POLITICS, ECONOMICS, SOCIETY

Student Loan Debt is Changing

Biden’s SAVE Program Offers Relief to a Lot of Suffering People

Let’s start with the basics: student loans are a scam.

Like so many things, it didn’t start that way. During World War II, U.S. leaders realized that nearly 16 million American men and women who were serving in the armed forces would be unemployed when the war ended, and that this could cause another depression and widespread economic instability similar to the aftereffects of the 1929 stock market crash. In response, the G.I. Bill, formally known as the Servicemen’s Readjustment Act of 1944, was passed through Congress in 1944 in a bipartisan effort led by the American Legion. When FDR’s special representative to the European Theater returned with her report on the G.I.’s postwar expectations, it was clear they wanted educational opportunities previously unavailable to them. FDR “lit up,” one historian recalled, and subsequent versions of the Bill included provisions for higher education.

The final bill provided immediate financial rewards for practically all World War II veterans, avoiding the highly disputed postponed life insurance policy payout for World War I veterans that had caused political turmoil in the 1920s and 1930s. Benefits included payments of tuition and living expenses to attend high school, college, or vocational school.

By 1956, 7.8 million veterans had used the G.I. Bill education benefits, with some 2.2 million attending colleges or universities. The result was a major contribution to the U.S. stock of human capital and the foundation for the economic boom of the 1950s and 1960s. While it was far from perfect — the exclusion of Black veterans and the inclusion of private universities has led one scholar to describe it as “affirmative action for whites” — for those who qualified it was a godsend.

The original G.I. Bill ended in 1956. In response to Sputnik, Federal student loans were first offered in 1958 under the National Defense Education Act (NDEA). These were available only to students studying engineering, science, or education. One result was victory in the space race. Another was engineering breakthroughs and small businesses that culminated in the personal computer revolution.

Student loans became more broadly available in the 1960s under the Higher Education Act of 1965, with the goal of encouraging greater social mobility and equal opportunity. In 1967, the publicly owned Bank of North Dakota made the first federally-insured student loan. By this time, college enrollment was as much about avoiding the draft as it was about gaining an education (paradoxically, the reverse of the pattern of the G.I. Bill). 1973 saw the U.S. first major government loan program, the Student Loan Marketing Association.

The corruption of the system was driven by the recognition that government-guaranteed loans were a risk-free means for large banks to make a buck. To avoid sticking the government (and the banks) with potential losses, it was made virtually impossible for debtors to clear their debt through bankruptcy. Direct-to-consumer private loans became the fastest-growing segment of education finance.

By the time rules for disability discharge underwent major changes as a result of the Higher Education Opportunity Act of 2008, effective July 2010, the amount of student loan debt held by Americans exceeded the amount of credit card debt, totaling at least $830 billion, of which approximately 80% was federal and 20% was private. By the fourth quarter of 2015, total outstanding student loans owned and securitized had surpassed $1.3 trillion.

Guaranteed loans were eliminated in 2010 through the Student Aid and Fiscal Responsibility Act and replaced with direct loans. Like the bailouts of the subprime mortgage crisis, the Obama administration admitted that guaranteed loans benefited private companies at taxpayer expense without reducing student costs. Beginning July 2010, the Health Care and Education Reconciliation Act of 2010 (HCERA) ended private-sector lending under the Federal Family Education Loan Program (FFELP). All subsidized and unsubsidized Stafford loans, PLUS loans, and Consolidation loans moved under the Federal Direct Loan Program.

The promise of “easy money” encouraged colleges and universities to focus on seeing students as revenue streams. This encouraged price inflation and multi-tier pricing schemes that go to inflated administration without educational improvement. The same “easy money” has been offered to students and their families like the “free credit card” offers that show up the first week for a freshman class. Like with those credit cards, banks have been the primary beneficiaries. Like the conditions that created the subprime mortgage bubble, banks had every reason to extend loans to people who will never be able to pay them back. Unlike mortgages, there are no properties to seize to cover the student debt, but that doesn’t matter. By law, a borrower is obligated to pay and keep paying, to the best of his ability, a debt that may be increasing faster (due to interest and compounding) than he will ever be able to cover. Unlike a credit card or a mortgage, there is virtually no possibility of relief through bankruptcy.

