

When we’re talking about investing in the broad sense of the term, diversification is about investing not just in stocks but also in things called bonds. Within the 2 categories (stocks and bonds), you want to pick a bunch of different variations in order to minimize your exposure:

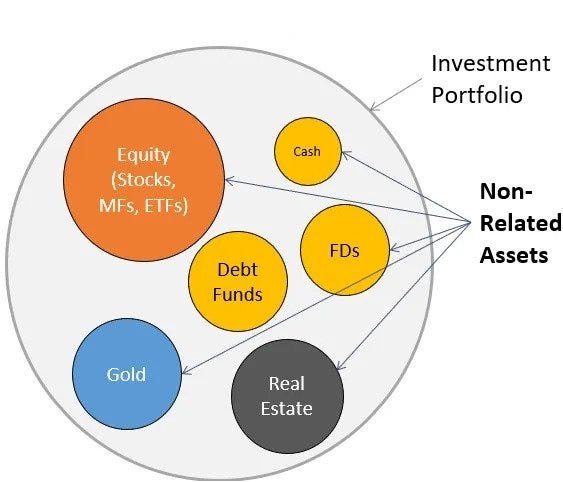

You can also invest in more different types of assets, like gold, real estate, or even foreign currencies, but those things get a bit complex:

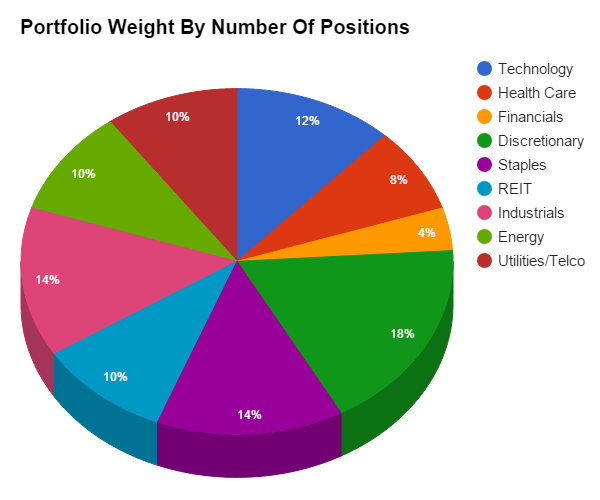

When talking strictly about “stock investment diversification”, you’ll want to pick a bunch of different industries and usually look at the top players in each field.

With this approach, it’s good to look at the expected “trends” for each year and adjust your industry allocation accordingly. For instance, in 2024 tech is expected to continue to dominate, so slightly increasing one’s position there could be an interesting option. Energy stocks are also expected to increase due to the energy crisis, but consumer spending is expected to decrease due to high inflation. Again, these are only predictions and the odds that they will all be correct are very low. But if only one turns out to be wrong and the 4 other ones are right, you’re still in the money, and it’s very unlikely they’ll all be wrong at the same time.

Pillar #2 — Quality investments

There’s no point in spreading your eggs across different baskets if they’re all rotten to start with, right? One of the downsides of diversification is that it’s very easy to use as an excuse to place a bunch of bad bets that will lead nowhere in 90% of cases. That’s why 90% of people who practice individual stock-picking lose money.

The best way to diversify is to do it by only investing in companies that match this criteria:

Limited debt and strong balance sheets.

You don’t have to be an expert to look up those numbers, and you don’t even have to understand everything they entail. We all know that it’s better to have cash at hand for a rainy day and that it’s better to make money than to owe money. The less debt a company has, the less trouble it will have when the economy takes a downturn and interest rates rise (like right now).

Pricing power

Pricing power is the ability of a company to raise its prices without negatively affecting demand or high-profit margins. For instance, insurance companies raise their prices every year to match inflation, and they don’t lose customers because of it. In the tech world, Apple has been steadily increasing the price of their iPhones, and consumers have kept buying them. Unlike insurance companies, this model is a lot more likely to come to exhaustion once people realize they don’t want to pay $1000+ for a phone anymore, so it’s not as scalable.

