Smart Money

Taking Your Financial Medicine

The Role Bonds Play in Your Portfolio

Yes, you need bonds in your portfolio. Unless you are under 30, know what you are doing and have the stomach to handle extreme volatility (40% declines) a 100% equity portfolio is not going to produce a pleasant experience.

The difference between stocks and bonds

When you invest in stocks, you have partial ownership or “equity” in a company. As the company profits, you also profit through increased share prices and dividends. When the company does poorly, so do you. Share prices and dividend payouts can be drastically reduced during bear markets and recessions.

When you invest in bonds, you are giving a loan to the issuer of the bond. The bond issuer agrees to pay you back the face value of the loan on a specific date and to pay you interest payments.

Bonds have a lower expected return than stocks but are less volatile.

Stocks and bonds play different roles in your portfolio

- The role of stocks is to grow your initial investment.

- The role of bonds is to preserve capital, generate income and reduce the overall level of volatility in your portfolio.

Stocks are more exciting than bonds, particularly with interest rates as low as they are right now. However, you may not want too much excitement in your portfolio especially if you are nearing retirement age.

A balanced portfolio will have a mix of stocks and bonds

Vanguard has compiled some interesting data on the expected returns and volatility of portfolios that range from 100% bonds to 100% equities. The following data is from 1926–2018.

100% bonds

- Average annual return: 5.3%

- This portfolio had a negative return in 14 out of 93 years (15%)

20% stocks-80% bonds

- Average annual return: 6.6%

- This portfolio had a negative return in 13 out of 93 years (14%)

40% stocks-60% bonds

- Average annual return: 7.7%

- This portfolio had a negative return in 17 out of 93 years (18%)

60% stocks-40% bonds

- Average annual return: 8.6%

- This portfolio had a negative return in 22 out of 93 years (24%)

80% stocks-20% bonds

- Average annual return: 9.4%

- This portfolio had a negative return in 24 out of 93 years (26%)

100% stocks

- Average annual return: 10.1%

- This portfolio had a negative return in 26 out of 93 years (28%)

These model portfolios tell us something very important. The more we invest in stocks the higher our expected return will be. The 100% stocks portfolio had a 4.8% higher return per year than the 100% bonds portfolio.

However, that higher average return comes with a lot of bumps along the road. The portfolio invested in 100% stocks had a negative return 28% of the time. Compared to 15% of the time for the 100% bonds portfolio.

Not only are you more likely to have years with a negative return with a 100% stock portfolio, but the magnitude of those losses is much higher for stocks. The single worst year for the 100% stocks portfolio was a loss of 43.1% in 1931.

Relative to bonds, when stocks lose, they lose big. It’s easy for people to say they will “ride out the bad years”. However, we never know how we will react when we are living through a market crash. Millions of people sold at the bottom of the market in 2009 and locked in their paper loss into a real loss.

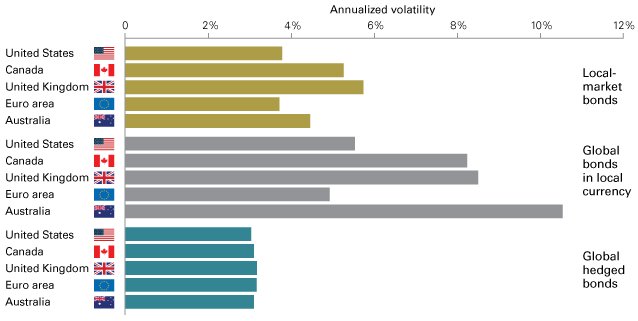

Diversification matters for bonds too

It’s important to not only have a diversification between stocks and bonds but also geographic diversification. This graphic from Vanguard shows the overall volatility of bonds in the U.S, Canada, the U.K, the EU, and Australia.

The results clearly show that a global bond fund that is hedged to an investors local currency reduces the volatility of bonds within a portfolio. Here’s an explanation as to why that is.

- Remember, Bonds are very sensitive to interest rates. When rates rise, bond prices go down. When rates fall, bond prices go up.

- If an American invests in a U.S bond fund and the Federal Reserve cuts interest rates, bond prices will go down

- If an American invests in a global bond fund, hedged to U.S dollars and the Federal Reserve cuts interest rates, the global bond fund may not go down if the other countries in the global bond fund do not cut interest rates.

A word of caution. It is important to ensure any global bond fund you consider is hedged to your local currency. If it is not, you introduce exchange rate risk and the volatility of your portfolio will increase.

Since one of the primary goals of bonds is to reduce portfolio volatility, the data suggests it makes sense to have exposure to a globally diversified bond portfolio that is hedged to your local currency.

Final thoughts

It is true that a 100% equity portfolio will give you a higher expected return than a balanced portfolio. However, expected returns are not guaranteed. We plan for expected returns but we eat real returns. If the market crashes at the wrong time and you are forced to sell at a loss, you have less money to put food on the table.

Bonds are boring, but they make the investing journey a lot less bumpy. Investing in bonds is taking your financial medicine. It might not taste great going down, but it will help ensure your financial health.

If you found this article useful, you may want to enroll in my free “Investing-101” course available right here.

This article is for informational purposes only, it should not be considered Financial or Legal Advice. Consult a financial professional before making any major financial decisions.