Like a mortgage, there may be conditions where it makes sense to lock yourself into years of debt to obtain an education and a career that would otherwise never be yours. Student loans (plus substantial financial aid) helped me to get out of my social class and into a career I loved. But at seventeen, while everyone is an optimist, the odds are not in your favor. Far too many find themselves locked into an eternal cycle of debt. The consequences include a steady stream of income from the poorest to the wealthiest, to the detriment of society as a whole.

The result, as described by a current college student on Medium a few days ago:

The first break I had in college I had an honest talk with my parents. We looked over my options, we budgeted my money, and we researched a lot of different options for me. The saddening conclusion that we came to was college dropouts make about 40% less than college graduates, and to avoid that, I would have to take out student loans and work even harder. I was pissed. I asked my mom why they make it so hard to complete college when in reality, I’m taking high school-level classes for half of my college career. She simply said, “Money is the root of all evil”. And there it was. The sad truth is that the structure of college is simply a money grab for these big schools. They don’t care about our future, all they care about is charging an absurd amount of money for classes that don’t matter while they attempt to create a bigger poverty gap between the students who can afford to complete all four years of college. The U.S. has a college dropout rate of almost 40%, and now it seems clear why that is.

College is becoming increasingly more difficult to complete, and as I mentioned before, it is not because the course material is adapting or standards are being raised. Instead, college graduation is harder to achieve because of how expensive it is to finish all four years. Never once did I struggle with understanding the course material in my COMP 150 course, but I did struggle with worrying that if I didn’t pick up another shift, then I might not be able to buy a parking pass on campus. Doesn’t that seem wrong? The other concerning thing I encountered was where my money was going. I figured that my tuition charges, student fees, and whatever the hell else I have to pay for might at least go to the right things. But, when my 30-year-old professor brings me DoorDash one night and says money is tight, that’s a huge problem. What am I paying for? Is my money not going to the teachers? Is my school struggling to hire teachers, all while having to drop courses because they lack the faculty to teach the course? The answer to both of those questions is yes. — Aidan Loberg (2024)

To the day I retired, I was still paying the banks for my forty-year-old loans. I was lucky: I could afford to pay that eternal tax. But I was only able to discharge the debt when I was declared disabled. In a strange way, Parkinson’s Disease may be the best thing that’s ever happened to me. You never really appreciate how debt slavery constrains your options until you find you are no longer living under it.

So I’ve seen the student loan system from both sides. As a professor, I’ve seen how the transformation of students into “customers” has undermined the missions of the university. As a student and a debt-holder, I’ve seen how debt has made me more risk-averse. Possibilities that look reasonable at eighteen look far different when you have a family to support and a mountain of debt. As a social scientist, I can’t help but wonder what would happen if a generation were freed from that weight and empowered to fulfill their potential.

Enter SAVE

To his credit, Joe Biden has recognized the problem and done all he can to deal with it. Today, Americans owe more than $1.74 trillion in student loan debt — a number that keeps rising while tuition costs continue to increase. A 2022 Bankrate survey found that 70 percent of millennial and Gen Z borrowers have put off major milestones because of this debt: saving money for retirement, paying off high-interest loans, or buying their first house.

An emergency repayment pause related to COVID gave some short-term relief to borrowers. That pause is ending. Another student describes how that feels:

This past fall, with student loan payments set to resume after the pandemic pause, dread was setting in. My pre-pandemic monthly payments had been a crippling burden that made saving money impossible; the pause was a lifeline that had allowed me to pursue a graduate degree and open my first-ever savings account. For more than three years, the dark rain cloud that had followed me everywhere had cleared. Now it was back. — Ellie Quinlan Houghtaling (2024)

Biden tried to deliver a $430 billion debt cancellation plan this summer, only to find that initiative blocked by the Supreme Court. So he took another tack: the Saving on a Valuable Education (SAVE) repayment plan. Announced in August, it begins in February.

In a surprise move, the Biden administration says it will fast-track a big change, previously scheduled for July, that will soon erase the debts of thousands of federal student loan borrowers — undergraduate as well as graduate students who initially borrowed less than $21,000.

The math works like this:

Anyone who borrowed $12,000 or less in federal student loans and has been in repayment for at least 10 years will have their debts automatically erased in February, as long as they first enroll in the Biden administration’s new income-based repayment plan known as SAVE. It does not matter what repayment plan or plans they were in before, so long as they were actively repaying their loans and now enroll in SAVE.