Decade-long track record (or longer)

The longer a company has been around, the more it has gone through, and the better it will handle economic and financial headwinds. Long-standing companies are especially good investments when their stock price drops as a result of a PR storm, bad management, or simply due to market conditions. Many people will start to panic sell, not thinking long long-term recovery but short-term drop. This will drive the stock price even lower, and who doesn’t like a good bargain on a quality stock?

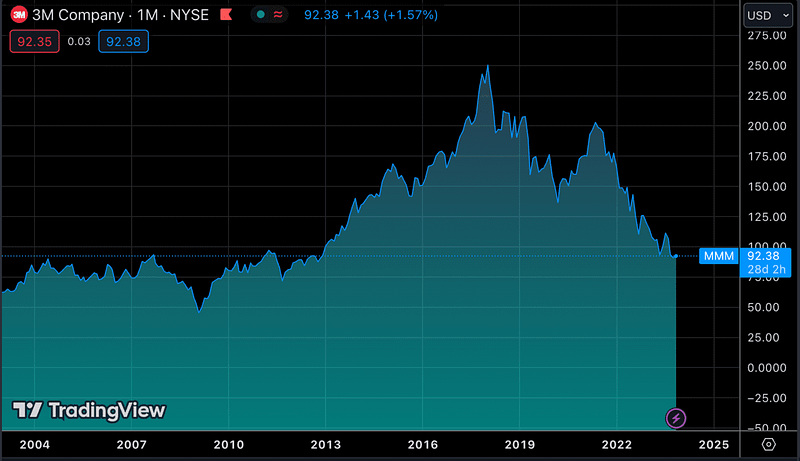

A great recent example of this is 3M. It’s a 120-year-old company operating in the fields of industry, worker safety, healthcare, and consumer goods. It has incredible “internal diversification”, meaning that if one of its branches gets hurt financially, it has 3 other ones to keep growing. It has been through 2 world wars, countless recessions, and economic crises, and it recovered every single time. It’s been having bad press for a while due to an earplug lawsuit trial and a $6 billion settlement that came with it. It’s also in hot waters over forever chemicals in Europe, and this bad news has driven the stock price to historic lows. The stock lost 53% in the past 5 years and is trading at a 10-year low:

This is not the first time 3M has gone through a big lawsuit, and it won’t be the last. The company is committed to completely stopping PFAS manufacturing by 2025, and it has already prepared a 6-year installment plan to pay out the settlement (from 2023 to 2029 including $1 billion in stock).

Pillar #3 — Risk management

Too many people lose money on the stock market because they don’t understand the concept of risk management. Risk management is the process of identification, analysis, and acceptance or mitigation of uncertainty in investment decisions (Investopedia). Risk is inseparable from return in the investment world, and you can never know for sure that your bet is going to be a winning one.

What you can do, however, is draft up a worst-case scenario in which you would lose X% of your investment, and anticipate whether or not you could afford such a loss. That’s where most people fail to optimize their investment. They only think of the potential upside and don’t think of how much they would lose if they turned out to be wrong.

Say that you want to invest in a stock that’s been doing terrible for the past few months. The company has been around for almost 100 years (pillar #2), and has seen all kinds of economic turmoil, and you think the bottom of the curve is near and will pick up again next month. You intend on buying that stock at a discount a few days before the end of the month. Here is an example of what that could look like:

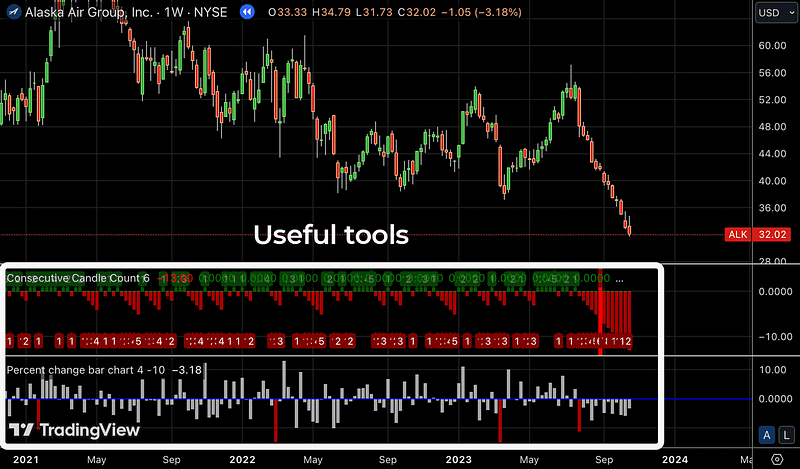

You see some upside here, but what if you were wrong? Well, a good idea to calculate your risk is to look at how much the stock may drop on another typical bad month. You can also look at how many consecutive months the stock has dropped in the past, to get an idea of whether or not it could drop even more. There are plenty of tools that let you do this online:

In this particular case, we see that the stock rarely drops more than 10% even in its worst months. If you decide to invest $2,000, you need to ask yourself if you could potentially withstand a $200 loss. If you think long-term, you’ll also maximize your chances of recovery, and that’s the last pillar we’re going to talk about.

Pillar #4 — Timelines and patterns

Just like Rome wasn’t built in one day, a portfolio doesn’t create consistent wealth in a few weeks. The last key to long-term wealth building and smart investing is, well, to think long-term. It’s good to manage risk (pillar 3), but it’s even better to be patient. If you hold onto a losing investment long enough, chances are the stock will recover and you’ll end up making a profit anyway.

The golden rule of pillar number 4 is to stay away from day trading and never trade on timelines shorter than 1 week. The best way to buy a stock is always to do it with a long-term horizon in mind.

The DCA approach

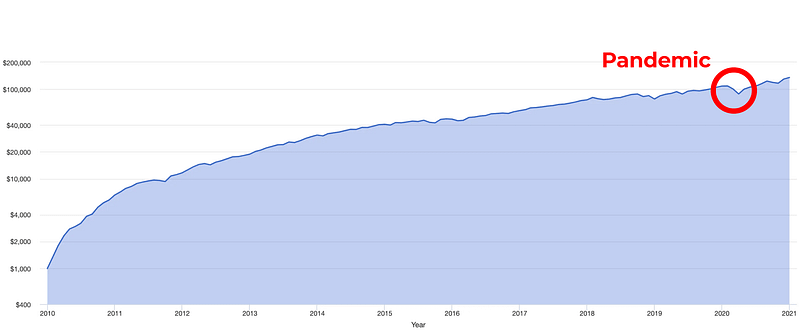

Holding onto your investments for a long time using the Dollar Cost Averaging approach has the double advantage of minimizing the impact of economic downturns on your portfolio while creating exponential returns during periods of growth. DCA consists of investing the same fixed amount regularly, regardless of how the economy is performing. Take a look at this example:

If you had started with $1,000 and invested $400 every month from 2010 to right now, your portfolio would have lost only 18% of its value during the peak of the pandemic, while the S&P 500 lost more than 30%. That’s the power of long-term thinking.

When it comes to monthly timelines, they’re usually the easiest to spot patterns and potential “one-off” opportunities, like a trend reversal or correction to take advantage of only for a short period. That being said, the best strategy is almost always to invest in companies you believe will perform great and have returned consistent returns through many different economic periods.

I interviewed 50 productivity/business experts and made a 150+ page guide out of the project. Get it for free here.

Subscribe to DDIntel Here.

Have a unique story to share? Submit to DDIntel here.

Join our creator ecosystem here.

DDIntel captures the more notable pieces from our main site and our popular DDI Medium publication. Check us out for more insightful work from our community.

DDI Official Telegram Channel: https://t.me/+tafUp6ecEys4YjQ1