With each additional $1,000 of debt, the window for forgiveness increases by one year. For example, a student who took out $13,000 in loans will now have their debts erased if they’ve been in repayment for 11 years — or in 12 years for those who borrowed $14,000 and so on.

The U.S. Education Department will base the policy on the amount students initially borrowed, not on the amount they currently owe. — Cory Turner, NPR (2024)

I am proud that my Administration is implementing one of the most impactful provisions of the SAVE plan nearly six months ahead of schedule. — President Biden (2024)

The Biden administration does not yet know precisely how many borrowers will immediately qualify for cancellation through the policy change. On a call with reporters, Education Under Secretary James Kvaal added that this move will help a particularly vulnerable group of federal student loan borrowers: those with low incomes. “About three-quarters of them receive Pell Grants. About one-third of them first attended a community college,” Kvaal told reporters. Perhaps most importantly, “more than 3 in 5 borrowers with defaulted loans originally borrowed less than $12,000.”

Many of these low-debt borrowers also have something else in common, Kvaal said: They left school before completing a degree. In the past, those who left schools without the wage premium that comes with a degree had the worst of both worlds.

To qualify for fast-track forgiveness, borrowers first need to enroll in the SAVE plan. Beginning in February, borrowers enrolled in SAVE will be notified if their debts qualify for cancellation, with no further action required. As of early January, 6.9 million borrowers have enrolled in SAVE (mostly by automatic transference from other plans) with more than half, 3.9 million, of them making incomes low enough to qualify for a zero dollar monthly payment.

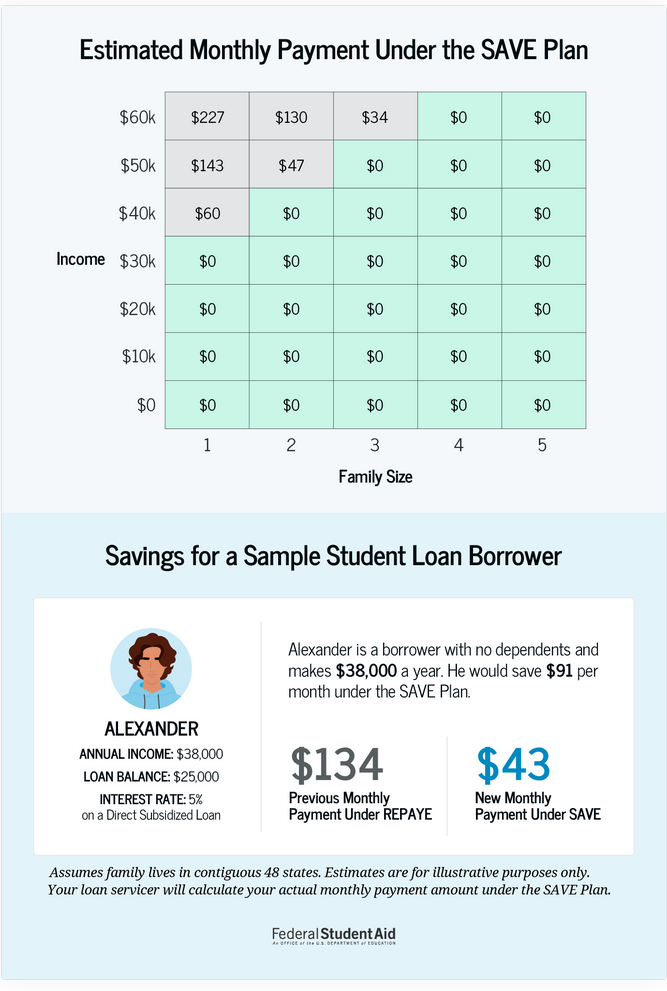

The SAVE plan exempts more of a borrower’s income from the monthly payment math than previous plans, and, under SAVE, interest no longer accumulates beyond what a borrower can afford to pay each month. Under previous plans, borrowers with low or $0 payments — too low to cover their monthly interest — saw that interest explode. With SAVE, that stops.

What’s more, the plan promises multiple windows for loan forgiveness. This means many borrowers will end up paying far less over time on SAVE than they would have on old plans. The Education Department acknowledges that under a previous plan for low-income borrowers, borrowers repaid, on average, $10,956 for every $10,000 they borrowed. Under SAVE, they will pay back just $6,121.

The potential benefit is one reason why Republicans in Congress have been fighting to stop SAVE. (Does this remind anyone else of Trump University?)

“President Biden is downright desperate to buy votes before the election — so much so that he greenlights the Department of Education to dump even more kerosene on an already raging student debt fire,” said the Republican chair of the House Education Committee, Virginia Foxx of North Carolina, after Friday’s announcement. “It would surprise no one if the Department relied on infants playing with abacuses to balance its books — it is a complete and utter disaster.”

But while House Republicans have fought the plan, it seems unlikely the Senate will agree. President Biden has said that even if Congress does send him a bill to kill SAVE, he’ll veto it.

Where To Go Next

The Administration estimates that over 20 million borrowers could benefit from the SAVE plan. Borrowers can sign up today by visiting StudentAid.gov/SAVE.

To apply, first log in to StudentAid.gov using your FSA ID. To receive an FSA ID (username and password), create an account at StudentAid.gov/create-account. (The screen also provides links for people who may already have an account but have forgotten their username or password.) On StudentAid.gov/idr you will need to fill out some information about yourself, including personal information and income. You will have the option to give permission for the IRS to securely access the income information, which lets the U.S. Department of Education recertify you every year. You can also provide your income manually.

Review your plan options. Based on your information, you will be able to see which IDR plan is best for you. You can select the option to place you on the lowest monthly payment plan, which will usually be the SAVE Plan.

Complete your application. Once you have picked the best plan for your situation, click submit and you’ll receive an email confirmation. It may take up to four weeks to process your application, so don’t put it off. Ten minutes online may change your life.

The Consequences Are Personal And Historic

This is not a conventional debt forgiveness plan. It is an Income-Driven Repayment plan (IDR). Therefore, it is much less vulnerable to judicial rejection or Republican lawmakers than conventional forgiveness. The Education Department has run similar IDR programs for decades. As Ryan Cooper wrote in The American Prospect, the Supreme Court would be “more hesitant to strike down a program with such a long precedent.” A recent attempt by Senate Republicans to block the plan came up short. At present, SAVE faces no challenges in the courts.

An IDR means working professionals who can afford to pay back their loans do so, but on terms that their budgets can handle and allow them to move on with their lives. There is relatively little chance of SAVE promoting needless risk-taking. There is no “risky shift” among borrowers (who still have to pay, insofar as it is possible). If anything, it reduces the tendency of lenders to make bad loans. There are no guaranteed eternal repayments.

Predictably, this has driven some elements of the conservative media a little insane. “Unlike Biden’s other student debt cancellation proposals, there’s very little chance the Supreme Court will block it,” a Fox News column observed. The Wall Street Journal fretted that SAVE would “make forgiveness a permanent part of the student-loan system.”

That’s correct — and that’s the point. “SAVE is President Biden living up to Candidate Biden,” in the words of Spencer Dixon, senior policy adviser with the nonprofit advocacy group Student Debt Crisis Center.

Like so many successful Biden initiatives, there has been relatively little reporting about SAVE and the good it can do. While using SAVE (or at least applying for it) is an obvious win for borrowers, few have taken advantage of the opportunity. It’s likely that millions of borrowers who are eligible to apply for SAVE have not heard of the program. Progressives, upset that they didn’t receive the outright forgiveness they hoped for, are ignoring the very real benefit they are eligible for now. Conservatives, who want to block awareness of Biden’s initiative, aren’t telling anyone about it.

From the point of view of conservatives — and especially Trump cultists — there is no reason to draw attention to SAVE. Progressives who spent years fighting for debt relief are maintaining an uncompromising purity standard now that it has arrived in a form different than the one they envisioned.

It wouldn’t be first time uncompromising purity blocked real progress. A Universal Basic Income proposal passed the U.S. House of Representatives twice, in 1970 and 1971, before stalling in the Senate. It was stalled by Democrats who complained the guaranteed income floor wasn’t high enough. By refusing to accept what they could get (and a floor to build on later), progressives lost an opportunity that has haunted us ever since.

This needs to change. It’s time to get the word out. Borrowers who can see their loan repayments substantially reduced — perhaps to nothing — are a voting bloc that could be a key to victory over Trump in 2024. It would be a shame to throw that away.

{kind=link}

{kind=link}